Author: danny; Source: X, @agintender

Aster’s performance is undoubtedly one of the most eye-catching events of 2025 in the competitive Perp Dex track.Backed by the powerful resources of the Binance ecosystem, Aster quickly rewrites the market structure with a highly aggressive attitude through record trading volumes and aggressive incentive plans.

However, this rapid rise based on the “debt” of future huge token inflation has raised a crucial question: What will happen when the inspiring carnival comes to an end and music stops?Is this created prosperity a brilliant strategy to sustainable liquidity or an illusion that is about to break?

This article will deeply analyze Aster’s past, present and future, explore its evolution path from ApolloX’s pragmatic exploration to today’s market challenger, and focus on analyzing the severe challenges it faces after the “volume browsing” craze.

Part One: A Contender’s Bloodline: From ApolloX’s Innovation to Aster’s Rise

1.1 The Origin of ApolloX: A Hybrid Model Born for Performance

Originally launched in 2021, ApolloX aims to bridge the gap between the smooth experience of centralized exchanges (CEX) and the self-custody of assets in decentralized finance (DeFi).Its V1 version adopts a hybrid architecture of “off-chain matching + on-chain settlement”.This design prioritizes transaction performance and response speed, successfully attracts users who are accustomed to CEX operations, and ensures the uncustodial security of funds through smart contracts.

1.2 Strategic Transformation: Embrace the Full-chain Liquidity Pool with ALP

With the maturity of DeFi infrastructure and the rise of GMX, ApolloX V2 has moved to a fully on-chain mode, at the heart of which isALP (ApolloX Liquidity Provider) liquidity.This is a fund pool composed of a variety of mainstream assets (such as stablecoins, BTC, ETH), acting as the direct counterparty of all traders on the platform.This transformation greatly improves capital efficiency and transaction transparency, and ensures price accuracy by integrating Binance oracle and Chainlink’s dual oracle system to effectively prevent market manipulation.

1.3 Key Fusion: Merge with Astherus and inject the “real benefit” gene

At the end of 2024, APX Finance (formerly ApolloX) and earnings agreement Astherus announced a strategic merger, the most decisive step in Aster’s evolution history.Astherus focuses on maximizing “real gains”, bringing two core innovations to the combined entities (or inspired by Ethena):

-

asBNB: A liquid staking derivative of BNB that allows users to use it as trading margin while earning BNB pledge rewards.

-

USDF: An interest-generating stablecoin powered by a delta neutral strategy designed to create passive income for holders.

This merger gave birth to Aster’s iconic “Trading is mining, and you can enjoy profits when holding positions” (Trade & Earn) model. Traders’ margin is no longer idle capital, but interest-generating assets that can continuously generate returns, which greatly improves capital efficiency and builds a strong competitive barrier.

Aster’s strategy goes beyond BNB Chain and expands to multiple mainstream blockchains such as Ethereum, Solana and Arbitrum.Its positioning is a liquidity aggregator designed to solve the problem of liquidity fragmentation in DeFi, where users can trade on different chains without cross-chain bridges.This ultimate rebranding and multi-chain expansion reflects the current fierce competitive landscape, which requires excellent interoperability for liquidity and dares to challenge the leader directly on other chains.

Part 2: Deconstruction Engine: In-depth technical analysis of Aster architecture

2.1 Dual-mode architecture: a binary method of market segmentation

Aster’s architecture design subtly reflects a deep understanding of market segmentation, and by providing two distinct trading modes, it aims to capture the entire user spectrum from professional traders to high-risk-favored retail investors.This is a classic CEX strategy applied in the DEX field.

-

Professional model (order book perpetual contract): This model adopts a centralized limit order book (CLOB) mechanism, providing experienced traders and institutions with a CEX-like trading environment.It supports advanced order types, provides deep liquidity by “deeply bound” professional market makers, and charges highly competitive fees.

-

Simple mode (1001x): This model is based on the AMM-style ALP liquidity pool, providing retail and thrill-seeking “Degen” traders with a simplified one-click trading experience with a leverage of up to 1001 times.Its characteristics are zero slippage and zero opening fee, but in order to manage the risks of the ALP pool, there is an upper limit on profits.

