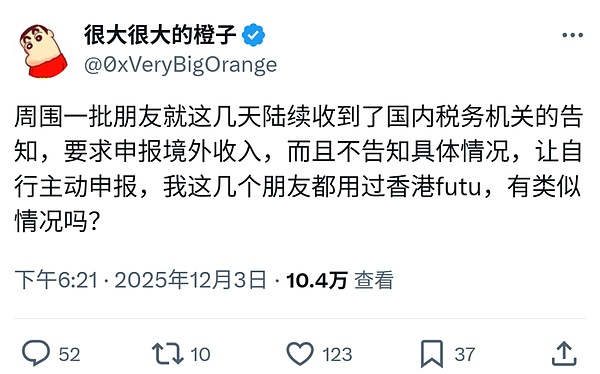

Recently, a tweet on social media about the declaration of overseas income quickly triggered a heated discussion, with more than 100,000 clicks.

Many domestic residents mentioned in the comment area that they have received reminders from the tax authorities through text messages, individual tax APP prompts or phone calls, requiring self-examination and declaration of overseas income as soon as possible.It is not difficult to see from this interactive boom that the tax authorities have recently paid significantly more attention to the overseas investments of domestic residents.Similar signals are not accidental: as early as November 11, the tax authorities in six places including Beijing and Guangdong simultaneously exposed 6 cases of failure to declare overseas income in a timely manner.Obviously, this unified regulatory action is no accident. The tax authorities’ systematic verification of individuals’ overseas income will have a significant impact on the highly popular web3 investment activities.

This article will combine the recent collective actions of the tax bureaus of six provinces and cities to analyze the panoramic view of this round of “batch notification” regulatory actions, and provide actionable compliance self-inspection and declaration response suggestions from the perspective of encryption practitioners.

1. Why now?CRS and the “Fourth Phase of Golden Tax” work together

On November 11 this year, the taxation departments of six provinces and cities in Beijing, Guangdong, Shenzhen, Fujian, Xiamen, and Sichuan issued the “Notice on Guiding Persons with Undeclared Overseas Income to Conduct Self-Inspection and Rectification” almost at the same time, and exposed a number of typical cases, such as Wang in Beijing who paid back 510,000 yuan, Zhou in Shenzhen who paid back 3.362 million yuan, and Fu in Xiamen who paid up to 6.987 million yuan.The fundamental reason why the tax department was able to launch collective action this time was the support of the “tax big data analysis system”.This regulatory upgrade is the inevitable result of technological maturity, mainly including CRS (Automatic Exchange Standard for Financial Account Tax-Related Information) and the “Fourth Phase of Golden Tax” project.

1.1 Normalization of CRS information return

CRS is a standard for the automatic exchange of financial account tax-related information issued by the Organization for Economic Cooperation and Development (OECD). Currently, more than 100 countries have joined.As of 2023, China has achieved normalized and automatic exchange of information with more than 100 countries and regions around the world. The information exchanged is very wide: not only account balances, but also bank deposits, securities accounts (such as US and Hong Kong stocks), insurance with cash value, offshore trust income, etc., are all exchanged.

It is rumored that the tax department has recently launched a collective action because the overseas account information for 2022-2023 has recently been exchanged and returned.The tax authorities hold the “accounts” returned by CRS and compare them with domestic declaration records. The individuals who have omitted to report will naturally be clear at a glance.

1.2 Accurate portrait of the “Fourth Phase of Golden Tax”

CRS is a key means of obtaining overseas tax information. With the launch of the fourth phase of the Golden Tax, the regulatory capabilities of tax authorities have achieved a leap forward.The tax department can now use big data, artificial intelligence and other technologies to efficiently compare multi-dimensional data including tax, banking and consumption.Its core function is to intelligently identify abnormal tax data and upgrade supervision from traditional means to precise digital review.

The intelligent comparison capabilities of “Golden Tax Phase IV” can quickly identify obvious tax risk points.For example, a resident’s annual declared income in China is RMB 500,000, but he purchased overseas real estate worth millions of yuan in his name; or he purchased a large amount of overseas insurance products through a domestic account.Such significant differences in domestic and foreign assets or consumption will immediately trigger tax warnings, allowing tax regulatory authorities to accurately locate potential risks and provide strong technical support for compliance reviews.

