This article attempts to fully sort out the technical path, market structure, institutional evolution and profit logic of stablecoins, and build a panoramic framework to understand the trend of stablecoins.This article is also the first in a series of research. We will also launch research on topics such as RWA and currency stocks in the future.

Stablecoin evolution path

The birth of stablecoins is a natural result of the crypto asset system trying to solve the basic problem of “currency volatility”.Whether it is Bitcoin, Ethereum, or other decentralized assets, its openness and scarcity constitute the foundation of the digital asset system, but its price fluctuations are drastically and lacks a stable pricing anchor, making it difficult for it to play a monetary role in daily transactions and payments.The proposal of stablecoins is to build a bridge between “responsible settlement means” and “predictable currency value”.

The prototype of stablecoin,Tether’s initial attempt with the on-chain dollar

In 2014, Tether’s launch marked the first structural attempt of a stablecoin.The principle is simple and straightforward: the user transfers USD to the Tether company account, which issues equivalent USDT stablecoins on the blockchain and promises 1:1 redemption.This “fiat currency collateral + off-chain custody + on-chain issuance” model essentially outsourcing the issuance rights of US dollar deposits to private institutions, forming a business model similar to that of a narrow bank.

The key to Tether’s success lies in its first-mover advantage in the market, the network effect of on-chain liquidity, and filling the gap in the demand for USD settlement in crypto transactions.At the same time, USDT’s off-chain custody asset structure has also caused controversy. The assets it holds are not entirely cash or treasury bonds, but include commercial paper, precious metals, and even Bitcoin.Although this asset mixed structure improves the return capacity, it also leaves a regulatory gray area at the level of trust.

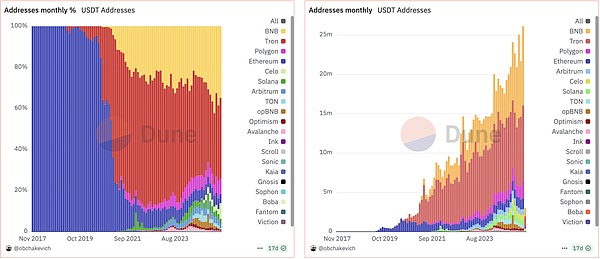

USDT launches various chain periods

The proportion of each blockchain user using USDT

With increased regulatory requirements and the market’s pursuit of transparency, the USDC stablecoin launched by Circle won favor with mainstream institutions in 2018.Unlike Tether, Circle, co-sponsored by Coinbase, operates under the regulated financial system of the United States, and its reserve assets are entirely composed of cash and short-term U.S. bonds and are regularly disclosed through third-party audit reports.USDC represents the path to stablecoin compliance and has also become an industry reference sample for the US government to promote the “payment stablecoin” compliance bill in the future.

Crypto-solidated stablecoins: The emergence of DAI and the foundation of the DeFi ecosystem

If Tether and USDC are the “centralized tokenized versions” of the on-chain US dollar, then the launch of DAI has enabled the stablecoin model under the decentralized finance (DeFi) paradigm.DAI launched by MakerDAO in 2017 no longer relies on fiat currency depositary and bank accounts, but is automatically minted and destroyed by smart contracts through on-chain pledge Ethereum assets.

The issuance of DAI relies on the over-collateralization mechanism.Users need to collateralize ETH with a value of more than 150% in order to obtain equivalent DAI and retrieve the collateral after repaying the loan.This mechanism worked well in the early stage, not only solved the demand for decentralized US dollars by on-chain users, but also became the base currency of the “interest rate market” and “leverage structure” in the rise of DeFi applications.

However, this model of ETH-centered assets faces the risks of volatility and liquidation efficiency.During the 2020 “3.12 plunge” incident, DAI faced problems such as liquidation system blockage and debt black holes, which triggered extensive reflections on the security of the model by the community.Since then, MakerDAO has added multiple collateral such as USDC, WBTC, and even real-world assets (RWA), significantly weakening its decentralization but enhancing its stability.DAI gradually transformed from a fundamentalist “crypto-collateralized stablecoin” to a “multi-collateralized synthetic dollar system”.

The rise and disillusionment of algorithmic stablecoins: a systematic warning of the UST event

While fiat-collateralized stablecoins such as Tether and USDC provide compliance and stability, while crypto-collateralized stablecoins such as DAI explore decentralization paths, another type of algorithmic stablecoin model that claims to be “no collateral” has also quickly attracted the attention of the market.This type of model attempts to regulate supply and demand through protocols and maintain currency price anchoring, thereby achieving a stable mechanism driven by pure mathematical logic.

UST in Terra system is the most representative case.UST does not rely on fiat or crypto assets to collateralize, but is anchored through a dual currency adjustment mechanism with its sister currency LUNA – when UST is above USD 1, users can mint 1 USD 1 USD mint 1 USD ; when USD 1 is below USD 1 USD 1 USD 1 USD 1 USD 1 USD 1 USD 1 USD 1 USD 1 USD 1 to achieve arbitrage hedging.However, this model has no real asset support at the bottom, and its stability depends entirely on LUNA’s market confidence.

With the expansion of Terra’s ecological incentive mechanism, the total issuance of UST exceeded US$10 billion at the end of 2021, becoming the third largest stablecoin after USDT and USDC.However, a large-scale redemption wave in May 2022 triggered the UST’s dean, and the mechanism of the protocol’s automatic issuance of LUNA failed to suppress the collapse of confidence. LUNA then entered the “death spiral”, and UST completely returned to zero.This collapse directly caused the evaporation of tens of billions of dollars of assets, and also caused the algorithmic stablecoin model to collectively “exit” in the face of global regulation.

The rise of new forms: USDe’s financial engineering and on-chain interest rate spread mechanism

The failure of UST did not end the exploration of the stablecoin model, but instead inspired the emergence of a new generation of stability mechanisms.At the end of 2023, the USDe stablecoin launched by Ethena proposed a different idea: hedge the stablecoin price fluctuations with the “Delta-Neutral” (market neutral) structure, while relying on on-chain interest rate spread income to provide support.

USDe’s issuance is based on a collateralized asset portfolio mainly based on Ethereum, combined with the strategy of shorting perpetual contracts hedging volatility risks.Users can deposit ETH, stETH or USDC, and the platform converts it into delta-neutral structured assets and issue USDe.This structure can theoretically achieve stability of net asset value through the combination of spot longs and contract shorts.In addition, sUSDe launched by Ethena allows users to pledge USDe to participate in the revenue sharing, and its annualized revenue comes from the combination of perp funding rate and stETH staking rate, which can reach 20-30%.

The key to the USDe model is its “interest generation stability mechanism” based on real arbitrage income on the chain.Instead of traditional stablecoins relying on external assets or redemption confidence, this model uses on-chain interest rate spreads as a source of reserve support, and highly binds stablecoins to on-chain liquidity and market expectations.At the same time, Ethena provides USDe with additional insurance mechanisms and redemption windows, striving to improve its systematic resilience and transparency.

The effectiveness of this model still needs to be verified periodically, especially during low funding or on-chain liquidity fluctuations.But it is undeniable that USDe has brought new directions to stablecoins: generating sustainable income through on-chain mechanisms, providing asset support with market neutral strategies, and embedding DeFi application scenarios with native protocols, representing the transition attempt of stablecoins from static “token mapping” to dynamic “return assets”.

Current market stablecoin pattern: Four major classification logic and institutional reconstruction

With the launch of the GENIUS Act, the global stablecoin market is entering a new stage of institutional reconstruction.The bill clearly regulates core issues such as issuance threshold, reserve structure, payment function, and technology companies’ participation paths, and its impact is far-reaching, no less than a “watershed event.”Under this new institutional structure, the stablecoin market has a clearer camp differentiation, which can be initially summarized into four main forces: compliance sovereigns, efficiency pragmatists, political capitalists, and the system counterattacking faction of traditional banks/tech giants.

