Since the global financial crisis created by Wall Street in 2008, criticism and controversy over the traditional financial system have never stopped in all sectors of society.As we all know, the real financial system centered on the traditional banking system has problems that are difficult to eradicate. Whether from different perspectives such as composability or capital allocation efficiency, entry threshold and transparency, traditional finance cannot meet the demands of today’s era.While the Internet and blockchain industries are making rapid progress, the financial industry is like an old train that stays in the steam engine era, not only old-fashioned but also staggering.

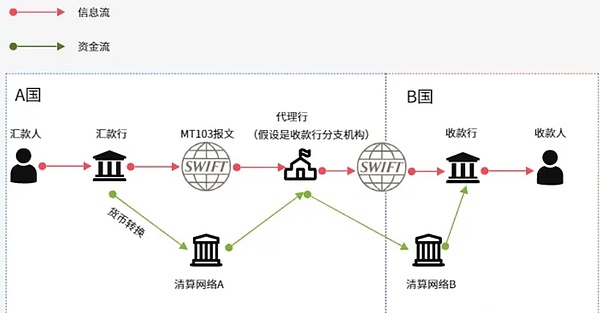

Ultimately, the technical and management backwardness of the underlying facilities represented by the traditional financial system represented by banks, securities and derivatives markets is the main cause of all problems.Taking the well-known SWIFT system as an example, since funds transfers require multiple intermediary agencies (similar to the routing process of Bitcoin Lightning Network), most cross-border transfers often take 1-5 days or even longer. Although the improvement measures in 2017 have compressed half of the transfers to 30 minutes, they still have not gotten rid of the high handling fees and dependence on multiple intermediary agencies;

(Picture source:

https://mirror.xyz/0x061DE2457ABe5d621E89FDFf28EB983468a5A2eD/6uR_uCSEURjGP_Y1yo9P_1E2JtURVmQDVQD1MZvIpYY)

In contrast, Ethereum, Tron, Solana and other public chains have achieved a set of decentralized distributed networks in the underlying architecture, which can quickly verify and synchronize data in a short period of time, fundamentally changing the cumbersome and inefficient asset verification and settlement methods in traditional cross-border transfers. While de-mediated, they can already achieve payment in seconds, which is basically a world of difference from SWIFT.

Inefficiency is not the only problem of SWIFT. The EU and the United States have repeatedly regarded SWIFT as a “financial nuclear weapon” and wantonly wield big sticks to attack enemy countries with their own control over SWIFT.Putting aside Iran, which suffered SWIFT sanctions twice in 2012 and 2018, the EU and the United States put pressure on SWIFT member banks during the 2022 Russian-Ukraine War alone, relying on the ban to deprive Russia of its ability to make international transfers through SWIFT, seriously limiting the latter’s trade activities and capital transfers.Regarding this,Russia has even completely changed its attitude towards cryptocurrencies and passed a bill to legalize cryptocurrencies such as Bitcoin in response to financial sanctions in Europe and the United States.

SWIFT is just the tip of the iceberg of the traditional financial system.The wide variety of trading activities in traditional finance generally have problems such as bloated processes, inefficient capital utilization, and excessive entry thresholds.First of all, most traditional financial transactions rely on special clearing institutions for settlement. Many transactions follow the T+1 or T+2 settlement cycle. Funds will be locked within 24 to 48 hours before liquidation, seriously hindering the flow of funds. However, in all-weather trading and in a high volatility market, instant liquidity is crucial, and settlement delay is a fatal problem.

In addition to settlement delays,The access method of traditional financial markets is highly exclusive. Many financial products require investors to meet financial and legal thresholds, shaping a system that only high-net-worth individuals and institutional investors can participate. Moreover, large institutions can conduct over-the-counter trading, bypass large exchanges and obtain better liquidity. These opportunities basically have no room for ordinary people to participate.