2. Overseas additionsecretIs asset income also taxed?

Many Web3 investors are confused: “Since the country prohibits virtual currency transactions, why does it still need to tax it?”

This view is reasonable on the surface, but it does not hold true from the perspective of the current tax law system.Tax collection and administration are not the same concept as administrative licensing. Even if certain types of asset trading activities are restricted, as long as the results of the behavior constitute “income”, the tax authorities still have the right to tax in accordance with the law.First of all, according to the “Personal Income Tax Law”, as long as you have a residence in China, or you have lived in China for a total of 183 days in a tax year, you are a “resident individual”.China implements a global taxation principle for individual residents.This means that whether personal income comes from wages in Beijing, dividends from US stocks, or income from on-chain DeFi, as long as it constitutes “income”, it is within the jurisdiction of the Chinese tax authorities.

Secondly, in terms of specific implementation standards, as early as 2008, the State Administration of Taxation made it clear in the “Reply on the Collection of Personal Income Tax on Income Obtained by Individuals from Buying and Selling Virtual Currency Online” that individuals’ income from buying and selling virtual currency online should be subject to individual tax as “income from property transfer”.Although this regulation originally targeted game currencies, in current regulatory practice, many trading gains from crypto-assets such as Bitcoin are implemented with reference to this document.

Therefore, even if crypto assets are stored in overseas exchanges or cold wallets, once income is generated – especially when it is liquidated and returned to the country through OTC, this part of the income is legally considered “overseas income” and must fulfill reporting obligations.

3. What are the consequences of not reporting?

We have noticed that in the comment section of the tweet, some web3 investors believe that “it is not too late to pay taxes after being found out.” However, under the framework of tax law, there is a big gap between the legal characterization and economic penalties of passive tax payment and active self-examination declaration.

3.1 Huge late fees

According to Article 32 of the Tax Collection Administration Law, if a taxpayer fails to pay taxes within the prescribed time limit, the tax authorities, in addition to ordering payment within a time limit, will also impose a daily late payment penalty of 0.05% of the overdue tax starting from the date of overdue tax payment.From a simple calculation, this means that the annualized interest rate of late payment fees is as high as 0.05% × 365 = 18.25%, which is far higher than the interest rate of ordinary commercial loans..Moreover, this money is compulsorily collected by law, and there is no room for “reduction or exemption”. The longer it is delayed, the heavier the burden will be.

3.2 Up to 5 times fine and characterization of “tax evasion”

According to Article 63 of the “Tax Collection and Administration Law”, anyone who refuses to declare after being notified by the tax authorities, or makes a false tax declaration, or fails to pay or underpays the tax due, is an act of tax evasion.Once it is determined to be tax evasion, the tax authorities will not only recover the underpaid taxes and late payment fees, but also impose a fine of not less than 50% but not more than 5 times the amount of non-payment or underpayment of taxes.That is to say, if an individual refuses to declare a tax payable of 1 million yuan, in addition to having to pay back taxes and late fees, the most severe penalty may be a fine of 5 million yuan, doubling the economic losses.

3.3 Credit downgrade and criminal risk

According to Article 6, Paragraph 1 of the “Measures for the Administration of the Disclosure of Information on Dishonest Subjects with Major Tax Violations”, if an individual fails to declare income from crypto assets, refuses to declare after being notified by the tax authorities, and fails to pay or underpays more than 1 million yuan in tax payable, accounting for more than 10% of the total tax payable for each tax category that year, he will be identified as a major tax violation and distrustful subject.At the same time, Article 15 of the Measures clarifies that untrustworthy entities included in the scope of tax credit evaluation will be directly judged as D-class taxpayers.Once judged as a D-class taxpayer, the consequences include but are not limited to: restrictions on leaving the country, restrictions on high consumption, and the inability to apply for loans, etc.