Compliance Sovereign: USDC Alliance

Representatives: Circle (USDC), Paxos (PYUSD), Gemini (GUSD)

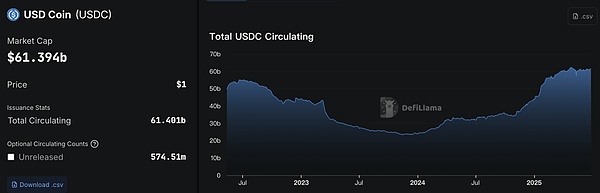

As regulations become clearer, stablecoin issuers, which are the first to adapt to the regulatory framework, have gained a first-mover advantage.Take Circle as an example. Its USDC market value was close to US$61 billion in June 2025, and its reserve structure consists entirely of cash and short-term US Treasury bonds, which meets the “STABLE Act’s requirements for reserve assets “≤93 days”.

As the representative of USDC, this type of stablecoins strictly comply with the provisions of the GENIUS Act. The reserve structure is mainly 100% cash and short-term treasury bonds, and audit reports are regularly disclosed. It is highly compliant and is welcomed by institutional customers, custody platforms and mainstream financial infrastructure.

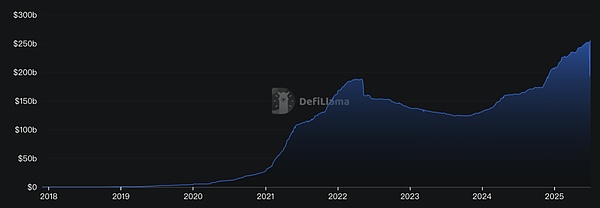

USDC total market value, source: Defilama

These issuers generally have:

-

State chartered bank or trust license

-

Monthly Reserve Audit Report

-

A clear 1:1 redeemable mechanism

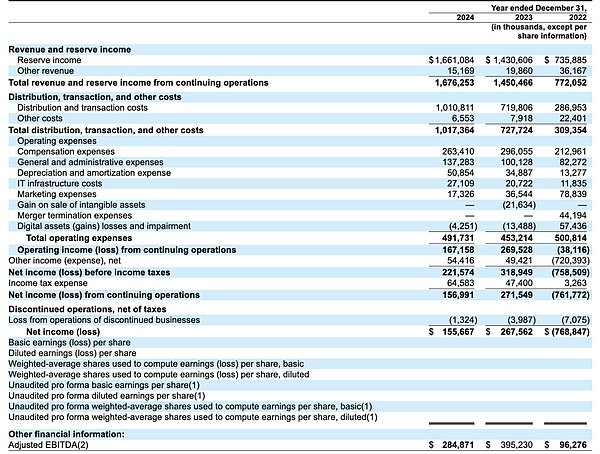

But in terms of revenue model, Circle faces the problem of high dependence on Coinbase distribution channels.It was disclosed that Circle’s full-year revenue in 2024 reached $1.68 billion, but its profit was only $167 million, mainly because Coinbase took away most of its channel expenses and marketing rewards.(The profit model of the leading stablecoin companies will be explained in detail)

In terms of income structure, stablecoin issuers can achieve billions of annualized interest income by managing reserve assets such as U.S. Treasury bonds.For example, Circle’s annual revenue reached US$1.68 billion in 2024, of which more than 99% came from reserve investment income.

Circle was successfully listed in 2025. The strategic intention behind its IPO is clear, breaking away from the single dependence on Coinbase, strengthening its independent issuance and compliance service capabilities to obtain support from more financial institutions and bank-level users.But the problem cannot be ignored – strong supervision also brings “channel dependence”. USDC (The reason for this part of the deletion and modification is that it is not right. There are many UDC transaction volumes on the chain. How could 90% of the transaction volume be driven by CB?) Most of the transaction volume is driven by Coinbase, which uses this bargaining force to suppress Circle’s profits and retain part of USDC custody rights.This structure of “compliant stablecoin × distribution oligopoly” has also triggered new risks such as centralization and platform lock-in.

Efficiency and Pragmatic: USDT Alliance

Representatives: Tether (USDT), Ethena (USDe), DAI (MakerDAO)

Tether has built a typical operating system with “loose off-chain supervision + efficient and accessible on-chain”. The USDT issued by Tether has always ranked first in the world’s stablecoins for many years. As of June 2025, the USDT circulation market value was close to US$150 billion, and its advantages lie in its ultimate efficiency and market network effect.Its reserve strategy is relatively flexible, and some of the funds are allocated to non-treasury bond high-yield assets (such as Bitcoin, gold, and private bonds), forming a “high-interest arbitrage” stablecoin.

The advantages of Tether are:

Global distribution costs are extremely low, and chains such as TRON and Solana are highly dependent on their liquidity.The reserve asset structure is more profitable (such as some Bitcoin, precious metals, and non-treasury bonds).Establish strong demand barriers for weak financial infrastructure markets such as Latin America and Southeast Asia.

Unlike Circle, Tether uses its head position to reversely harvest channel fees.Major exchanges actively connected to USDT to meet user needs, which helped Tether significantly save issuance costs, which also made its per capita profit level once surpassed traditional financial giants.

Faced with the “high-pressure regulation” of the GENIUS Act, Tether adopts a “dual-track strategy”: maintaining USDT’s flexibility in overseas markets, while also planning to launch a completely compliant new stablecoin to enter the US market.But even with Cantor Fitzgerald and has political endorsement, its “global stablecoin” model is still in the gray area in the United States.

Another category represents USDe (Ethena) and DAI (MakerDAO) and are heading towards on-chain synthesis models.DAI has transformed into a quasi-compliant hybrid model through “RWA + DSR + veToken governance”; while USDe adopts the “Share ETH + Arbitrage Hedging” model to build a “pseudo-1:1” redemption income stablecoin mechanism.

Its common characteristics are: on-chain native, interest rate sensitive, and strong composability, but there is also “policy uncertainty” – such as the “Endogenously collateralized stablecoins” clause in the STABLE Act may limit its role as a “payment stablecoin”.

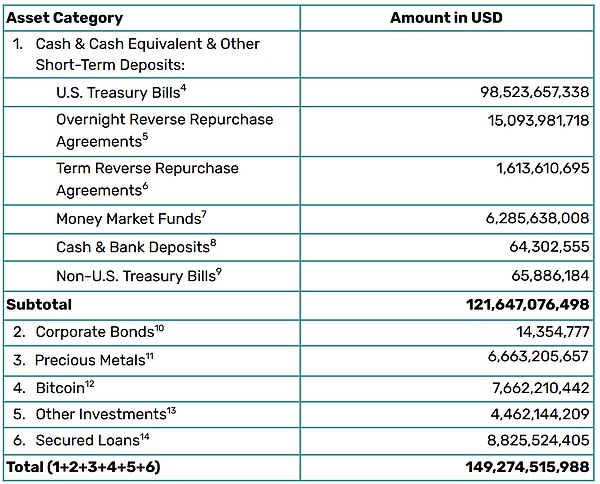

Tether Q1 2025 reserve assets composition, source: BDO audit report

Political Capitalist: USD1 and the establishment of the sovereign trading system

Representative: USD1 (World Liberty Financial)

Representatives are the USD1 stablecoin project promoted by World Liberty Financial and closely related to the Trump family.Its distinctive feature is that it relies on political resources and sovereign capital to leverage market application scenarios, such as the US$2 billion investment cooperation with the UAE sovereign fund MGX, and uses Binance Exchange to build transaction depth and liquidity.

In addition, this type of project focuses more on “scenario construction” rather than “technical breakthrough”.The arrangement with TRON chain as the issuance network and Justin Sun as the strategic consultant is a strategic combination of “technical foundation + political cover”.

Although the path of USD1 bypasses some traditional financial channels, its high reliance on political stability and the relationship between Middle East resources has also laid uncertainty for its future growth.