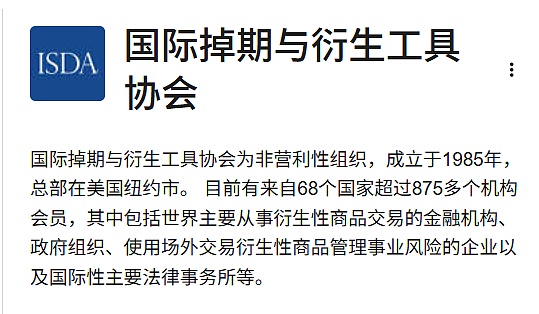

Cases in this regard include the ISDA (International Swap and Derivatives Association) agreement.Today, the ISDA agreement covers the global derivatives market with a scale of over $500 trillion, providing a complete set of standardized rules on counterparty risks, mortgages and settlements to ensure that financial institutions can trade derivatives under legal protection.However, the process of the agreement requires a lot of legal and bureaucratic processes, and only professional financial institutions can participate.

In addition, the ISDA protocol also includes a large number of manual processes, and the processing speed is comparable to that of a turtle.In the DeFi ecosystem, smart contracts can complete transactions in seconds according to predefined logic, which is almost the difference between Rockets and Snails.

Although many institutions introduce automation into traditional financial workflows, they still cannot match the Defi platform in terms of efficiency.In addition, the machineThe separation of inter-agricultural fluidity is also a big problem.A large amount of funds are stored in isolated fund pools of various institutions, showing a highly fragmented state.This fragmentation confines capital, liquidity and risk to the local market, affects the optimal allocation of resources, and makes it difficult to achieve extremely efficient liquidity utilization and transfer.

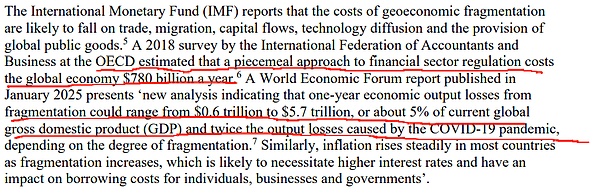

According to a 2018 survey by the OECD (International Federation of Accountants and Business) estimates that liquidity fragmentation causes about US$780 billion in global economic losses each year. The World Economic Forum predicts that liquidity fragmentation can cause losses to economic output by US$0.6 trillion to US$5.7 trillion (about 5% of global GDP) in one year, which is twice the output losses caused by the new crown epidemic, depending on the degree of fragmentation.

The root cause of liquidity fragmentation is that the asset conditions of different institutions and banks are seriously opaque and the trust costs are extremely high, which greatly hinders liquidity sharing among institutions.In addition, regulatory differences, geopolitical factors and market structures in different regions jointly hinder the efficient call of liquidity, and the consequence is the inefficiency of the global financial system.

Although liquidity fragmentation has also plagued the Defi ecosystem for a long time, due to the highly transparent asset distribution on the chain, anyone can judge the liquidity status in different platforms and pools at a low cost, which is conducive to real-time interaction between Defi projects and can solve the problem of fund fragmentation more smoothly than traditional finance.It has emerged in recent yearsIntent (user intention) and global liquidity protocols basically realize efficient calls to fragmented liquidity.

Intent-type projects can pre-statistic data, evaluate the distribution of assets in different public chains and different liquidity pools, estimate the slippage and handling fees of different pools, and finally split a large-value transaction into multiple small-value transactions, and complete them in multiple pools to obtain the best trading experience.Although this solution does not change the fragmented distribution of liquidity from the bottom layer, it simulates the effect of global unified liquidity on the user side by optimizing the transaction achievement path.