In addition, according to Article 201 of the Criminal Law, if an individual obtains high profits from buying and selling virtual currencies online but fails to declare them, and the amount of tax evaded reaches more than 100,000 yuan (a relatively large amount), which accounts for more than 10% of the total tax payable for the year, and if the tax authority issues a recovery notice and still refuses to pay back taxes, pay late fees, or accept administrative penalties, he will be deemed to be guilty of tax evasion.Once the crime of tax evasion is committed, not only will you have to pay back taxes and late fees, your credit and social rights will also be greatly restricted, and even worse, you will face jail time.

4. How to respond when receiving a notification?

Although the consequences of failure to declare are serious, there is no need to panic or delay after receiving a prompt or notice from the tax authorities regarding the declaration of overseas income.A more prudent approach is to complete fact checking, material compilation and declaration standard confirmation as soon as possible, and communicate with the tax authorities on the basis of verifiable evidence.

Step One: Verification and Self-examination

Log in to the “Personal Income Tax” APP to check the site’s messages, reminders, and whether there are years for which supplementary declarations are required. Also pay attention to whether the specific year, income type, or processing path is specified in the text message/telephone notification.Compare the scope of the notice and sort out overseas-related matters in the past 3-5 tax years: overseas financial accounts, cross-border capital flows, overseas investment income (including dividends, interest, property transfers, etc.), as well as transactions, exchanges and capital reflows involving crypto-assets.Synchronously organize basic materials that can prove the source and whereabouts of funds and build a chain of facts.

Step 2: Distinguish between “principal” and “income”

This is crucial.The tax bureau levies taxes on the “increased part”, not the principal.The calculation formula is: taxable income = transfer income – original value (cost) of the property – reasonable expenses.

Step Three: Cost of Proof

If clear and verifiable purchase costs and transaction paths cannot be provided, the tax authorities, under risk control, may: approve the collection, or even recognize the full withdrawal as income, resulting in a significant negative increase.For example, if the amount of a certain capital repatriation is 1 million yuan, and the corresponding asset purchase cost is 900,000 yuan and the reasonable expenses are 0, the theoretical taxable income is 100,000 yuan; however, if the taxpayer cannot provide complete transaction records to prove the costs and expenses, the tax authorities may only recognize part of the cost, or even confirm a higher taxable income based on the approved method, and the final tax burden may be much higher than the result calculated based on the true income.

5. How to sort out the “messy” encryption accounts?

For most Web3 investors, the core difficulties in reporting compliance to the tax bureau lie in two points: the transaction chain can be traced and the cost basis can be verified.The reason why encrypted accounts are prone to chaos usually stems from the following four types of structural problems:

-

High-frequency trading: The number of transactions is huge, and it is easy to miss and make mistakes when checking each transaction manually, making it difficult to ensure the integrity of the details.

-

Cross-platform and cross-chain decentralization: assets are distributed across multiple exchanges and multiple wallet addresses, with frequent internal transfers and capital paths that are difficult to restore.

-

Pricing and profit and loss recognition are complex: in tax calculations for currency-to-currency transactions, currency swaps, contract closings, etc., it is often necessary to recognize disposal income and calculate profits and losses based on the fair value of legal currency at the time of transaction.

-

DeFi flow is difficult to standardize: there are various transaction forms such as pledge/re-pledge, airdrop, liquidity market making, loan interest, etc. If the classification caliber is unclear, “misjudgment of nature, omission of income or double calculation” may easily occur.

Once the details, classification and cost evidence are insufficient, subsequent self-examination declarations or explanations will face higher uncertainty and compliance costs.

Conclusion

The centralized notices from the tax authorities in the six places can be seen as a signal for the “normalization and digitalization” of the supervision of overseas income of individual residents.As CRS information exchange and collection and management digitization capabilities continue to improve, the differences between overseas accounts and domestic declarations will become easier to identify, and the scissor gap between compliance costs and non-compliance risks will further expand.For Web3 investors, establishing verifiable accounting and reporting standards as early as possible will provide greater certainty and cost advantages than subsequent remediation.

Based on this, it is recommended to complete transaction data collection, cost basis sorting and income classification as soon as possible to form traceable detailed and summary reports so that there are sufficient facts and evidence support when self-examination declarations, supplementary explanations or communication with tax authorities.