Author: Anita; Source: X, @anitahityou

If you only look at the technology news in 2025, you will feel that the world is very good: AI investment is still continuing, the construction of North American data centers is accelerating, and crypto miners have finally “come out of the cycle” and successfully transformed the originally highly volatile mining business into a stable AI computing power service.

But in Wall Street’s credit sector, the mood is very different.

Credit Investors are not discussing model effects, nor do they care which generation of GPU is stronger.They stared at the core hypothesis on the Excel sheet and began to feel a chill:We appear to be using a 10-year real estate financing model to purchase a fresh product with a shelf life of only 18 months.

Continuous reports from Reuters and Bloomberg in December revealed the tip of the iceberg: AI infrastructure is quickly becoming a “debt-intensive industry.”But this is just an appearance. The real crisis lies in the deep-seatedFinancial structural mismatch——When highly depreciated computing power assets, highly volatile miner collateral, and rigid infrastructure debt are forcibly bundled, a secret default transmission chain has been formed.

1. Deflation on the asset side: The cruel revenge of “Moore’s Law”

The core logic of debt is the cash flow coverage ratio (DSCR).Over the past 18 months, the market has assumed that AI computing power rents will be as stable as house rents and even as inflation-resistant as oil.

The data is ruthlessly shattering this assumption.

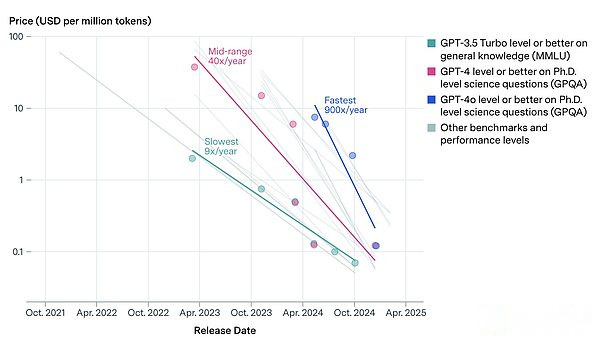

According to Q4 2025 tracking data from SemiAnalysis and Epoch AI,Unit AI inference (Inference) costs have dropped by 20–40% year-on-year in the past year.

-

The popularity of model quantization (Quantization), distillation technology (Distillation), and the efficiency improvement of dedicated inference chips (ASICs) have led to an exponential increase in the efficiency of computing power supply.

-

This means that the so-called “computing power rent” has a naturaldeflationary properties.

This constitutes the firstDuration Mismatch: The GPU purchased by the debt issuer at the high price (CapEx) in 2024 is locked in a rental yield curve that is destined to plummet after 2025.

If you are an equity investor, this is called technological progress; if you are a creditor, this is called collateral depreciation.

2. Alienation on the financing side: packaging venture capital risks into infrastructure returns

If the returns on the asset side are getting thinner, a rational liability side should be more conservative.

But the reality is just the opposite.

According to the latest statistics from The Economic Times and Reuters,Total debt financing for AI data centers and related infrastructure surges 112% in 2025, reaching $25 billion.The main drivers of this surge are “Neo-Cloud” vendors such as CoreWeave and Crusoe, as well as mining companies in transition, which adopt large-scaleAsset-Backed Lending (ABL)andProject Finance.

This essential change in financing structure is extremely dangerous:

-

past: AI is a game for technology VCs. If it fails, the equity will be returned to zero.

-

Now: AI has become an infrastructure game, and failure is a debt default.

The market is mistakenly placing high-risk, high-depreciation technology assets (Venture-grade Assets) into the low-risk financing model (Utility-grade Leverage) that should belong to highways and hydropower stations.

3. Miners’ “fake transformation” and “real leverage”

The most vulnerable link appears among crypto miners.The media likes to praise miners’ transformation to AI as “de-risking”, but from a balance sheet perspective, this isrisk stacking.

A look at data from VanEck and TheMinerMag reveals a counterintuitive fact:The net debt ratio of the leading listed mining companies in 2025 has not been substantially reduced compared with the high point in 2021.In fact, the debt of some radical mining companies has increased by 500%.

How did they do it?

-

Left hand (asset side): Still holding highly volatile BTC/ETH, or using future computing power income as implicit collateral.

-

Right hand (liability side): Issue convertible notes (Convertible Notes) or high-interest bonds, borrow US dollars to purchase H100/H200.

-

This is not deleveraging;Rollover (debt rollover).

This means the miners are playing a“Double Leverage” Game: Use Crypto’s Volatility as Guarantee to Bet on GPU Cash Flow.This is double profit during the tailwind period, but once the macro environment tightens, “currency price decline” and “hash rate rent decline” will occur at the same time..In the credit model, this is calledCorrelation Convergence, is a nightmare for all structured products.

4. The Missing Repo Market does not exist

What wakes up credit managers late at night is not the default itself, but the aftermath of the default.Liquidation.

In the real estate subprime mortgage crisis, if the bank takes over the house, it can at least be auctioned.But in AI computing power financing, if a miner defaults and the creditor takes back those 10,000 H100 graphics cards, who can they sell them to?

This is a secondary market with severely overestimated liquidity:

-

physical dependence: High-end GPUs cannot be plugged into your own computer. They rely heavily on specific liquid cooling cabinets and power density (30-50kW/rack).

-

Hardware Obsolescence: With the release of NVIDIA Blackwell and even Rubin architecture, the old cards in hand are faced withnonlinear discount.

-

Buying vacuum: When a systemic sell-off occurs, there is no “lender of last resort” in the market willing to take over obsolete e-waste.

We must be wary of this “collateral illusion” – the LTV on the books looks safe, but the secondary repo market (Repo Market) that can withstand billions of dollars of selling pressure simply does not exist in reality.

This isn’t just an AI bubble, it’s a credit pricing failure

It needs to be clarified that this article does not deny the technical prospects of AI, nor does it deny the real demand for computing power.What we question isWrong financial structure.

When deflationary assets (GPUs) driven by Moore’s Law are priced as anti-inflation real estate (Real Estate); when miners who have not truly deleveraged are treated as high-quality infrastructure operators for financing – the market is actually conducting a credit experiment that has not yet been fully priced.

Historical experience has repeatedly proven:Credit cycles tend to peak earlier than technology cycles.For macro strategy and credit traders, the top priority before 2026 may not be to predict which big model will win, but to re-examine the true credit spreads of those “AI Infra + Crypto Miners” combinations.