Author: Will Owens, research analyst at Galaxy Digital; Translation: Bitchain Vision xiaozou

In the intersection of the crypto world and traditional finance (TradFi), a new type of listed companies emerged: Digital Asset Vault Companies (DATCOs).These companies explicitly make accumulating digital assets (usually Bitcoin) a core business strategy.Although Michael Saylor’s Strategy (formerly MicroStrategy) laid the foundation for groundbreaking Bitcoin hoarding as early as 2020, the emergence of a large number of new entrants and novel capital strategies this year has made DATCOs the core narrative of the stock market and crypto market.

This article comprehensively sorts out the DATCOs industry ecosystem, deeply explores the market mechanism behind its valuation, visualizes its geographical distribution pattern, and analyzes the capital structure that supports these companies’ continuous accumulation of large-scale crypto asset positions.We will also assess the risks of this model, especially potential crises in situations of capital depletion or equity premium collapse.

1,summary

Currently, the total value of digital assets held by DATCOs has exceeded1000$100 millionAmong them, listed companies Strategy (MSTR), Metaplanet (3350.T) and SharpLink Gaming (SBET) are leading the way.

Bitcoin vault companies dominate in this category, holding more value than930$100 millionBTC; while DATCOs focused on Ethereum have accumulated more than40$100 millionETH.

These vault companies hold791,662博BTCand1,313,318博ETH, accounting for approximately the supply of BTC circulation3.98%and ETH circulation supply1.09%.

Strategy alone has more than280$100 millionThe unrealized profits of the BTC position value is calculated based on the current market price.718$100 million.Smaller participants also showed a lower BTC cost base and considerable upside space.

New entrants are diversifying their portfolios beyond BTC and ETH.The vault company has begun holding at least ten other digital assets, including SOL, XRP, BNB and HYPE.

Ethereum Vault companies are adopting strategies such as pledge and DeFi income to create potential non-dilution returns for Vault capital – an advantage that cannot be achieved by a pure BTC strategy.

Although the United States remains the main gathering place, the emergence of new entrants highlights the growing international demand for DATCOs, which is mainly driven by regional capital market dynamics.

The difference between DATCOs and ETFs is their strategic financing and capital deployment capabilities and may benefit from narrative-driven investor capital inflows.

The DATCO model is susceptible to the collapse of premiums, changes in regulatory policies and turmoil in the capital market.Companies that rely too much on PIPE financing or high leverage may experience sharp retracement under adverse market conditions.

While DATCOs are currently creating a positive feedback loop for cryptocurrency prices, potential position closings may have a counterproductive effect if the category is overscaling.

However, this risk is only at the theoretical level, and except for Strategy, DATCOs is relatively small overall – they only hold about US$32 billion in assets, accounting for only 0.83% of the total market value of US$3.8 trillion in cryptocurrencies.

2,definition

Before we go into the deeper, let’s first clearly define the core concepts of the digital asset vault companies (DATCOs) model.

Digital Asset Vault Company (DATCOs):A listed company that incorporates Bitcoin or other digital assets as the main strategic function into its balance sheet.Unlike traditional companies that only have exposure to crypto assets (such as Tesla), DATCOs actively accumulates digital assets with the clear goal of continuously expanding their holdings.Investors see these companies as leveraged, high-beta investment alternatives to their holdings.

Equity relative net asset premium rate:This indicator quantifies the trading premium of a company’s share price relative to the net asset value per share (NAV).This article defines it as:

Premium Rate (%) = ((Stock Price/NAV per share)-1) * 100

This formula reflects the degree of valuation premium of the company’s digital assets in the public equity market.Note: This concept is different from the general concept of corporate valuation premium (including debt or fully diluted shares), which is more commonly used when describing such companies.

mNAV:That is, “net asset value multiple”, which expresses the same concept as the premium rate, but is presented in a multiple rather than a percentage form.Example: Stocks traded at 2.75 times mNAV have a premium rate of 175%.