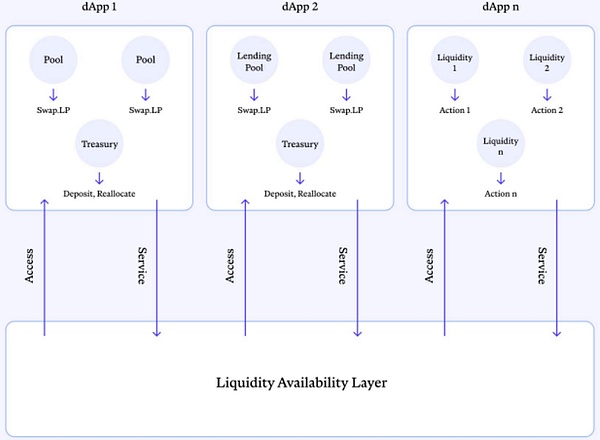

The liquidity availability framework and supporting components currently being developed by INJ public chain will try to fundamentally solve the liquidity split problem by building a unified liquidity pool and transaction matching engine for all on-chain financial platforms.

From a model perspective, this form of placing liquidity in a unified and centralized manner and allocating instant liquidity to different dApps through specific algorithms is very novel. It is an innovation in the way of liquidity utilization directly at the bottom of the chain, and the foundation of all this is based on data transparency and rapid transaction settlement.

Efficient utilization of liquidity is only one of the benefits of data transparency, and the greater benefit is that it can provide security for market participants and the entire financial system..In contrast, traditional finance with severe opaqueness is simply riddled with holes, and the collapse of Lehman Brothers in 2008 highlighted the systemic risks in the opaque financial system.

As a mainstream broker, Lehman frequently remorts client collateral to quickly raise funds. The leverage ratio in its balance sheet is as high as 16 times, becoming a huge powder keg that can be detonated by Mars. Neither the opponent nor the regulator could understand these details in a timely manner, which eventually triggered a chain reaction.In order to absorb the financial tsunami caused by the subprime mortgage crisis, the global financial system maintained a low interest rate policy for more than ten years since then. To this day, the side effects of maintaining low interest rates for a long time on the economies of various countries are still evident.

Although countries have been more strict in supervision of the banking system after 2008, the main brokerage business remains structurally opaque, and collateral flow, margin exposure and leverage ratios are still managed internally by financial institutions rather than transparent and auditable.The 2023 Silicon Valley bank bank bank collapse fully demonstrates that an opaque banking system can never avoid moral risks.In today’s Defi system, although it is impossible to completely eliminate the evil of financial platforms, the possibility of the project party doing evil has been greatly reduced with the strong on-chain data monitoring.

However, for the past Defi ecosystem, although it has a lower threshold, de-mediated and transparent data than the traditional financial system, can achieve second-level settlement and efficient use of liquidity, it still does not show the positive externalities it should be. In the final analysis, Defi is basically decoupled from real economic activities, always being self-entered in its own closed circle, and cannot have in-depth interaction with the traditional financial system.For a long time before 2024, many people had doubts about the true value of Defi, believing that this is just a self-entertainment in the blockchain circle and has no other use except speculation.

However, in fact, this is not a problem with the Defi project itself. The fundamental reason is that traditional financial assets are not circulated on the blockchain in a suitable way.The RWA concept that has been popular since 2024 has announced the combination of Defi and traditional finance, effectively binding the two.

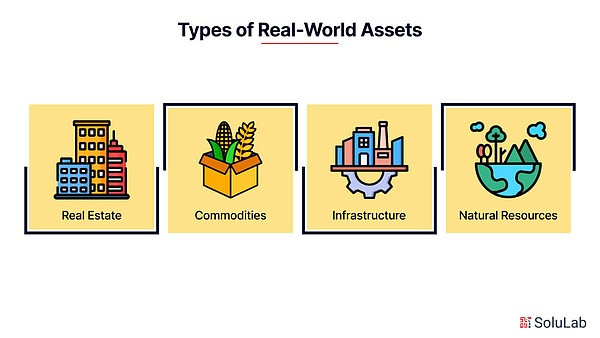

So, what exactly is RWA?What types of them are there?RWA’s full name is Real World Assets, which refers to tokenized real-world assets, such as bonds, stocks, crude oil, etc., by establishing ownership binding between on-chain tokens and off-chain real assets.RWA can use blockchain to achieve a more efficient and transparent transaction experience.In theory, all assets can be RWA, and all physical and virtual assets such as real estate, patents, and data can be circulated on the chain. Behind this is a rapidly expanding trillion-level market.