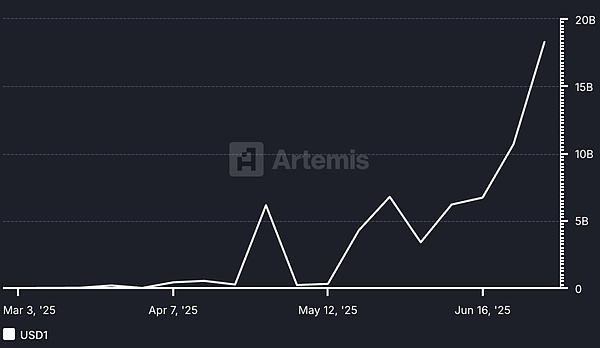

Changes in USD1’s trading volume, source: Artemis

The market structure of stablecoins: scale, participants and competitive landscape

As stablecoins evolve from crypto transaction matching tools to the infrastructure for global digital payments, their market structure is showing a more layered and differentiated pattern.From issuance model, asset reserves, circulation mechanisms to regional compliance, various stablecoins form a composite network intertwined by multiple rules systems, stakeholders and usage scenarios.

Total market volume and share distribution

Global stablecoin market value growth trend (2019–2025): The total stablecoin market value has climbed from less than US$10 billion at the end of 2019 to more than US$250 billion in the second quarter of 2025.This means it has increased by more than five times since the end of 2020, reflecting the explosive expansion of stablecoin demand and its rapid increase in position in the crypto market.

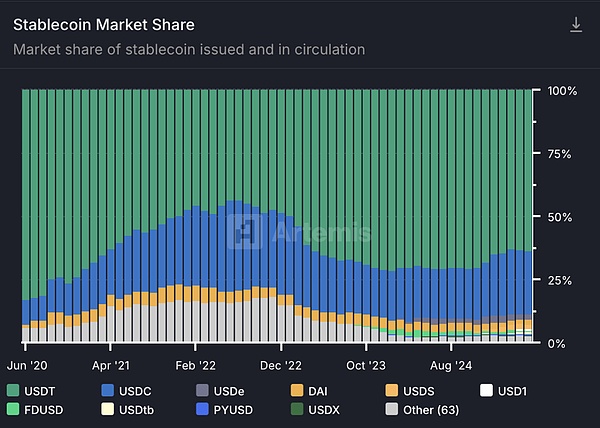

Currently, the total market value of global stablecoins has accounted for about 7-8% of the total crypto market value.Among the many stablecoins, USDT and USDC dominate, with the combined market share of more than 88% (USDT: 63.5%, USDC: 24.9%).

Among them, USDT is still the largest stablecoin, with supply exceeding US$118 billion in 2024, accounting for nearly 75% of the stablecoin market value at that time; as of mid-2025, USDT circulation further increased to about US$150 billion, accounting for about 63% of the total global stablecoin.

USDC is the second largest stablecoin, with a market value of about US$40 billion and 50 billion, accounting for about 20%.In addition, other stablecoins such as DAI, FDUSD, TUSD, USDe, and PYUSD together constitute the remaining market share, and each has formed a certain influence in specific user groups and scenarios.

Stablecoin market share structure (by market value)

As of the latest quarter, USDT accounted for about 69.0%, USDC accounted for about 20.7%, DAI accounted for about 3.1%, FDUSD accounted for about 1.7%, emerging income stablecoins USDe accounted for about 1.5%, and other stablecoins accounted for about 4.0%.It can be seen that USDT and USDC are absolutely dominant in the stablecoin territory.USDT occupies a leading position with its long-term trading network effect, extensive user trust and abundant liquidity. Its user group values its network breadth, market depth and relatively stable operational record.USDC, relying on its highly compliant and transparent reserve management, has won the favor of institutions and corporate users – for example, its reserves are audited and disclosed by licensed accounting firms every week, mostly composed of cash and short-term US bonds.This transparent compliance advantage allows USDC to gain higher trust and adoption rates in formal financial channels such as banks and payment companies.

It is worth noting that in a high interest rate environment, the issuer of fiat mortgaged stablecoins itself has also achieved considerable returns.For example, Tether disclosed that it holds approximately $97 billion in U.S. Treasury and repurchase agreements (second quarter 2024 data), and its monthly interest income is close to $400 million.This shows that as the scale grows, the stablecoin business itself is becoming an important profit center, and further strengthens the advantages of the top stablecoins in terms of capital and credibility.

Looking ahead, as global regulation gradually becomes clear and user demand continues to grow, the overall stablecoin market still has room for expansion.The news that the U.S. Senate passed the stablecoin bill in June 2025 once pushed the total global stablecoin market value to a record high of US$251.7 billion, indicating that policy favorable policies may further enhance market confidence in stablecoins.Although the market structure of mainstream stablecoins is relatively stable, the rise of new types of stablecoins (such as the endogenous USDe, etc.) is also constantly expanding the boundaries of the stablecoin market, injecting new competitive momentum into this field.

Regional distribution

The global usage of stablecoins is showing significant geographical differences.On the one hand, stablecoins have achieved “spillover” of the value of the US dollar and acted as a replacement tool for anti-inflation and US dollar in emerging markets; on the other hand, the different regulatory environments in different regions have also affected the local preferred types of stablecoins and the degree of on-chain activity.

US and developed markets: In the US, institutions and enterprises prefer compliant and transparent stablecoins due to stricter regulatory requirements.For example, USDC issued by Circle and PYUSD launched by payment giant PayPal have been adopted by many financial institutions and technology companies.On payment networks such as Visa and Mastercard, USDC is being used for cross-border clearing and merchant settlement, realizing instant payment of digital dollars.For example, in June 2025, Shopify announced a cooperation with Coinbase and Stripe to integrate USDC stablecoin payments, enabling e-commerce networks around the world to accept digital dollar payments.In these scenarios, as a closed-loop part of the compliant and penetrating payments, its transparency and regulatory filing are particularly important.Therefore, the US market is anchored by USDC, PYUSD, etc., and is dominated by stablecoins issued through the Ethereum main network and trusted banking channels.The demand for speculation and trading is relatively limited.In addition, Europe, Singapore, Japan and other places have also formulated stablecoin regulatory frameworks (such as EU MiCA, Singapore MAS regulations, etc.) to cultivate compliant local stablecoins (such as Euro EURS, Singapore dollar XSGD, etc.).The common point of these developed regions is that they emphasize the issuer’s license qualifications and reserve review, and the use of stablecoins is more reflected in areas such as B2B cross-border payments, trade settlements and wealth management, rather than personal risk aversion.

Emerging markets and developing countries: Latin America, Africa, the Middle East, South Asia and other regions have particularly strong demand for stablecoins, and are regarded as a tool for the replacement of the US dollar and financial inclusion.In countries with high inflation and depreciation of the local currency, residents and enterprises purchase large quantities of stablecoins to hedge currency declines, conduct cross-border remittances or daily settlements.According to Chainalysis data, Latin America is the world’s leading region for the real-life applications of stablecoins: 71% of the respondents use cross-border payments as the main stablecoin use, far higher than the global average of 49%.Many Latin American companies have achieved an efficient cross-border remittance experience that is difficult to reach in traditional banking systems by combining stablecoins with local payment networks.For example, Brazil received a total of approximately US$90.3 billion inflows of crypto-funded funds from July 2023 to June 2024, ranking among the forefront of Latin America.Among them, stablecoins account for as much as 70% of the crypto flows from local exchanges to overseas.As the local real currency exchange rate weakened, the transaction volume of stablecoins on the Brazilian exchange soared by 207.7% year-on-year, far exceeding the growth of Bitcoin or Ethereum in the same period.This reflects that in order to obtain US dollar exposure and avoid exchange rate risks, local companies and individuals have turned to stablecoins as cross-border carriers of funds.