ATM(Market price equity issuance plan):Companies are allowed to issue additional shares gradually at the current market price.When there is a NAV premium for the company’s stock price, the amount of crypto assets that can be purchased per dollar of funds raised through the ATM will exceed the equity dilution effect it causes.Because ATMs are highly scalable and can avoid substantial discounts or large-scale issuance, they are usually the preferred capital formation tool for DATCOs.

PIPE(Private investment after listing):Through negotiated capital raising, large investors subscribe to newly issued shares at agreed prices, which is often found in stocks with insufficient liquidity or fewer outstanding shares.Although PIPE can achieve rapid financing, it is usually accompanied by significant equity dilution and brings short-term price risks, which will be analyzed in detail later.

Bitcoin yield:This is a key performance metric to track the efficiency of Bitcoin vault companies accumulating BTC on a dilution per share over time.This indicator reflects the capital efficiency of the enterprise – that is, the ability to convert raised funds into BTC without severely diluting equity.Higher BTC yields are usually positively correlated with higher equity premium rates.

3, methodology

This article uses first-hand and second-hand data sources to analyze the digital asset vault companies (DATCOs) structure, market impact and capital strategies as of July 2025.The research methodology prioritizes public data and adopts a unified analytical framework for all companies included in the study.

Source of data

Analyze cross-validation based on the following multi-dimensional information:

Financial declaration documents of listed companies;

Official news announcement;

On-chain data analysis platform;

The company voluntarily discloses information.

Inclusion criteria

If a company wishes to be classified as a digital asset vault company (DATCO) and can be included in this analysis, the following conditions must be met:

Listed publicly on major exchanges (such as Nasdaq, Tokyo Stock Exchange);

Holding large amounts of digital assets on the balance sheet;

Implement a clear and prudent fund management strategy, that is, asset accumulation is the core of its business model;

This standard excludes Bitcoin mining companies (such as Riot and Marathon) because their digital asset holdings are mainly by-products of mining business rather than active capital allocation decisions;

It also does not include companies like Tesla and Block, and its digital asset purchase behavior is not a core component of its business model.

Position and valuation assumptions

BTC and ETH positions are based on the latest disclosed balance (as of July 28, 2025).

Calculate the market price adopted (as of July 28, 2025):

• BTC price: $118,000

• ETH price: $3,800

All foreign currency positions (such as the yen for Metaplanet and the euro for ALTBG) are converted into US dollars at the spot exchange rate at the reporting time:

• Euro/USD: 1.17

• Japanese Yen/USD: 144.2

4, historical evolution

The Digital Asset Vault Company (DATCO) model was first launched in 2020 by Michael Saylor, and its headline MicroStrategy became the first publicly traded company to convert large amounts of cash reserves into Bitcoin (the price of Bitcoin at that time: $11,650).This move redefines the perception of Bitcoin by companies – not only regarding it as a speculative asset, but also as a strategic reserve asset that can resist the depreciation of fiat currency.

MicroStrategy’s transformation significantly increased the company’s market value and created a new narrative of using Bitcoin as a corporate capital reserve, which subsequently sparked many imitators.

The operation template created by Saylor (by issuing bonds to increase Bitcoin, launching market-priced equity issuance plans, and publicly singing Bitcoin) has established a replicable business model.Although MicroStrategy has always been an isolated case for many years, it has laid the foundation for future generations.

2023-2025Development period

Between 2023 and 2025, multiple catalysts promote the evolution of DATCOs from individual phenomena to systematic trend:

The 2023 Financial Accounting Standards Board (FASB) revised accounting standards to allow listed companies to use fair value measurement of digital assets, so that crypto positions can be valued at market prices;

In 2024, the US Securities and Exchange Commission approved the spot Bitcoin ETF, marking that Bitcoin officially entered the mainstream financial infrastructure system;

Tensions in the global situation and intensified fiat currency volatility have prompted more companies to use Bitcoin as a store of value;

In 2024, Metaplanet (3350.T) will implement a radical Bitcoin increase strategy based on the “Japanese version of MicroStrategy”.It is worth noting that the company has become a typical case of efficient allocation of Bitcoin outside the United States;

In 2025, we are witnessing the rise of alternative currency fund management strategies.Companies such as SharpLink Gaming (SBET), BitMine (BMNR) and GameSquare (GAME) have adopted income-enhanced fund management models.Other blockchain native pledge reward mechanisms that do not rely on the proof-of-work consensus mechanism have also begun to attract the attention of specific companies.