This dual-mode architecture enables Aster to serve two distinct user groups simultaneously, thus maximizing its total potential market (TAM).A trader who is liquidated for 1001 times leverage in a simple mode is completely different from a trader who manages risks in a professional mode.By satisfying these two types of users at the same time, Aster avoids alienating either party due to its overly single product positioning.

2.2 Capital efficiency and “real returns”: the technology implementation of USDF and asBNB

“Trading is mining, holding positions and enjoying profits” model is Aster’s “money-making method”, which is driven by two innovative assets, USDF and asBNB.The model transforms the opportunity cost of margin (a major friction point in DeFi) into a source of returns, creating a powerful incentive for users to lock capital within the Aster ecosystem.

-

USDF Stable Coin: USDF is a fully collateralized stablecoin minted at a ratio of 1:1 through assets such as USDT.The core mechanism is that the underlying collateral is deployed into delta neutral trading strategies (e.g., holding both long spot and short perpetual contracts) to generate returns, which are subsequently distributed to USDF holders.

-

Technical explanation: The Delta neutral strategy aims to create a portfolio with a delta value of zero, which means its value is insensitive to slight changes in the underlying asset price.This is usually achieved by holding long spot positions and short perpetual futures positions of equivalent values.Its earnings mainly come from the charges for positive capital rates paid by longs to shorts.

-

asBNB liquidity pledge: asBNB is a liquid staking token.Users pledge BNB and receive asBNB, which continues to accumulate BNB’s pledge rewards (and potential Launchpool/Megadrop rewards) while serving as Aster’s trading margin.This enables a single asset to generate multiple revenue streams simultaneously, greatly improving capital efficiency.

In traditional derivatives trading, margin is “dead capital” and is only used to secure positions.Astherus’ core innovation lies in the creation of interest-bearing collateral.By integrating this mechanism, Aster allows a unit of capital to achieve simultaneously: a) as margin; b) earn pledge income (asBNB); c) earn delta neutral strategy income (USDF); d) earn airdrop points.This creates an ecosystem with extremely stickiness and capital is unlikely to flow out, as leaving means giving up multiple returns flows.This directly solves the “mercenary capital” problem that plagued the early DeFi protocols.

2.3 Innovation in privacy and fairness: Hidden orders and anti-MEV mechanisms

Aster integrates iceberg-like functions designed to improve transaction fairness and privacy at the protocol level, trying to solve two core pain points of on-chain transactions: maximum extractable value (MEV) and information leakage.

-

Hide order: Hidden order is a limit order (similar to iceberg order) that is completely invisible on the public order book before the transaction is completed.These orders are submitted directly to the core matchmaking engine, sharing liquidity with visible orders, but completely hiding the trader’s intentions.

-

Technical background: This function is equivalent to an on-chain “dark pool” designed to protect large-scale traders from preemptive trading, sandwich attacks and malicious hunting by MEV robots, but this is still far from “real dark pool trading”.

-

Simple mode anti-MEV properties: Simple mode is advertised as anti-MEV.This is likely achieved through multiple mechanisms, such as frequent oracle price updates from multiple sources (Pyth, Chainlink, Binance Oracle), and possible transaction batching or the use of private memory pools, which prevent MEV robots from exploiting price slippage by inserting transactions.

Part 3: Binance Connection: “Agent” Valuation Theory

3.1 Tracking capital flow: Strategic investment from YZi Labs

Aster’s connection to the Binance ecosystem is deeply rooted, and its funding and development support clearly point to Binance’s strategic intentions.

-

Direct Investment: Records show that Binance Labs participated in ApolloX’s seed round in June 2022.YZi Labs then invested in Astherus in November 2024.

-

Strategic timing: The timing of investment in Astherus (November 2024) coincides with the rapid rise of Hyperliquid and posed a major threat to Binance’s derivatives market dominance.This shows that the investment is a strategic and defensive move.

-

Ecosystem support: This investment goes far beyond the funding level, it also includes mentor guidance, technical and marketing resource support, and ecosystem exposure, ultimately establishing Aster as “the number one Perp DEX on BNB Chain”.

3.2 “CZ Effect”: Interpreting public endorsement as a strategic signal

CZ’s public support injects unparalleled market credibility and attention into Aster, and its behavior pattern far exceeds the ordinary celebrity effect, and is more like a well-thought-out strategic signal.