In Africa, stablecoins also play a role in daily finance alternatives.Nigeria’s cryptocurrency reception amount reached US$59 billion between 2023 and 2024, of which about 85% of the funds transferred are less than US$1 million – showing that it is mainly composed of small and medium-sized retail transactions, and the grassroots adoption is extremely high.Many Nigerians bypass bank controls and store value and trade through peer-to-peer markets using stablecoins such as USDT to replace naira.The cost advantage of stablecoins over traditional remittance channels is particularly significant: through cross-border remittances, the fees can be as low as 0.1% of the transfer amount, while traditional remittance fees are often as high as 7-8%.This gap means that using stablecoins can save 98% of the remittance costs and funds arrive in almost real-time (completed in minutes), while traditional wire transfers can take 2–5 days.Taking Ethiopia as an example, after the country experienced a 30% depreciation of its local currency Bill in 2024, people flocked to stablecoins to avoid risks, driving local retail-grade stablecoins to surge by 180% year-on-year.According to statistics, stablecoins currently account for about 43% of the total crypto trading volume in sub-Saharan Africa.It can be said that in African countries with weak financial infrastructure, stablecoins provide unprecedented low-cost, fast-track means of value transmission, and are regarded as a “revolutionary” tool to improve the remittance and payment systems.

Asia and other regions: The use of stablecoins in the Asia-Pacific region is becoming more diversified, with institutional applications in developed economies and retail demand in developing markets.For example, India ranks first in the global crypto adoption index, with about 68.8% of its crypto transaction volume coming from a single large transfer worth more than US$1 million – indicating that it is mainly driven by institutions and large investors, and stablecoins are widely used in scenarios such as trade settlement and fund scheduling.In Southeast Asia, the XSGD SGD stablecoin launched by Singapore has processed on-chain transactions of more than SGD equivalent since its issuance in 2020.In the second quarter of 2024, Singapore’s stablecoin payment scale reached about US$1 billion in a single quarter, indicating an increase in interest in compliant stablecoin payments from local fintech companies and cross-border e-commerce (about 25% of which are small retail scenarios and 75% are corporate payments).Indonesia has become the emerging leader in Asia: from 2023 to 2024, Indonesia has received a total of about US$157.1 billion inflows of crypto assets, ranking third in the world, with an annual growth rate of nearly 200%.Most of Indonesia’s transaction volume is concentrated on decentralized trading platforms and token trading, but stablecoins still play an important role, helping local users save about $300 million a year in cross-border payments and preservation of US dollar.

Overall, stablecoins have a much higher penetration rate in developing countries than in developed countries.This is due to strong demand for the dollar under the pressure of exchange rate fluctuations in emerging markets and the strong demand for the dollar under inflationary pressure, and also because stablecoins lower financial thresholds and fill the gap in the traditional banking system.Research by the World Economic Forum pointed out that when the local currency depreciates, stablecoins adoption will grow rapidly – this rule has been confirmed in many places in Latin America, Africa, and Southeast Asia.On the contrary, in the United States, the European Union and other places, stablecoins are more used as tools for technology companies and financial institutions to improve payment efficiency, rather than residents’ urgent needs.Therefore, we see that the “dollar stablecoins” are spreading globally, but the methods of adoption vary from place to place: on one side, Stripe, Visa, etc. embed stablecoins into the payment link, and on the other side, Nigerian street vendors quoted goods with USDT.This imbalance in regional distribution indicates that the promotion of supervision and market education in various countries will profoundly affect the regionalization of the stablecoin pattern in the future.

Usage scenarios and ecological embedding

The application of stablecoins has long gone beyond the scope of transaction matching, deeply integrated into various financial scenarios such as payment, lending, financial management, and remittance, and has become an indispensable infrastructure component in the blockchain ecosystem.More and more multinational payment companies are incorporating stablecoins into their channels, and Visa has allowed USDC to clear some cross-border credit card transactions through the Circle platform; remittance companies such as MoneyGram also provide stablecoin cash services, allowing users in developing countries to send and receive USDC and immediately exchange local fiat currencies.In the field of e-commerce, after platforms such as Shopify integrate stablecoin payment, small and medium-sized merchants can easily receive digital dollars from overseas without worrying about the high handling fees and settlement delays in traditional collection.

Global payments and remittances

The outstanding advantages of stablecoins in the remittance scenario are reflected in two aspects: lower cost and faster speed:

Cost of handling fees:

Traditional cross-border remittances are made through bank wire transfers or remittance companies (such as Western Union), with an average fee of about 5% to 8%, and some small channels are even as high as double-digit percentages.For example, in 2023, the average remittance rate in Latin America was 5.8%, and in Africa it was as high as more than 8%.

By contrast, stablecoin remittances only require Gas fee, which in many cases are only a fixed rate of a few cents.Taking Africa as an example, the average rate of remitting $200 with stablecoins is about 60% lower than the traditional method.

Account arrival speed:

Traditional SWIFT cross-border transfers often take 2-5 working days, and they are cleared by multiple agent banks and can only be processed on working days. If there are weekends and holidays, it will be delayed for a longer time.Stablecoins are transmitted via the blockchain point-to-point and are usually confirmed within minutes.A stablecoin transfer on a high-performance chain takes only a few seconds to be recorded.

In addition, the stablecoin network 7×24 operates continuously and is not subject to time difference and business hours.This is particularly critical for small and micro families that rely on instant capital turnover.Faster settlement also reduces the risk of exchange rate fluctuations. In traditional remittances, large fluctuations in funds during the days of the journey may erode the remittance value, while instant exchange of stablecoins locks in value.

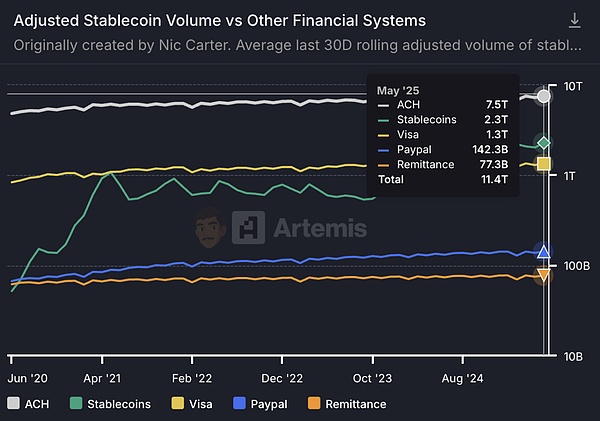

In summary, stablecoins are becoming a transformative force for cross-border remittances in emerging markets.In the past year, the number of active stablecoin wallets around the world has increased by 53% year-on-year to more than 30 million; the monthly on-chain transfer volume of stablecoins has also jumped from US$1.9 trillion in early 2024 to US$4.1 trillion in early 2025, and has processed a total of approximately US$35 trillion in value transfers throughout the year, which is comparable to or even exceeds the transaction volume of traditional international payment networks.

In Latin America, Africa, Southeast Asia and other places, many successful cases of stablecoin remittances show that their low cost and high efficiency are meeting the urgent needs of ordinary users and small and micro enterprises.Of course, the large-scale application of stablecoins still depends on the support and cooperation of regulatory authorities in various countries, especially the improvement of systems in anti-money laundering and user protection.

Source: artemisanalytics, the settlement amount of stablecoins exceeds Visa and becomes the second largest settlement architecture in the world

On-chain lending and synthetic finance

In the DeFi world, stablecoins are the most important base currency and are widely used in activities such as mortgage lending, leveraged trading and income farms.Users can deposit stablecoins into Lending protocol, obtain interest income or use them as collateral to lend other assets.Many leveraged traders amplify their positions by borrowing stablecoins, because the stablecoins price is stable and will not increase the risk of additional volatility like borrowing BTC and ETH.Stable coins are also often used as arbitrage and market maker funds: arbitrage borrows stablecoins to sell or buy assets on different exchanges to earn price spreads; market makers hold tokens and stablecoins at the same time, providing liquidity in the AMM pool to charge handling fees.It can be said that without stablecoins, there would be no today’s prosperous DeFi ecosystem.

OTC trading and over-the-counter markets

Emerging market clearing media features

Due to foreign exchange controls and fiat currency deposit and exit restrictions, OTC networks have adopted stablecoins to clear.USDT plays a “shadow dollar” role in Nigeria, Argentina, Venezuela and other countries, and is used for commodity pricing, exchange and savings.Local residents use USDT to complete payments through Telegram and other channels to form a parallel financial system.

