Author: Ana Levine, Source: E1 Ventures, Compiled by: Shaw Bitchain Vision

The sharpest criticism comes from the ECB economists who essentially accuse Bitcoin of being nothing more than a Ponzi scheme in crypto.Their argument is concise and sharp: Since Bitcoin will not enhance the economic production potential, the continued rise in its prices will only cause a pure wealth redistribution effect, and consumer gains are directly at the expense of others.This is just an extra zero-sum game, accompanied by carbon emissions.

This criticism builds on earlier research that shows that Bitcoin’s current design generates benefits losses equivalent to about 1.4% of consumption, making it about 500 times less efficient than a moderately inflated monetary system.Even if the Bitcoin protocol is optimally designed, the benefits losses it causes are still equivalent to an annual inflation rate of 45%.

Criticism of productivity is not limited to abstract models, but extends to disturbing reality.Bitcoin’s security model has the problem that eloquently calls “fundamental limitations”—that is, its energy consumption is linearly growing with the guaranteed value.As Bitcoin prices rise, investment in resources for mining must also increase, which could have been used to fund productive activities such as artificial intelligence, R&D or infrastructure construction.

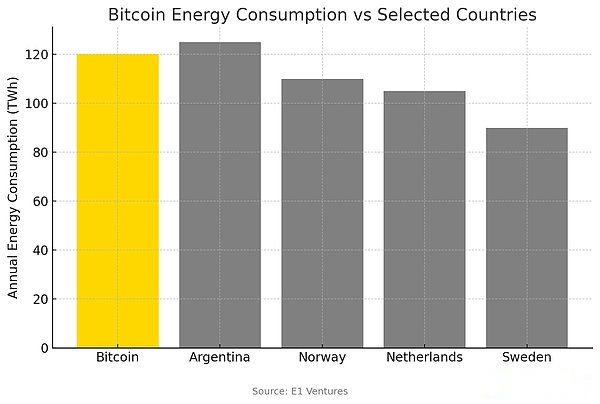

Recent empirical research shows that the computing resources consumed by Bitcoin mining today are equivalent to the economic scale of the entire country.If Bitcoin is a country, its power consumption will be between Argentina and Norway, it makes people ask: Is this “digital gold” really worth the price to the earth?

However, a growing number of research has questioned so-called criticism of productivity, completely redefining Bitcoin’s economic role.These studies no longer view it as a speculative asset that pulls capital out of productive uses, but position it as a fundamental infrastructure that enhances long-term economic stability and efficiency—a similar to what the Internet had seen as an expensive cat video sharing tool before it completely transformed everything.

The “hard currency” argument that Austrian school economists love is believed that Bitcoin’s fixed supply plans and transparent monetary policy are fundamentally superior to the fiat currency system.

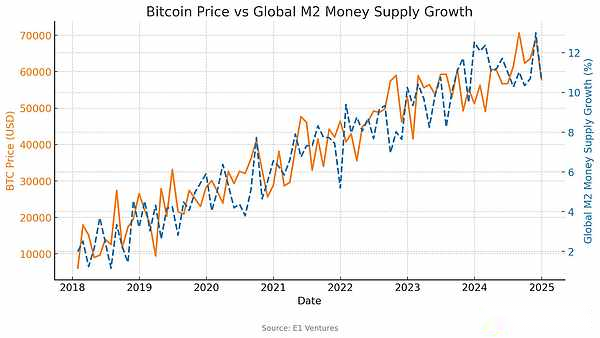

Fidelity’s macro researchers have confirmed that there is a strong positive correlation (R² = 0.70+) between Bitcoin and the broad money supply indicator, indicating that Bitcoin plays a role in resisting currency expansion rather than speculative interference.This correlation is particularly evident during periods of liquidity expansion, indicating that Bitcoin acts as a pressure relief valve for over-expansion of monetary policy rather than competing with productive investment.When the money printing machine is on, the price of Bitcoin will rise.