5, digital asset vault company (DATCOs) Why does it exist?

Digital asset vault companies are essentially investment vehicles native to the capital market, aiming to provide investors with leveraged exposure to digital assets (especially Bitcoin, as well as other tokens that are gradually gaining attention).

One of the structural positive factors supporting the DATCO model is the regulatory restrictions faced by large institutional investors when directly allocating crypto assets.As economist Lyn Alden pointed out in The Rise of Bitcoin Stocks and Bonds: trillions of dollars of capital worldwide are subject to investment charters that prohibit direct holding of digital assets but allow investment in stocks of listed companies.For institutional investors such as pension funds, sovereign wealth funds and endowments, DATCOs provides a compliant access to crypto assets exposure, and their stock prices often reflect this scarcity premium.Investors are not only purchasing crypto assets already on the balance sheets of these companies, but also the regulatory arbitrage opportunities and capital formation flywheel effects they represent.

6, market composition and asset concentration

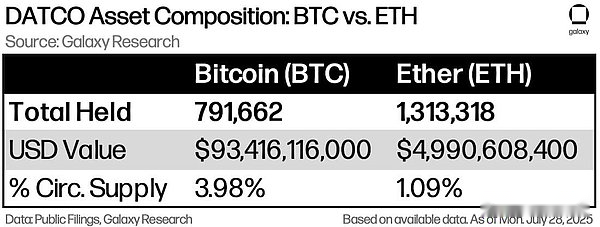

As of July 28, various digital asset vault companies (DATCOs) held a total of more than 791,000 BTC and 1.3 million ETH, worth approximately US$93 billion and US$5 billion respectively based on the current market price.

This asset structure not only reflects the dominance of BTC in existing strategies, but also reflects the rise of ETH treasury narratives – especially among new entry companies that focus on pledge returns or ecological layout.

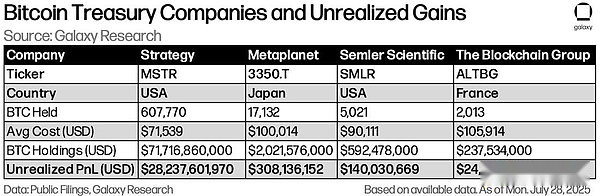

Strategy (MSTR) is still a core participant, with its 600,000 BTC holdings accounting for more than 70% of the total BTC holdings of all listed companies.It has become the world’s third largest Bitcoin-holding entity, second only to the ETF products of pseudonym founders Satoshi Nakamoto and BlackRock.The second-tier enterprises composed of Metaplanet, Semler Scientific, etc. constitute the sub-largest holding group calculated based on market value and unrealized income.

althoughStrategyDominate, butMetaplanetandSemler ScientificCompanies such as the company also showed considerable unrealized revenue.The data is based on publicly disclosed positions and adopts118,000US dollarBTCPricing benchmark.Note: The subtle differences between the calculated income and the unrealized income in this report may be due to the exchange rate fluctuations of each company when purchasing coins.

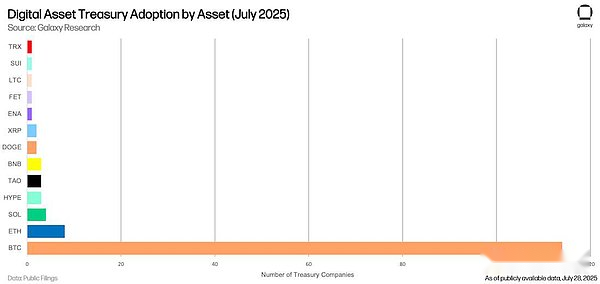

In addition to BTC, more and more companies are implementing the “alternative currency priority” vault strategy.Companies including SharpLink Gaming (SBET), Bit Digital (BTBT) and Tron Inc. (formerly SRM Entertainment, code: TRON) are actively increasing their holdings of non-BTC digital assets and participating in income generation strategies.This model introduces a productive income dimension to traditional strategies – a feature that is not yet available to pure Bitcoin strategies (of course, there may be low-risk BTC native income solutions in the future).