After Nigeria implemented foreign exchange controls, it was difficult to find US dollars on the black market, so citizens turned to Telegram groups to use USDT to complete the payment of import and export payments.In high-inflation countries such as Argentina and Venezuela, residents immediately exchange the peso paid for it to USDT to maintain their value, and spend or exchange it back to paper money through point-to-point channels.It can be said that stablecoins are acting as a parallel financial system in these regions: USDT/USDC is the US dollar replacement, exchanges and wallets are bank accounts, and blockchain is the clearing network.Although this part of the transaction is largely free from traditional regulation, it meets real market demand and objectively promotes the growth of global circulation of stablecoins.

Commercial Payment and Supply Chain Finance

Multinational companies have begun to use stablecoins for B2B settlement, shortening the settlement cycle and reducing exchange costs.Cross-border e-commerce uses USDC to directly pay overseas suppliers, and mining companies use USDT to pay equipment to achieve payment in minutes.In the field of supply chain finance, stablecoins provide technical tools for accounts receivable securitization to accelerate cash reflux.Some government agencies have accepted stable currency tax payments.

Competitive pattern and ecological layout

The competition for stablecoins has shifted from stable currency value to ecological competition.USDT leads the currency trading and OTC sectors, and USDC leads in compliant payments and enterprise services.All issuers are actively expanding application scenarios: Circle provides USDC enterprise integration API, Tether invests in cross-border payment channels, and decentralized communities explore the combination of DAI and credit systems.

In summary, stablecoins are moving from the crypto circle to mainstream finance, becoming a bridge connecting different economic systems.In the future, competition will focus on who can provide more efficient stablecoin services under the premise of security and compliance.The market structure is developing towards multi-level division of labor and coordination, and stablecoins are expected to become an important financial infrastructure in the digital economy era.

The profit model of the leading stablecoin companies

Circle

Circle Internet Financial forms a core source of income with USDC reserve interest:More than 90% of Circle’s revenue comes from USDC reserve interest, and the interest mainly comes from investment in US Treasury bonds and reverse repurchase agreements, and a small part comes from bank deposit interest;

The cooperation with Coinbase allows most of the interest income to be distributed to coin-holding users in the form of “user rewards”, and this arrangement is considered a marketing expense;

By reclassifying some of the “distribution expenses” into market expenses, Circle significantly increased its book gross profit margin;

In addition, Circle’s enterprise payment network, developer API and other revenue currently accounts for a small proportion (less than 5%), but it has growth potential in the future.

Interest income composition and trend changes

Reserve interest is Circle’s absolute entity income.Circle’s revenue model is extremely simple: USD reserves obtained from issuing USDC are invested in secure, short-term interest-bearing assets, thereby earning interest income.According to Circle’s disclosure, more than 99% of its revenue in 2024 comes from interest generated by USDC reserves, which was 98.6% in 2023 and 95.3% in 2022, showing a trend of more concentrated with rising interest rates.

Specifically, Circle only had reserve interest income of US$735 million in 2022, soaring to US$1.43 billion in 2023 and further increasing to US$1.66 billion in 2024.This is mainly attributed to the surge in short-term interest rates under the Fed’s interest rate hike environment, which still drives a significant increase in interest income even if the scale of USDC circulation declines in 2023.

Reserve assets composition

US Treasury bonds are mainly reverse repurchases, supplemented by bank deposits.According to the Circle S-1 document, the company follows strict reserve management standards, 80~90% of USDC reserves are allocated to cash equivalents such as short-term US Treasury bonds and overnight reverse repurchases, and the remaining 10~20% are retained as bank demand deposits for liquidity.

Starting in January 2023, Circle will concentrate its reserves on BlackRock-managed Circle Reserve Fund, a government money market fund that is only open to Circle, which invests in U.S. Treasury bonds that mature within three months, overnight U.S. Treasury bond repurchase agreements, and a small amount of cash.For example, Circle holds an average of approximately $37.5 billion in the fund in 2024, and approximately $6.4 billion is deposited in the Global Systematic Important Bank (GSIB) deposit accounts.The bank deposits also generate interest (the average interest rate in 2024 is about 3.96%), but due to the small proportion, its contribution is far less than the interest in treasury bonds and repurchase agreements.In other words, Circle interest income mainly comes from U.S. Treasury bond interest and reverse repurchase income, while bank deposit interest accounts for only a small proportion.

Trend change: Upward interest rates drive surge in interest income

The Fed’s rapid rate hike has brought the yield on Circle reserve investment from less than 0.5% in early 2022 to around 5% in 2023.In 2022, the average Reserve rate of return will be only 2~3%, and by 2023 it will exceed 5%.Even though USDC’s liquidity declined after the Silicon Valley banking incident in mid-2023, rising interest rates still doubled Circle’s interest income.The full-year interest rate remained high in 2024 (US March Treasury bond interest rate was approximately 5.1%), and Circle reserve interest continued to grow.It can be said that during the analysis period, Circle’s revenue has benefited greatly from the macro interest rate environment: the upward interest rate “benefits” Circle’s profits, and once it enters the interest rate cut cycle, its revenue will face downward pressure.According to the sensitivity analysis of the prospectus, if interest rates are lowered by 200 basis points, Circle’s annual profit may decrease by US$414 million (equivalent to nearly 1.6 times the net profit in 2024).

Cooperation mechanism with Coinbase and USDC interest share

Coinbase is not only an important distribution channel for USDC, but also a key partner of Circle.In 2018, the two parties jointly established a Centre consortium, and initially agreed to share interest income based on the proportion of USDC issued or custodians.Under this model, “Whoever issues (or hosts) the more USDC, the more interest you get”, effectively inspires Coinbase to actively promote the adoption of USDC.In August 2023, the Centre consortium was dissolved, and Circle took over USDC governance with full authority, and granted Coinbase minority equity, and signed a new three-year cooperation agreement.

The new agreement adjusts the income distribution mechanism: Circle first extracts a small portion of issuer retention fees to cover compliance and operational costs, and then the remaining interest income is split to Coinbase in two layers:

Platform share (Party-product slice): The interest income allocated to Coinbase according to the proportion of USDC hosted on the Coinbase platform on that day; the USDC on Circle’s own platform also obtains the same proportion of income based on the proportion.

Ecosystem slice: After the above allocation, if there is still remaining income, Circle and Coinbase will each be divided into 50%, but Coinbase will need to fulfill its obligation to promote USDC (ensure that users can easily purchase USDC, integrate it into key products, and participate in policy support, etc.).

This new share arrangement means that Coinbase can obtain a considerable interest share regardless of USDC inside and outside its platform.If the proportion of USDC hosted by the Coinbase platform is higher, the more Coinbase share is divided; conversely, if more USDCs are circulated on Circle or third-party platforms, the proportion of Coinbase share is reduced.In recent years, the proportion of USDC on Coinbase platform has increased significantly, from about 5% at the end of 2022 to about 20% at the end of 2024, and to 25% as of March 2025.Coinbase has become one of the most important issuance and hosting channels for USDC, which not only brings scale growth to Circle, but also means that the majority of the revenue needs to be shared with Coinbase.

USDC interest points become a “reward” issued by users.Coinbase will share the USDC interest obtained from Circle, which is mainly used to pay USDC balance rewards (similar to the return of interest income) to users holding USDC on its platform.This is essentially Coinbase subsidizes users’ currency earnings with its own income to increase the attractiveness of USDC to users.For example, Coinbase increased the annualized reward for USDC holding by ordinary users to nearly 5% in the second half of 2023, significantly stimulating USDC’s retention and growth on its platform.In accounting, Coinbase regards such USDC user rewards as marketing expenses and is classified as sales and marketing expenses accounts.Coinbase’s USDC user reward expenditure reached US$224 million in 2024, a 542% increase from US$34.94 million in 2023.Coinbase explained that increasing the USDC reward rate is intended to enhance customer acquisition, retention and platform participation, and is a marketing investment.Therefore, although this part of the interest comes from USDC reserves, it is ultimately regarded as Coinbase’s marketing cost in the form of “user rewards”.