According to Boston Consulting Group (BCG) forecast, the market size of RWA assets is expected to reach $16 trillion by 2030. What is even more exaggerated is that BlackRock CEO Larry Fink said that BlackRock’s goal is to tokenize about $110 trillion in stocks and bonds and identify Ethereum as the preferred platform for stablecoins and DeFi applications.Fink expects RWA funds will eventually become as popular as exchange-traded funds (ETFs).

There is no doubt thatA financial revolution is breaking out, and the existing global financial landscape will be subverted.This means that many assets with poor liquidity can be highly monetized with the help of RWA, thus opening the 3.0 chapter of Finance after Internet finance.

Some people may ask, how meaningful is all this?To answer this question, we can look at the three major processes in the historical evolution of asset financialization, which are: capitalization, securitization, and monetization.The so-called capitalization is the process of promoting asset appreciation.For example, land and houses can be turned into capital by renting them and become an interest-producing asset, which is the capitalization of land and houses.For example, cash itself cannot generate interest directly, and it is turned into interest-producing assets through lending. This is the capitalization of cash.Capitalization of assets is the foundation of commercial banks and the credit market, and this process opened up the earliest financial industry.

The invention of a series of financial instruments such as bonds, annuities, and stocks symbolizes the securitization of assets.There is no essential difference between capitalization and securitization, but there are differences in asset patterns and liquidity.For example, the IOU you get after lending money to others is non-standardized and difficult to trade and circulate, but if it turns it into a bond and becomes a standardized asset and has strong liquidity, you can trade freely in the market.

Compared with capitalization, securitization has the characteristics of quota, standardization and strong liquidity.In the past, the most successful securities were stocks, bonds, funds, insurance, REITs, etc. The emergence of these things gave birth to the prosperity of investment banks and capital markets.

In addition to securitization,The ultimate form of assets is monetization, which is a more liquid way of asset financialization than securitization.The simplest example is the difference between US Treasury and US dollar.Once the assets are highly monetized, they will become an excellent asset comparable to mainstream currencies and have more advantages than simple securitization.The emergence of RWA indicates that all physical and virtual assets in the world can be monetized. If intellectual property rights and other assets that could not fully release their economic value in the past achieve low cost, instant settlement, and wide access, they will directly rewrite the history of the entire global economy, and many problems will be solved.

(Photo source: ChainUP)

Of course, those familiar with the finance industry might say that many assets had the ability to monetize before the emergence of RWA, but the problem is,Assets in the traditional financial system cannot achieve high monetization due to problems such as high intermediary costs, insufficient liquidity, excessive entry threshold and low transparency.

For example, in real life, monetize utility assets in higher education institutions is extremely difficult, and many American universities (such as Ohio State) monetize assets by selling or outsourcing utility systems (such as hydropower systems) to relieve budgetary pressure.Typically, they sell utility systems to third-party consortiums, but this process involves complex contract negotiations, valuation disputes and reviews, transaction cycles are often several years and intermediary fees are extremely high.Even if monetization can be achieved in the end, it will only obtain poor liquidity and will not attract the full participation of retail investors or high-net-worth individuals. The counterparty is limited to institutions, which seriously restricts the full release of asset value.

The Defi-based RWA market can help physical assets achieve a high degree of monetization with low thresholds and extensive mass participation, and the significance behind it is of great significance.Wall Street, which has always had a keen sense of smell, naturally understands the value of Defi and RWA systems.Cathie Wood, founder of ARK Invest, once regarded DeFi as the “future of finance”, believing that Defi will subvert traditional banks and brokers and provide lower-cost and more efficient financial services.JPMorgan CEO Jamie Dimon also pointed out that some parts of DeFi can be integrated with traditional finance and become the backbone of the future financial system.

andBlackRock CEO Larry Fink has supported Bitcoin and RWA in public statements many times, saying: “Every stock, every bond, every fund, every asset can be tokenized.”In his 2025 annual chairman letter to investors, he stressed that this shift could revolutionize the investment sector.