-

Public promotion: CZ posted on Twitter several times to congratulate Aster on its Token Generation Event (TGE) and promote the project.As analysts pointed out, “CZ rarely shares charts”, which makes his promotion of ASTER an important market signal.

-

Narrative construction: CZ’s remarks, such as emphasizing that Aster’s hidden order function is a solution to the problem of liquidation manipulation in “other on-chain DEXs”, directly positioning Aster as a better choice than competitors such as Hyperliquid.He claimed that Aster became the second largest holder of BSC-USDT, further opening up the “imagination space” of the project.

-

Market Influence: The “CZ effect” was immediately effective, and shortly after its first post, the price of ASTER tokens soared by more than 400%, fueling the narrative that “Aster is Binance’s weapon against Hyperliquid.”

3.3 Comparative analysis of API design

Aster’s API structure design reveals its strategic intention that is consistent with Binance CEX.

-

Structural similarity: In the official GitHub repository (asterdex/api-docs), the structure and naming conventions of the API document are extremely indicative.Its documents are divided into aster-finance-futures-api.md and aster-finance-spot-api.md. This division method is exactly the same as the API structure of CEXs such as Binance, which is also divided into spot, futures, leverage and other modules.

-

Inspiration for market makers: This standardized, CEX-like API structure is no coincidence.It aims to significantly reduce access friction for professional market makers and algorithmic trading companies that have been integrated with Binance.By providing familiar APIs, Aster encourages these key liquidity providers to access their ecosystem with minimal development overhead.This demonstrates a strategy to direct liquidity from Binance’s existing network of professional traders.

3.4 New valuation framework: treating Aster as a function of Binance market value

Combining the above evidence – direct investment, strategic timing, the founder’s continuous public promotion, in-depth ecological integration and familiar API structure – proves that Aster is Binance’s strategic agent (proxy).

Peer-to-peer valuation of Aster with Hyperliquid is a classification error.Hyperliquid’s value stems from its independent L1 technology and protocol revenue.The value of Aster is composed of its agreement revenue and its huge strategic premium brought by its native extension of Binance DeFi.Its valuation should be regarded as a parameter of Binance’s market value, reflecting its importance in defending Binance market share and expanding the Binance ecosystem into the on-chain world.

Aster is a key component of the defense strategy in the post-compliance era.It allows the Binance ecosystem to compete aggressively in the on-chain derivatives space, while creating a critical regulatory isolation layer between the heavily scrutinized CEX and the “decentralized” protocol.After reaching a settlement with the U.S. authorities in 2024, Binance faces strict regulatory oversight, and CZ himself has been banned from holding an executive position at CEX.Meanwhile, the rise of on-chain perpetual contracts led by Hyperliquid poses an existential threat as it attracts the most mature and DeFi native traders.Binance cannot directly launch its own “Binance Perpetual Contract DEX” without incurring immediate and overwhelming regulatory actions.

The solution is to operate through an agent.As CZ’s family office, YZi Labs provides the perfect tool for investment and guidance, while having reasonable room for denial.Aster is built on BNB Chain and directly benefits Binance’s core L1.It is designed to make users feel and use like Binance (API, UI), providing a frictionless exit for Binance’s existing user base and market makers.Therefore, Aster plays a strategic role in “regulatory arbitrage”.It projected Binance’s power and liquidity into the DeFi field without expanding Binance’s formal regulatory boundaries.

Part 4: The Prosperity Created: Game Theory and Consequences of Incentive Trading Volume

4.1 On-chain data analysis: Quantitative volume trading

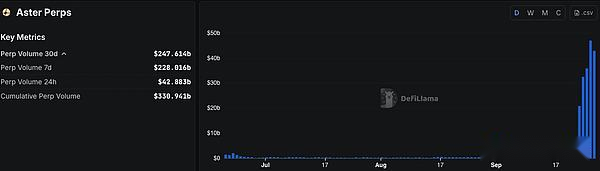

The most illustrative indicator is the ratio of trading volume to total locked value (TVL) and open contracts (OI).At its peak, Aster’s 24-hour trading volume reached an astonishing $36 billion to $70 billion, while its OI was only $1.25 billion, and its trading volume to TVL ratio was about 19, indicating that there is “extremely aggressive volume-brushing transactions.”