Although Bitcoin is still allDATCOsThe absolute dominant asset, but the company has begun to increase its holdings based on narrative logicETH,SOL,XRP,BNB,HYPEetc.

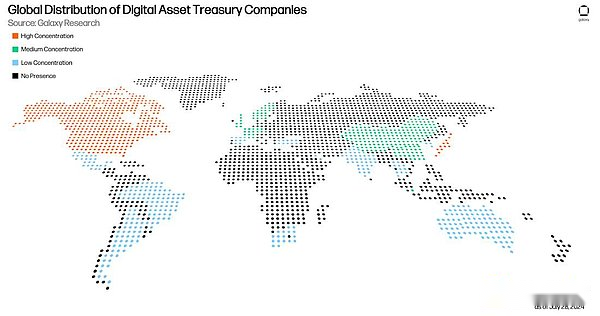

7, digital asset vault company(DATCOs)Geographical distribution

Digital asset vault companies (DATCOs) have become a global phenomenon.The following figure is drawn by Galaxy Research based on publicly disclosed crypto asset holding data, showing the distribution of global public DATCOs as of July 2025.

To evaluate the activity of DATCOs in various countries, we divide the country into three levels (high, medium and low concentrations) based on the number of public DATCOs and their digital asset holdings.

The high concentration hierarchy includes countries with more than 10 listed DATCOs or companies holding unusually large crypto reserves (such as Japan was selected for this hierarchy because Metaplanet held a large number of Bitcoin vaults).The medium concentration level includes 3 to 9 DATCOs, and representative institutions are increasing and reaching trend adoption levels.At the low concentration level, there are only 1-2 countries that can identify DATCOs, indicating that they are in the early stage of participation and market testing.

8, Valuation Difference and Equity Premium

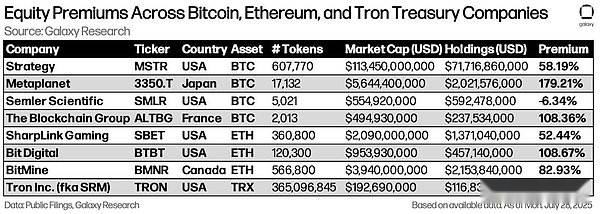

There is a significant differentiation in the valuation of digital asset vault companies (DATCOs).Although these companies share strategies to accumulate digital assets, the premium assessments of their equity relative net asset value (NAV) by open market investors vary greatly.

The following table highlights this difference by comparing eight BTC/ETH/TRX vault companies that hold a large number of publicly disclosed digital assets and have a considerable market value (data as of July 28).

Some companies have relatively mild premiums, such as 58% of MSTR (reflecting its size and maturity); while Metaplanet has a premium of up to 179% with its aggressive capital formation model.

The premium differentiation of ETH-like DATCOs is more significant.For example, Bit Digital has a trading premium of 108% compared to its ETH holdings USD value, and the market seems to convert ETH’s unique earning potential into future capital efficiency for pricing.

Not all premiums are derived from vault strategies.Some companies have physical businesses that generate basic revenue, such as SharpLink Gaming, which operates a sports betting data platform.

The chart also contains Tron Inc. (code TRON) renamed from SRM Entertainment, which pledged 365 million TRX.Although the scale of the vault is smaller than that of some BTC peers, its 64% premium mainly comes from brand collaboration with the TRON ecosystem and narrative exposure.For emerging alternative currency vault strategies, symbolic meaning and signal transmission have actual valuation weights.

9, capital strategy and market mechanism

The core engine of the DATCO model is: raising capital at a premium and converting this capital into higher holdings of crypto assets per share.Companies that perform this cycle most effectively usually get the maximum premium (Metaplanet is a typical example).This section will analyze two of the most commonly used tools: ATM additional issuance and PIPE financing.