Coinbase will benefit greatly in 2024.As USDC interest income soared, Coinbase’s share amount rose.According to the prospectus, Circle confirmed a total of US$1.017 billion in “distribution, transaction and other costs” expenditures in 2024, of which approximately US$908 million were paid to Coinbase.

In other words, about 54% of Circle’s total revenue was transferred to Coinbase as a cooperation share.This figure was approximately US$248 million and US$691 million in 2022 and 2023, respectively, corresponding to 40% and 50% of the annual revenue.It can be seen that Coinbase is gaining an increasing share of revenue in the USDC ecosystem with its strong user base and distribution capabilities.Some analysts pointed out that after deducting the rewards issued to users, Coinbase’s net income from USDC business even exceeded Circle itself.This highlights Coinbase’s strong position in the USDC ecosystem: it is not only a “rainmaker” for Circle’s revenue growth, but also a “toll station” for profitability.

Distribution cost classification reduces reported gross profit margin

Circle classifies the channels related to USDC issuance and circulation expenditures as “distribution and transaction costs”, which are directly included in operating costs and deducted from revenue.The $908 million share paid to Coinbase in 2024 and the $74.1 million strategic fees paid to Binance were processed in this way, resulting in the company reporting gross profit margin of only 39%.

These distribution expenses are economically essentially user acquisition costs and are marketing expenses.If reclassified as marketing expenses rather than sales costs, Circle’s gross profit margin would be close to 100%, because there is almost no direct cost to obtaining interest income itself.However, regardless of the accounting classification, Circle still needs to distribute more than 60% of its revenue to its partners, and the proportion of distribution costs has increased from 40% in 2022 to more than 60% in 2024.

Edge Revenue: Enterprise Payment Network and API Services

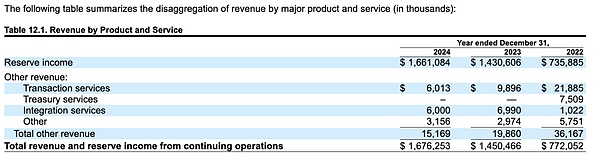

Other income currently accounts for a limited proportion.In addition to reserve interest, Circle also has a small amount of revenue from transactions and infrastructure services, i.e. “Other income.”This includes providing enterprise customers with fee income from payment of settlement, digital wallets, block linking and other services through APIs, as well as technical service fees charged when assisting the integration of USDC in the new blockchain.However, for now, this part of the revenue is very small.

The prospectus disclosed that in 2024 and 2023, Circle’s other products revenue only accounted for 1% of total revenue, and in 2022 it also accounted for only 5%.In terms of amount, other income in 2024 is about $36.17 million, a drop in the bucket compared to the total income of $1.676 billion. Circle has not effectively escaped its single dependence on interest income.

Prospects for development potential

The market has high hopes for Circle to expand revenue beyond interest.Investors expect Circle to make substantial progress in cross-chain bridge CCTP, merchant payment, enterprise API and other fields, thereby “improving revenue quality.”According to Tanay Jaipuria’s analysis of S-1, the public offering market has implied that Circle will achieve double-digit USDC circulation growth in the future and gain significant traction on paid products.Management also stated that it will continue to invest in the development of new products and gradually diversify revenue.However, as of the beginning of 2025, these marginal incomes were still in the incubation period and had limited contribution to overall performance.Circle’s short-term performance fluctuations will still mainly depend on USDC interest income. Only by deepening the stablecoin ecosystem and providing differentiated value-added services can we gradually increase the proportion of non-interest income and enhance business resilience.

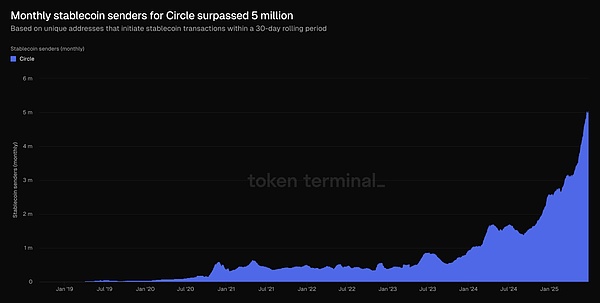

Incremental curve for USDC users, source: Token tetminal

Tether

U.S. bond interest income

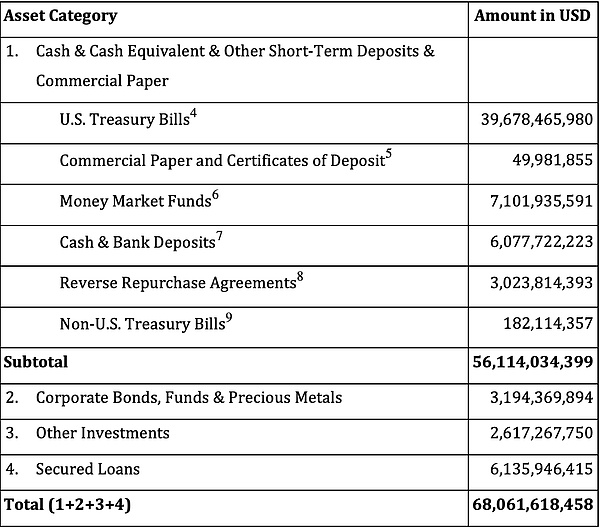

Tether’s main revenue is currently derived from interest generated from large amounts of U.S. Treasury bonds held by its reserves.As the Federal Reserve raises interest rates to boost U.S. Treasury yields, Tether’s short-term U.S. bond portfolio has become its core source of revenue for “low-risk, high-yield” in recent years.

Currently, Tether directly holds US Treasury bonds, while holding US$6.286 billion in money market funds, while holding US$4.885 billion in funds; while in the overnight reverse repurchase agreement, US$15.094 billion in US Treasury bonds as collateral reached US$15.087 billion.

Tether’s U.S. Treasury exposure to:

-

Directly held US Treasury bonds amounted to US$98.524 billion

-

Indirect holding (via money market fund): USD 4.885 billion

-

As collateral control: $15.087 billion

-

The total of approximately $118.496 billion is related to U.S. Treasury bonds, accounting for approximately 79.4% of the total reserves of $149.275 billion.

In the first quarter of 2024, Tether announced a record-breaking net profit of US$4.52 billion, of which approximately US$1 billion came from US Treasury interest income.This figure has increased significantly compared with the previous quarter, reflecting the role of rising U.S. Treasury interest rates combined with the expansion of Tether’s reserve scale.In a high interest rate environment, Tether’s single-quarter interest income has exceeded the order of billions of dollars.

Revenue for redemption and transaction fee

Tether also receives a certain fee income through the issuance and redemption of stablecoins.According to its regulations, the minimum amount of a single transaction for subscribing or redeeming USDT directly on the Tether platform is US$100,000, with a redemption fee of 0.1% (at least $1,000) and a subscription fee of 0.1%.These fees not only meet the institutional large redemption needs, but also provide Tether with stable cash flow.During a period of severe market fluctuations, large redemptions were converted into company revenue: for example, during the crypto market turmoil in 2022, Tether redeemed more than $20 billion in redemptions in just a few weeks and kept the redemption stable (the redemptions in the second quarter alone brought tens of millions of dollars in handling fees for the company).

In addition, the frequent use of USDT transfers and transactions by users in multi-chain environments also reflects its value as a crypto market infrastructure.According to statistics, as of April 2025, Tether’s cumulative revenue this year has been approximately US$1.46 billion, significantly higher than other blockchain platforms (Ethereum revenue was approximately US$157 million during the same period, and USDC issuer Circle’s profit was approximately US$620 million).Overall, compared with huge interest income, the redemption/transaction fee is a secondary but stable revenue supplement, reflecting the widespread use of USDT in transaction settlement.