Empirical evidence: Four major influence channels

Consumption and wealth effect channels

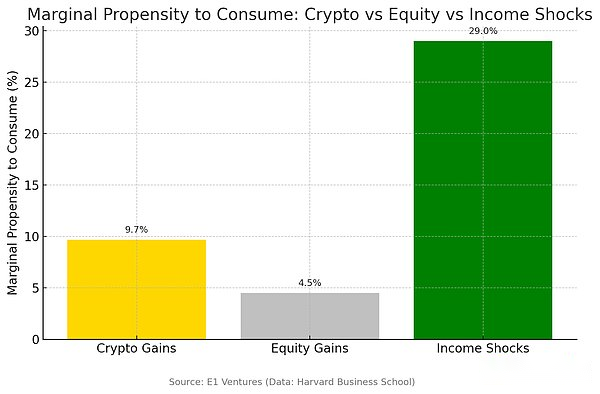

Research by Harvard Business School using transaction-level data from millions of households shows that the wealth effect of Bitcoin actually stimulates real economic activity rather than inhibits.Households show a marginal propensity to spend from cryptocurrency returns is about 9.7%, which is more than double the traditional stock returns and about one-third of the direct income shock.This higher consumption response suggests that Bitcoin appreciation directly stimulates economic demand rather than trapping resources in the quagmire of speculation.

The consumption model is especially inspiring.The growth in Bitcoin wealth flows mainly to cash and check expenses, mortgages, and discretionary consumption—categories that directly support employment and corporate income.In countries with high cryptocurrency adoption rates, house prices have increased significantly as the cryptocurrency market rises, indicating that it has a significant spillover effect on the local economy.

This evidence directly refutes the “crowding out effect” hypothesis.If Bitcoin investment really pulls resources out of productive uses, then we should see a decrease in consumption and investment in the real economy.However, cryptocurrency wealth has formed a positive feedback loop, expanding rather than shrinking economic activity.

Investment allocation channel

Research at the University of Warsaw uses the Markowitz optimization model to show that Bitcoin is a supplement rather than a substitute for traditional productive investments.A portfolio containing Bitcoin can achieve better risk-adjusted returns under multiple rebalancing frequencies and backtracking windows.Crucially, Bitcoin’s optimal configuration changes predictably as macroeconomic conditions change—increasing during periods of currency expansion and decreasing when traditional productive assets become more attractive.

This complex rebalancing behavior suggests that investors see Bitcoin as a hedge against currency uncertainty rather than a substitute for productive investment.When monetary policy becomes more relaxed, funds flow to Bitcoin to maintain purchasing power.When economic growth accelerates and business investment opportunities improve, funds flow back to traditional assets.

If Bitcoin investment comes at the expense of enterprise formation, R&D spending or expansion of production capacity, then the concerns about the “crowding out effect” make sense.However, evidence suggests that Bitcoin adoption is primarily at the expense of excess cash holdings, government bonds and other monetary assets rather than productive investments.As global money supply increases from less than $1 trillion in 1970 to over $180 trillion in 2025, Bitcoin’s share of hard money assets has grown from almost zero to more than 8%—a representation of a rational response to currency instability rather than abandoning productive opportunities.

Innovation and network effect channels

The emergence of Bitcoin-based financial services, including asset tokenization, programmable currencies and decentralized lending, represents real innovation, which enhances traditional economic activity rather than replaces it.These blockchain-based financial services create entirely new categories of economic value through decentralized finance (DeFi) protocols and smart contracts, bringing productivity gains that traditional economic models are difficult to capture, exactly the same as the 1995 GDP statistics failed to foresee the transformative impact of the Internet.

Monetary policy constraint channels

Cross-border analysis reveals an important macroeconomic benefit that economists generally ignore: the binding role of Bitcoin on monetary policy.Countries with higher Bitcoin adoption rates tend to experience more stable monetary policies because governments face competitive pressure from alternative monetary systems.

This constraint function works through several channels.First, citizens with other means of store of value have reduced tolerance for inflation policies.Secondly, the flow of funds to Bitcoin provides instant feedback on the credibility of the policy.Third, the existence of alternative assets limits the government’s ability to obtain seigniorage income.

Research by multiple institutions shows that monetary policy announcements have a measurable impact on Bitcoin prices, which shows that the cryptocurrency market can assess policy risks in real time.This feedback mechanism can prevent the boom and bust cycles unique to pure fiat monetary systems.Instead of weakening monetary authority, Bitcoin enhances, rather than weakens macroeconomic stability by making the cost of bad policy decisions obvious and immediate.