Market price equity issuance plan (ATM)

Mature DATCOs generally adopt “market-price equity issuance plan” (ATM) as the main strategy for continuously accumulating digital assets.This mechanism allows companies to issue additional shares at market prices gradually to avoid significant discounts and market fluctuations caused by bulk issuance.ATM gives enterprises precise control: they can raise funds when demand is strong and the market is suspended when the market turns cold, ensuring that the issuance rhythm is synchronized with investor sentiment.

When there is a NAV premium in DATCOs’ stock price, the number of crypto assets that can be purchased for every $1 raised through the ATM will exceed the dilution effect per share caused by it.This forms a “value-added cycle for crypto assets per share”: the company issues additional shares → purchases tokens → increases NAV per share → further expands the premium (called “value-added dilution” in the industry).Metaplanet uses this strategy in absolutely way to continuously expand its Bitcoin position by dynamically adjusting its ATM plan.

But ATMs also have risks.Overuse will suppress stock prices.However, if used properly, it will become an engine for efficient capital growth of DATCOs.

Private equity investment (PIPEs)

Private equity investments (PIPEs) are common tools for rapid fundraising by smaller or newly established DATCOs.Unlike ATM additional issuances, PIPEs are transactions negotiated with buyers of large institutions, usually priced at a fixed market discount.Such financing is significantly efficient in speed and scale, but it will bring serious equity dilution risks and future supply surplus pressure.

In June 2025, Nakamoto (non-Samoto) announced the completion of a $51.5 million PIPE financing to support its Bitcoin funding reserve strategy.The deal is completed within 72 hours and is priced at $5.00 per share.”We will continue to execute the strategy to raise as much money as possible to acquire as much Bitcoin as possible,” said David Bailey, CEO of Nakamoto.

Both BitMine and SharpLink Gaming accumulate strategic financing for ETH through PIPEs.Although these financings have expanded token reserves, they have also increased the number of outstanding shares.

Although PIPEs are very efficient in speed and scale, a rapid influx of capital may suppress NAV-based valuations.Since PIPE shares usually have a lock-in period, as investors expect this part of the stock to enter the market, future selling pressure will be formed.This type of tool is best used in a market environment where the premium is obvious and investors fully understand the company’s ability to convert capital into digital assets.

PIPEs themselves have no absolute advantages and disadvantages. They are efficient tools that can amplify returns and risks at the same time.

10, What factors may lead to market reversal?

The core of the DATCO growth model is to continue to maintain the premium of equity relative to net asset value.If the premium disappears or even turns to a discount, the model will begin to collapse.

The stock prices of many companies have begun to show signs of NAV discounts.In this case, the company may use digital asset reserves or operating cash flow to initiate stock repurchases to embezzle discounted profits.(Bitmine has been approved by the board of directors to repurchase up to $1 billion in stock when management considers it appropriate.) If only individual companies take such operations, the impact on the entire ecosystem will be limited.But these DATCOs are highly correlated – both interconnected and resonant with the crypto asset market that serves as the basis of value.If redemption or repurchase behavior spreads within the industry, it may trigger a larger market reversal.

Current trading strategies of vault companies are becoming increasingly crowded.In the past week alone, at least ten companies have announced the adoption of the DATCO strategy.Its operating template is clearly readily available, and capital is pouring in large quantities – and this poses a risk.When hundreds of companies implement a homogeneous one-way strategy (issuance of additional stocks → purchasing crypto assets → recycling operations), the entire system will become structurally fragile.Deterioration of any variable of investor sentiment, crypto price, or capital market liquidity may trigger a chain reaction.

The reversal of DATCO trading may put significant downward pressure on the price of digital assets itself.Just as the inflow of funds from vault companies provides Bitcoin with “continuous buying”, redemption-driven outflows are likely to have a reverse effect.At least, the net asset accumulation process may be interrupted.