The evolution of asset allocation and profit model

Tether’s profit model is closely related to the composition of its reserve assets, which underwent significant adjustments at different stages:

Early Stages (2019–2021)

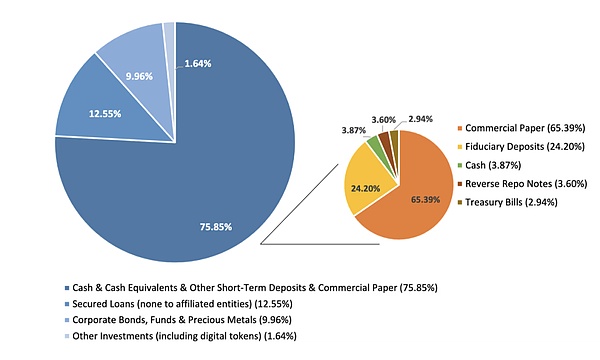

In a global low interest rate environment, in order to increase returns, Tether has allocated a large number of credit assets and high-yield investments in its reserves, with a low proportion of US dollar cash and treasury bonds and a high proportion of risk assets.Take the reserve details first disclosed in March 2021 as an example (at this time, the audit was provided by Moore Global, a Caribbean audit company with only 5 employees): Only 2.94% of the reserves are U.S. Treasury bonds, 49% are made up of relatively poor liquid commercial paper, and the rest are mortgages (12.55%), corporate bonds and precious metals (9.96%), and other investments (1.64%, including a small amount of digital currencies).

At that time, the interest rate of US Treasury was nearly zero. The company gained additional returns by holding short-term credit assets such as commercial paper and corporate loans, but also assumed higher credit and liquidity risks.At this stage, Tether’s revenue structure can be described as a “high risk, low interest rate” model: limited interest income, mainly relying on return on venture capital and profitable transaction fees for stablecoin business, and also faces market doubts (such as the lack of independent audits in the early stage, opaque quality of commercial papers, etc.).

Tether reserve structure for this stage:

-

Commercial paper accounts for 65.39% of cash and cash equivalents

-

U.S. Treasury bonds account for 2.94%

-

Guaranteed loans account for 12.55% of the total reserves

-

Corporate bonds and precious metals account for 9.96%

-

Other investments (including digital currencies) account for 1.64%

Transformation phase (2022)

Faced with regulatory pressure and industry concerns about reserve security (events such as the TerraUSD collapse triggered a review of the quality of stablecoin reserves), Tether significantly adjusted its asset allocation in 2022.The company gradually reduced its holdings of commercial paper and announced in October 2022 that commercial paper had been cleared, turning to cash equivalents such as U.S. Treasury bonds and bank deposits.

BDO’s forensic report shows that at the end of September 2022, Tether held approximately US$39.7 billion in U.S. Treasury bonds, accounting for more than 58% of the total reserves; at the same time, 82% of the assets are “highly current” assets such as cash, cash equivalents and short-term deposits.This adjustment greatly reduces the credit and liquidity risks of reserves.

In the fourth quarter of that year, despite the sharp decline in the crypto market, Tether still achieved a net profit of more than $700 million.The source of profit has begun to shift to interest income. As US bonds account for more than half and interest rates rise, the company’s quarterly profits have increased significantly.This profit model can be summarized as “reducing risk exposure and steadily spending the winter.”On the one hand, increasing the proportion of US debt ensures redemption liquidity and asset security, and successfully withstood the test of large redemption of about US$20 billion in the second half of 2022.On the other hand, the interest income brought by the Federal Reserve’s interest rate hike has gradually replaced the previous high-risk investment returns and become a new engine for profit growth.

Current stage (2023 to present)

Starting from 2023, Tether’s asset structure will further tilt towards conservative and high liquidity, and benefit from high interest rates and significantly improve profitability.As of the end of 2023, Tether’s reserves of China-US bonds and cash equivalents have exceeded 82%; it reached more than 90% in the first quarter of 2024, setting a record high.In other words, most of the reserve assets are low-risk assets such as US short-term Treasury bonds, money market funds and bank deposits, and the proportion of high-volatility investments (such as Bitcoin and gold) has dropped to about 10%.

Such an asset structure has brought rich and stable returns in the interest rate upward cycle. Tether made considerable profits in all quarters in 2023, with an annual net profit of about US$6.2 billion; at the beginning of 2024, there was even a surge in profits in a single quarter, with a net profit of US$4.52 billion in the first quarter of 2024, which is not only due to the huge interest income of US Treasury in the quarter, but also the additional benefits provided by the rise in the price of assets such as Bitcoin.

The proportion of U.S. bonds in reserves jumped from less than 3% in 2021 to about 82% in 2024, and profits have also increased year by year.Tether’s return model model changes from “high risk and low return” to “low risk and high return”.This change not only increases the total profit, but also greatly improves the sustainability and stability of profits.

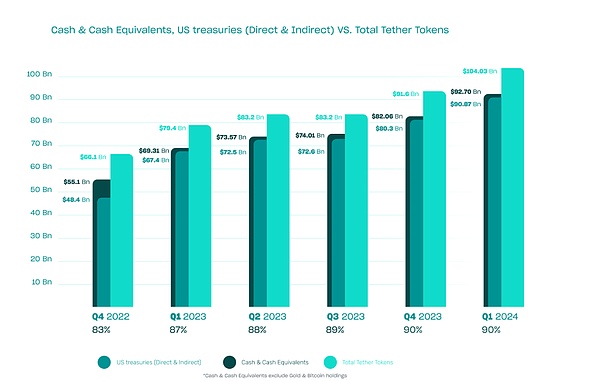

Figure: Tether reserve assets composition from 2022 to 2024.

The above figure shows the proportion of different asset classes in each quarter, from deep to shallow: cash reserves, US Treasury bonds (direct or indirect holdings), and the total amount of Tenther tokens, indicating that the proportion of US debt has increased significantly since 2022.

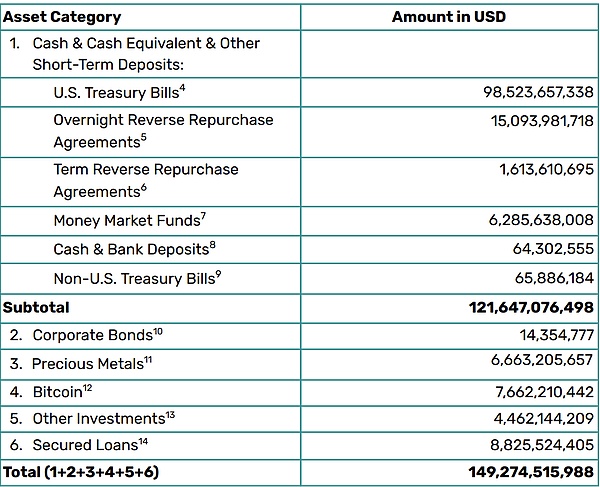

This optimized asset allocation has allowed Tether’s total profit to climb, while significantly improving the stability and sustainability of profits.By the end of the first quarter of 2025, Tether’s reserve assets had increased to approximately US$149.3 billion, with circulating USDT reaching US$143.6 billion; of which nearly US$120 billion were invested in US Treasury bonds (including direct holdings of approximately US$98.5 billion and indirect holdings of approximately US$23 billion through repurchase agreements and funds).

Source: Tether’s first quarter financial report for 2025

In the first quarter of 2025, USDT’s circulation increased by another US$7 billion month-on-month, and the number of user wallet addresses increased by about 46 million.Tether achieved operating profits of more than US$1 billion in the quarter, mainly from US Treasury investment income; in terms of risky assets, the income from gold holdings basically offset the impact of price fluctuations in crypto assets such as Bitcoin, and did not significantly drag or boost net profit.

Comparing the first quarter of 2024 and the first quarter of 2025, it can be found that the former has huge book returns due to the sharp rise in the crypto market, while the latter returns to the “normal” profit dominated by interest income.This shows that Tether’s current profits mainly rely on expected interest returns, while additional fluctuations caused by risky assets are secondary and intermittent.