The surge in trading volume is clearly related to Aster’s aggressive airdrop points program (“Rh Points”), which rewards trading volume, position time and profit and loss.

4.2 Necessary “evil”?: Strategic logic to guide liquidity

This artificial transaction volume is a necessary but temporary measure.Its logic is a classic guide flywheel:

-

Without trading volume, no attention: A new DEX with no trading volume is like a ghost town that cannot attract liquidity.

-

Incentives generate trading volume: Airdrops create powerful incentives for users, prompting them to generate huge but artificial transaction volumes.

-

Attract market makers: This high transaction volume, even if it is fake, makes the platform look very active.This is crucial to attracting professional market makers who seek high traffic places to deploy strategies.

-

Real liquidity entry: With market makers accessing, they provide depth, real liquidity and tighten the spread.

-

Attract real traders: Combining deep liquidity, low fees and good user experience ultimately attracts organic, non-incentive-driven traders.

By occupying the top spot in the transaction volume rankings on the data platform, Aster has forcibly entered the market’s vision, accelerating its process of gaining market recognition.

This account is very smart, using $320 million aster (4% supply) as the stage 2 incentive, with a forward token incentive of about $600 million token maintaining a market value of 3 billion (15 billion FDV).

4.3 Future debt: Assessing long-term consequences

The main consequence of this strategy is the “future debt” arising from huge airdrop allocations (53.5% of the total supply).This creates a large amount of token suspension, which will be distributed to mining users who have a high tendency to sell, resulting in constant selling pressure.

In order to alleviate this “debt”, the agreement designed an extremely long vesting timetable.TGE unlocked 8.8% (704 million ASTER), and the remaining airdrop allocation will be released linearly within 80 months.This long-term attribution is a key mechanism that aims to mitigate its impact by spreading the selling pressure over a long period of time.

Although strategically effective, the public volume trading has caused it to be labeled as “Temu version of Hyperliquid” and has caused concerns about market manipulation.The key challenge is,Can we successfully transition from false incentive-driven transaction volume to sustainable organic activity before rewards are exhausted and mining users leave.

Huge airdrops and the resulting volume-brush trading are a carefully planned high-risk gambling that uses game theory to solve the cold start problem of DEX liquidity.Aster’s incentive method is similar to Dydx, which targets not only liquidity providers, but also traders and market makers.By rewarding the original trading volume, it creates a seemingly highly active and liquid market.This public signal (dominates the DeFiLlama chart) is designed to attract the real dominant player of liquidity: professional market maker companies.

The “future debt” of airdrops is the cost of this marketing campaign.The bet is that by the time the debt matures (i.e. the tokens are completely “spread”), the platform has attracted enough real liquidity and organic trading flows (“externality”) to absorb the selling pressure.

This is a race against time, so it is forced by the situation and the mode.

Part 5: Challenges to Aster’s financial stability

5.1 Challenge 1: The “post-motivation era” of user retention

Current volumes driven by airdrop expectations are unsustainable.Once the rewards are reduced or ended, the biggest challenge Aster faces is whether it can retain users, market makers and liquidity.There are many cases in DeFi’s history that rapidly declined due to the exhaustion of incentives.

Aster’s breakthrough point is whether it can successfully transform the incentive-driven “airdrop hunter” into a loyal user who truly recognizes the value of the product with its unique product advantages—such as the high capital efficiency brought by the mortgage of interest-bearing assets, the hidden order function that protects large users, and the dual-mode design that serves both professional and retail users.This is a race against time, and the agreement must build a healthy ecosystem driven by real income and organic demand before the “future debt” (i.e., the selling pressure brought by airdrops) expires.This involves first transactions?Or is there a philosophical question of liquidity first?

Token incentives are two-way. When the price is high, the high incentives are paid, so it will attract many market makers, studios, traders, etc. to pay tribute to the handling fee, contribute to the transaction volume, and achieve “discounted buying coins”.

However, as more and more tokens are motivated, more and more market circulating markets will be. Can it be maintained with fee income and even increase the token price become a question mark?When the incentive is reduced, the fee income decreases, the transaction volume decreases, the token price decreases further, and the incentive is further reduced. If this is repeated, the platform will fall into a negative cycle in no time.