The investment trust boom in the 1920s experienced a similar cycle of self-reinforcement.Trusts trade stocks at a premium above net asset value (NAV) to raise funds through additional issuances to buy more assets.When market sentiment reverses, the same mechanism will amplify downside risks.The collapse of premium cuts off financing channels, while leverage amplifies the losses from asset depreciation.These chain reactions accelerated the stock market crash in 1929 and the subsequent Great Depression.Although DATCOs are more transparent and more well-regulated than trust companies back then, the capital formation mechanism based on mNAV is surprisingly similar.

Market reversals may lead to industry integration.Large players like Strategy (MSTR) who still maintain premium transactions may start acquiring small DATCOs at a discounted NAV.Such transactions essentially allow the acquirer to acquire BTC at a discount on its own equity.However, the premise of this strategy is that the acquirer must continue to maintain a premium advantage.

As these companies grow in size, their influence on the digital asset market has also increased accordingly.The market reversal will weaken the biggest positive factor for cryptocurrencies in this cycle – the normalization of digital assets on corporate balance sheets.The reversal of DATCO trading may reduce the open market’s interest in various types of digital assets and slow down the flow of funds into crypto ETFs, which will drag down the price of the underlying cryptocurrency when other conditions remain unchanged.

It should be clear that except for Strategy, DATCOs are still relatively small participants in the digital asset ecosystem, holding only about US$32 billion in cryptocurrencies, accounting for about 0.83% of the global market value.Although the emerging new DATCO announcements daily may exaggerate its current importance, the above-mentioned market risks are currently mainly at the theoretical level.However, as this category continues to expand, these risks deserve close attention.

11, conclusions and prospects

Digital asset vault companies (DATCOs) have evolved from a novel capital allocation experiment to an important source of structural buying pressure in the crypto market.Their continued rise not only reshapes the way market participants gain exposure to digital assets, but is also profoundly changing people’s perception of the relationship between crypto markets and traditional finance (TradFi).

Looking ahead, DATCOs will play a more important role in the field of crypto.But this development is not without risks.

The reflective relationship formed between the DATCOs stock trading market and the price of Bitcoin deserves close attention.The funds flowing into the BTC vault company enable it to carry out more value-added financing and thus purchase more BTC.This cycle has formed a strong stimulus effect in the bull market.However, if the macro environment turns to risk aversion, this stimulus may quickly turn into a inhibitor.

But there is a more reasonable concern: BTC prices are increasingly affected by risk appetite in the open stock market.This may be inevitable – if Bitcoin is indeed the “purst capital”, companies will naturally spare no effort to acquire it.Although DATCOs broaden the channels for institutional participation, they may also lead to structural dependence, thereby weakening Bitcoin’s target for non-related assets.

The Digital Asset Vault Company (DATCOs) model operates best when the following three conditions are met at the same time:

1) The price of digital assets is on a continuous upward trend;

2) The equity premium remains high;

3) The capital market maintains liquidity and acceptance.

The development pattern of DATCOs is likely to continue to expand in breadth and complexity.Galaxy Research is expected to see the following trends:

• Protocol diversification continues to deepen, and more companies will explore tokens (especially proof-of-stake chains) to generate non-dilution benefits;

• The rise of a hybrid capital management model combines operational businesses that generate cash flow with capital-efficient digital asset accumulation;

• The geographical distribution is further diversified, and new companies in emerging markets will use local regulatory and capital market conditions to start adopting similar strategies.

DATCOs reflect the financialization of cryptocurrencies (and the cryptography of finance).Although they are imperfect, they are a powerful bridge between two increasingly intertwined worlds.

Although DATCOs cannot replace the core cryptocurrency philosophy of self-custody and decentralization in any sense, they provide a compliant and well-liquidated channel for large-scale capital, allowing them to gain exposure to digital assets.