Macro-level conclusion: complementarity rather than competition

Comprehensive empirical evidence shows that Bitcoin is economically beneficial infrastructure, not speculative distractions.Its impact on consumption is positive, investment allocation is becoming more mature, innovation effect is significant, and the discipline of monetary and monetary policy has also been strengthened.Studies trying to find out the crowding out effect have always found that Bitcoin adoption is a supplement to productive investment rather than a competition.

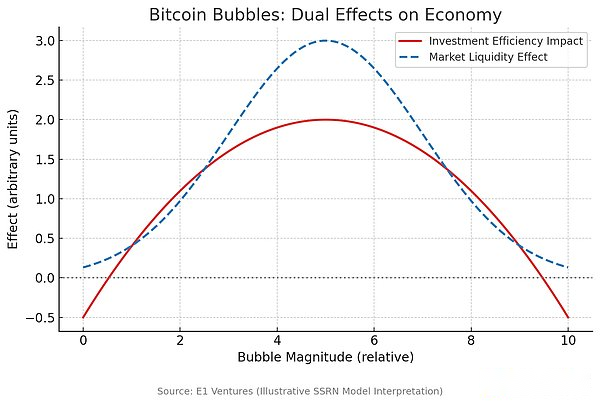

SSRN’s research modeled Bitcoin in an indefinite production economy and found that while the cryptocurrency bubble would reduce investment efficiency, it could also provide market liquidity, thereby facilitating actual investment.The key is that the economic impact of Bitcoin works through multiple channels, which traditional crowding-out effect models fail to cover.Instead of simply replacing capital for production purposes, Bitcoin creates new forms of economic efficiency, reducing transaction costs, enhancing currency stability, and promoting innovation in financial services.

The cyclical fluctuations in the Bitcoin market can temporarily improve liquidity while moderately reducing investment efficiency – these two forces can coexist in a dynamic economy.

The view of Bitcoin as competing with traditional productive investments fundamentally deviates from the point.Bitcoin does not draw resources from productive uses, but plays a role as a supplementary monetary infrastructure, improving the efficiency of existing economic activities.When people buy Bitcoin, they are usually selling dollars, bonds, or other paper assets instead of canceling factory construction or R&D projects.

Macroeconomic evidence suggests that skeptics are concerned about the indicators of the wrong focus.Policymakers should not measure Bitcoin’s direct contribution to GDP (which ignores the role of its infrastructure) but rather evaluate its systemic impact on economic efficiency, innovation and currency stability.

Appropriate policy responses include providing clear regulation that allows Bitcoin’s beneficial effects to flourish while curbing excessive speculation.This means establishing a clear framework for taxation, consumer protection and institutional adoption rather than trying to limit this seemingly economically beneficial innovation.

Countries that attempt to ban or strictly restrict Bitcoin adoption provide a natural experimental sample of the costs of such policies.Evidence shows that these restrictions mainly harm domestic innovation and financial inclusion, but the macroeconomic benefits are minimal.

Conclusion: Combining personal rationality with system benefits

Evidence in microeconomics about individual smart decision-making converges into systemic results that are beneficial to the macroeconomics.When millions of individuals choose to allocate some of their assets to Bitcoin, they are responding to real economic signals about currency uncertainty, inefficiency in the financial system, and technological innovation.

These individual decisions bring collective benefits through improving monetary discipline, improving financial infrastructure, and enhancing economic resilience.Bitcoin adoption is not a speculative craze that diverts resources from productive uses, but seems to be a rational response to the structural problems of existing monetary architecture.

Therefore, macroeconomic analysis supports a cautiously optimistic view of the impact of the Bitcoin economy.Despite reasonable concerns about energy consumption and speculation, there is a lot of evidence that Bitcoin enhances, rather than weakens economic output and productivity.For an asset class that is said to “nothing produces”, Bitcoin shows extraordinary productivity in improving the efficiency of the currency itself—perhaps the most basic infrastructure of all economic activity.

Austrian economists may have always been right: a robust currency is not just an abstract ideal—it is a productive infrastructure.In an era of endless currency experiments and central bank balance sheets expand, Bitcoin is becoming less and less like a speculative bubble, but more like the inevitable evolution of the oldest technology of mankind – the currency itself.