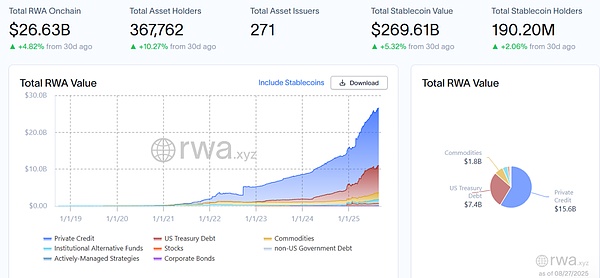

Wall Street’s statements are not only reflected in its verbal troubles, but its actual actions are also quite effective.According to rwa.xyz, the market size of non-stable currency RWA assets has increased more than 100 million in the past year and has now exceeded US$26 billion.cowryRyder’s tokenized fund BUIDL has grown to a size of US$2.3 billion in less than one and a half years after its launch, becoming the leader of US bond RWA funds.Franklin Templeton’s money market tokenization fund BENJI also grew to a scale of $700 million. The addition of these institutions not only provides liquidity for the RWA field, but also boosts market confidence in the track and further promotes RWA’s explosive growth.

Of course, the result of Wall Street’s massive outcome is the result of a series of factors.first,Unlike most on-chain assets, the rise of RWA is not due to pure speculative psychology, but because the market has a rigid demand for stable returns. RWA assets that have both real value support and superior liquidity are destined to be favored.After Bitcoin and Ethereum ETFs were approved, the market’s interest in RWA became increasingly obvious and soon became a new trend.

Second,The shift in U.S. regulatory policies pave the way for the rise of cryptocurrencies and RWA.The Loomis-Gillibrand Act in July 2024 clearly defines crypto assets jurisdiction, and years of regulatory chaos ended, creating a good environment for the establishment of a legal framework related to RWA.Since then, as Trump comes to power and former SEC chairman Gary Gensler loses power, the SEC stops targeting Immutable, Coinbase andKraken’s investigation and litigation, the regulatory environment related to Defi and RWA has been completely improved.

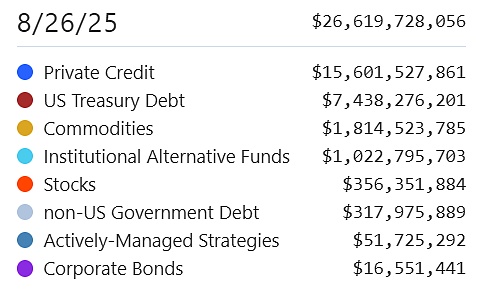

Overall, the combination of government support, clear supervision and legislative actions eliminates uncertainty in the crypto market and creates an ideal environment for the integration and development of blockchain and real assets.After excluding regulatory risks, different categories of RWA assets have sprung up like mushrooms after a rain, and tokenized real estate, bonds, and commodity-related assets have all become active on the chain.,As of August 26, 2025, there were 271 institutions that issued RWA assets, sorted by market size, and the sub-track scales of each RWA product are as follows:

•Private Credit ($15.6 billion)

•U.S. Treasury bonds ($7.4 billion)

•Commodity (US$1.8 billion)

•Institutional Alternative Investment Fund (USD 1 billion)

•Stocks ($350 million)

•Non-US government bonds ($310 million)

•Active Management Fund (USD 51 million)

•Others ($16 million)

Of course, all this is just the beginning. Financial 3.0 composed of RWA and Defi systems is far from reaching the growth bottleneck, and a financial revolution with considerable significance is breaking out.Throughout history, the capitalization of assets has given birth to commercial banks and credit markets, and the securitization of assets has given birth to investment banks and capital markets, promoted the formation of modern fiscal systems, and indirectly promoted the formation of power checks and balances and the formation of modern democracy.For current national organizations, asset monetization (RWA) will also be a significant revolution.