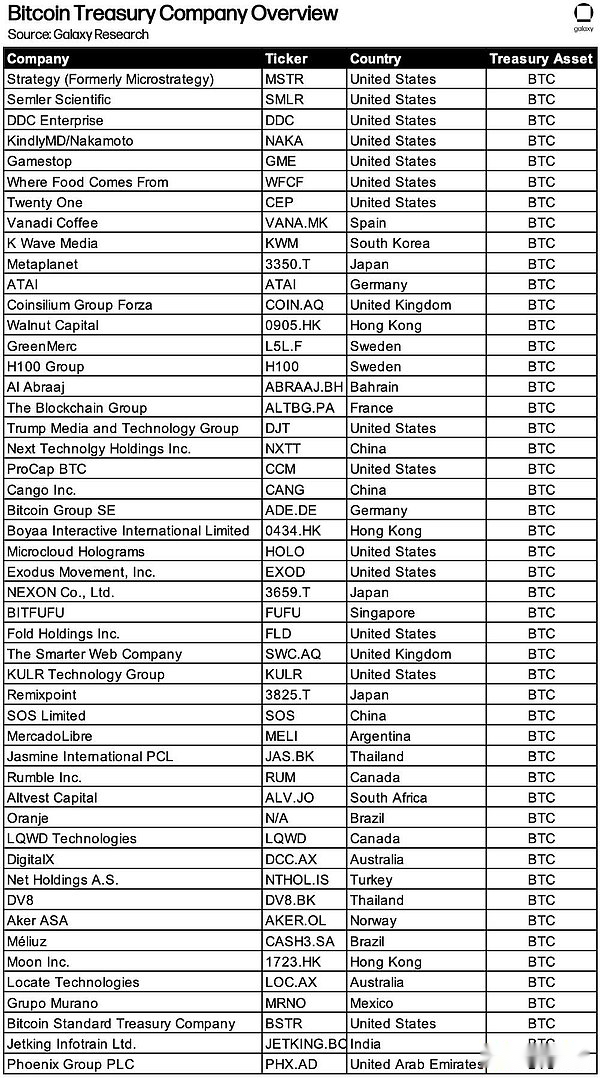

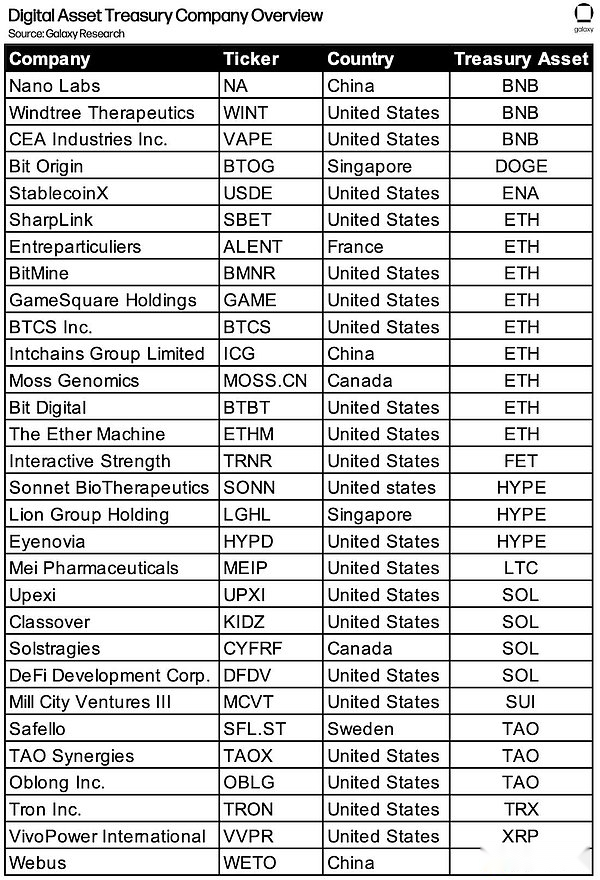

12, Appendix: Company Directory

The following table lists related companies that adopt the Digital Asset Treasury Company (DATCO) model, including case companies analyzed in detail in this report, and other companies that have similar fund management characteristics although they are not included in the core data set due to strategy differences.

This directory is not a complete list.The group of companies that include digital assets on the balance sheet have dynamic expansion characteristics, and the DATCO model continues to evolve in form and function.As capital strategy adjusts, companies may enter and exit this category at different times.

The purpose of compiling this list is to provide direction for the breadth and diversity of open market capital management strategies and also to provide reference for subsequent research.