UST+USDe’s profit model

In the development path of algorithmic stablecoins, UST is a landmark case and a representative of the industry’s early large-scale experiments on the “unsecured monetary policy model”.Its core architecture relies on a long-term commitment to Anchor Protocol’s annualized 20% income, which is not based on real spreads or on-chain profitability, but is a subsidized system supported by the Terra Foundation, the LUNA additional issuance mechanism and external financing subsidies.

UST itself does not create actual returns, but instead meets users’ expectations for interest by constantly injecting new capital, thus building a financial structure that seems stable but is actually highly dependent on incremental funds.In the Anchor protocol, a large number of users just deposit UST and wait for high returns, while the protocol does not have a clear lending target or asset return path, forming the illusion of “subsidies are income”.When user confidence is shaken and large amounts of redemption, LUNA is forced to mint depreciation tokens to cope with the pressure of exchange, thus entering an irreversible “death spiral”, causing the entire system to collapse in a short period of time.Anchor’s so-called 20% annualized income is actually an advance for future ecological development, rather than any real and sustainable commercial profit.Once users start selling UST, casting LUNA to redeem USD, the LUNA price will collapse, and this is the source of funds for the subsidy system, forming a fatal self-destruction chain

Anchor’s 20% annualized earnings initially came from Terra Community Reserve Pool (raised by LUNA Financing) and subsequent infusions by institutional investors such as Jump Capital.

Under this model, users get high returns, but the agreement continues to burn money.It is not the user who pays for the gains, but the losses are borne by the LUNA holders and the Terra Foundation.

USDe attempts to build a synthetic stablecoin system that does not rely on US dollar reserves through the hedging structure of delta-neutral.In the Ethena protocol, while the user pledges ETH or stETH to mint USDe, the protocol will open equivalent short positions on centralized exchanges or some on-chain perpetual platforms, trying to achieve price stability through the profit and loss hedging between spot and derivatives.

In this structure, the stability of USDe does not come from asset guarantees, but from capital hedging. When the prices of assets such as ETH fluctuate, the floating profit/float loss of the collateralized assets is offset by the contract profit and loss, achieving an approximate “risk-neutral” state, which makes USDe a “synthetic dollar” that does not rely on reserves, and its stability comes from hedging logic rather than reserve guarantees.

If users want to obtain additional benefits, they can convert the USDe in their hands into sUSDe and participate in the agreement spread distribution.The source of income is mainly the funding rate obtained by short positions in the perpetual contract market, that is, when long funds are more active, the reverse subsidy for short sellers becomes the interest source for holders.On the other hand, the proceeds come from the interest or handling fees paid by the mortgagee, and the agreement design level redistributes the systemic surplus to the sUSDe holders.

Core logic of the income model: AUM (USD value of assets deposited by users in the agreement smart contract) × Aerobic annualized interest rate

Funding rate difference: While the agreement opens short orders in the perpetual market and hedges ETH fluctuations, when the market demand is strong (normal), the funding rate paid by the longs to the shorts becomes the agreement revenue.

Mortgage fee/interest spread: USDe holders convert it into sUSDe, and can obtain the interest rate spread income of the agreement layer.

Vault Product handling fee: Institutions access the hedging path through customized strategies, allowing institutions to directly hedge with the futures market, increasing the efficiency of capital utilization and strengthening the handling fee income logic of the agreement layer, which is a relatively stable part of its profit model.

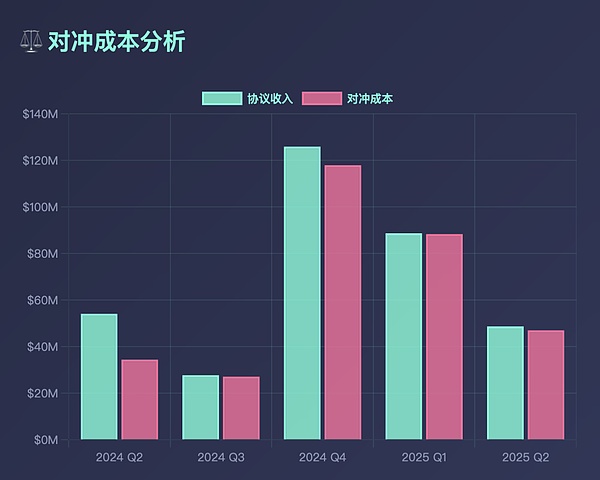

According to Token Terminal data, from Q2 2024 to Q2 2025, USDe’s AUM experienced a volatility from $2.7 billion to $6.6 billion, with a growth rate of 144.6%.Quarterly earnings fluctuated significantly, from $47 million to $126 million at one point, and then retreated to around $48 million.

Even so, its annualized arbitrage interest rate has always maintained a cyclical structure within the range of 3%~15%, which means that Ethena does not rely on arbitrage on a fixed exchange or node, but has built a relatively stable arbitrage strategy system, but the yield has market dependence on the structural bull market.

Although this model has made essential progress compared to UST, it still has a high dependence on the depth of the derivatives market, the positive sustainability of the capital expense rate, and the liquidity of market makers.When the derivative funding rate reverses, or the market fluctuates too much and the hedging fails, USDe may also collapse.Therefore, “stable returns” actually rely more on the interest rate spread dividends in the overall structural bull market, and it is still difficult to say that it is completely sustainable.

USDe’s hedging costs have remained high

From the perspective of profit model, UST’s so-called income relies more on additional issuance, subsidies and narrative stacking, which is a risk model that lacks a closed loop of real transactions; while USDe tries to rebuild the “credit” of algorithmic stablecoins with stronger financial engineering design, but its fundamental income is still limited by the bull market capital premium and hedging market structure.The comparison between the two not only represents the rise and fall of algorithmic stablecoins, but also outlines that in the innovation of stablecoin architecture, the real challenge comes from the unity of stability mechanisms and income mechanisms.

Stablecoin innovationTraditional banks andIts downstream

Inclusive finance, which has been discussed in a few years, allows more down-to-earth users to enjoy financial services such as bank wealth management/loaning/insurance.Why did China attach so much importance to inclusive finance at that time and once wrote inclusive finance into the 13th Five-Year Plan?——This is because the country needs to allow groups that were originally ignored by the mainstream financial system (such as rural residents, self-employed businesses, small and micro enterprises) to enjoy basic financial services, such as loans, deposits, insurance, etc.; finance is a resource allocation tool, and if it only serves the top groups, it will aggravate the gap between the rich and the poor.Inclusive finance can spread financial dividends to the middle and lower levels and enhance economic resilience.The core is that the CAC (customer acquisition cost) of traditional finance is actually very high, which leads to traditional banks/insurance/securities and other financial institutions being unwilling to reach down-to-earth users.But stablecoins are completely different. The CAC of stablecoins is 0, because all back-end work is done through blockchain. Due to the network effect, Circle does not need to open an online store in remote county towns to attract customers and open accounts.New users obtain USDC through OTC or C2C.

Secondly, stablecoins are more permissionless than traditional banks, with higher composability/privacy.Any USDC user can conduct permissionless financial management/borrowing/payment on the chain.

This has led to stablecoins reshaping traditional banks and the downstream industries of traditional banks.What is happening now is that stablecoins are reshaping the central bank (Tether/Circle, CEX is reshaping traditional exchanges and commercial banks (Binance/OKX/Coinbase), asset management companies are reshaping private banks (Amber/Matrixport), and stablecoin tripartite payment companies are reshaping traditional cross-border payment companies (Bridge).In the future, more downstream industries of traditional banks will be reshaped. In addition to the above, what we see now may be reshaped by securities companies, insurance, etc.

Ending

Stablecoins are evolving from “dollar digital mapping” to digital assets with native returns and globally common. Driven by the dual promotion of institutional reconstruction and technological innovation, they have gradually replaced some traditional financial functions and become a key infrastructure for cross-border payments, asset management and financial inclusion.Its reshaping traditional roles such as central banks, commercial banks, payment institutions and even securities and insurance has just begun.