The core of the exchange is liquidity (especially copying the CEX algorithm in the Clob model) – which means that it is necessary to attract in-depth participation from multiple market makers, but judging from the current incentive mechanism of Aster, it seems that there is no means or purpose to bind its interests.Hyperliquid knows this truth well. It is not only that the interests of various market makers are firmly tied together from the aspects of API, revenue, and even validator nodes. To achieve a sustainable income scenario that exceeds returns is the pursuit of a DEX.

To put it more, the essence of Hyperliquid is a “liquidity distribution center” dressed in Perp Dex guise – To be more eccentric, with this liquidity structure, what can I do?

Start with transaction data, and only by surpassing transaction data can we understand that DEX and Token are infrastructures that prioritize liquidity services, and then transactions are transactions.During this construction process, the Token first votes for the letter, and then the reward.

5.2 Challenge 2: Systemic risks of algorithms and markets

High leverage and high holdings are the sword of Damocles hanging over all derivatives exchanges, and some of Aster’s mechanism designs may exacerbate these risks.

-

The inherent fragility of the ALP model: In the simple model, the ALP pool serves as the counterparty of all traders, which means that if the trader continues to make profits as a whole, the LP will face huge losses.Furthermore, the model relies entirely on external oracle pricing, and any oracle delay or manipulation can have catastrophic consequences for the fund pool.

-

The ghost of chain liquidation and automatic position reduction: When large-scale, one-way “crowded transactions” appear in the market (especially for small market capitalization and high-controlled altcoins), a severe price fluctuation may trigger chain liquidation.Due to the lack of open and sufficient insurance fund mechanisms, Aster relies on automatic position reduction (ADL) as its last line of defense in extreme cases.The ADL mechanism will force the reverse position of profitable users to make up for system losses. Although this can maintain the solvency of the agreement, it is extremely unfair to profitable users. Once triggered, it may lead to a large-scale trust crisis and capital flight, resulting in a “bank run”.

-

Small-cap counterfeit manipulation endgame: Due to the transparency of the position and insufficient liquidity, incidents like Jelly will likely occur again, especially when the platform is highly dependent on exclusive market makers within the platform (the depth except Aster is slightly insufficient), and there may be a situation where you can’t take care of yourself.When the price breaks the depth of the order book, a liquidity vacuum will appear, and the user is free fall.

-

CEX’s algorithm cannot reach the other side of DEX: CEX’s algorithm for contracts (especially the capital fee rate, margin ratio, number of positions corresponding to leverage multiples, liquidation process, etc.) is designed based on the conditions of its own exchange (such as mm, liquidity basis, and even insurance funds). At present, Aster’s mechanism and liquidity conditions obviously do not yet meet these “preconditions”.

5.3 Challenge Three: Trust Deficit under Decentralized Narrative

-

The Sword of the Top: Extreme Concentration of 96% Token Supply: On-chain data shows that about 6 wallets control up to 96% of the total supply of $ASTER.This extremely centralized ownership structure makes its “community-first” narrative pale and poses huge systemic risks, including potential threats such as price manipulation and governance capture.

-

Terrible Boomerang: When the currency price cannot be maintained, the community’s counterattack may affect the founders and spokespersons.A little bit of negative emotions will be infinitely amplified.

Conclusion: The giant agent at the intersection

Aster’s story is a microcosm of the current stage of DeFi development: it is not only an innovative agreement in capital efficiency and product design, but also a strategic pawn driven by centralized giants behind the scenes and intends to reshape the market structure.

The past life was a clear evolution from pragmatism to innovation; this life was a grand carnival driven by capital and motivation.However, its future is full of uncertainty.After the false prosperity brought by brush volume fades, Aster must prove to the market that it can retain users with its true product value and effectively manage its inherent systemic risks and trust deficits.Whether one can successfully transform from an incentive-dependent ecosystem to a platform driven by real income and organic demand will be the key to its ultimate success or failure.

Aster’s future trajectory depends on whether it can transform artificial momentum into sustainable organic growth before its “future debt” expires.However, as a derivative of the Binance ecosystem, many of Aster’s back-up tricks have not been opened yet, such as being able to bind Aster chain market makers from a mechanism, or becoming an alpha outpost for Binance futures, etc., will be very interesting.

There is no perfect solution in development, only the courage and tenacity to learn to coexist with problems.Looking forward to Aster’s subsequent moves.