Author: AJC, Messari Research Manager; Source: X, @AvgJoesCrypto; Compiler: Shaw Bitcoin Vision

Of all the major cryptocurrency assets, Ethereum (ETH) has sparked the most heated debate.Bitcoin’s (BTC) dominance as a cryptocurrency is largely undisputed,ButEthereum’s status is far from settled.For some people,Ethereum is the only credible non-sovereign currency asset besides Bitcoin; and for others,It represents a business with declining revenue, shrinking margins and continued competition from faster and lower-cost L1 payment services.

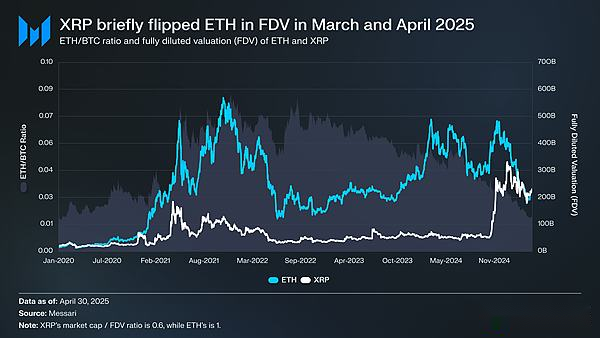

The debate seemed to reach a fever pitch in the first half of this year.In March, XRP’s fully diluted valuation (FDV) briefly surpassed that of Ethereum(It’s worth noting that Ethereum is fully liquid, while XRP’s circulation only accounts for about 60% of its supply).

March 16,Ethereum’s FDV is $227.65 billion, while XRP’s FDV reaches $239.23 billion, which almost no one expected a year ago.Subsequently, on April 8, 2025,ETH/BTC ratio falls below 0.02 for first time since February 2020.In other words, Ethereum’s excess returns relative to Bitcoin in the last cycle have completely disappeared.At this point, market sentiment towards Ethereum has reached its lowest point in years.

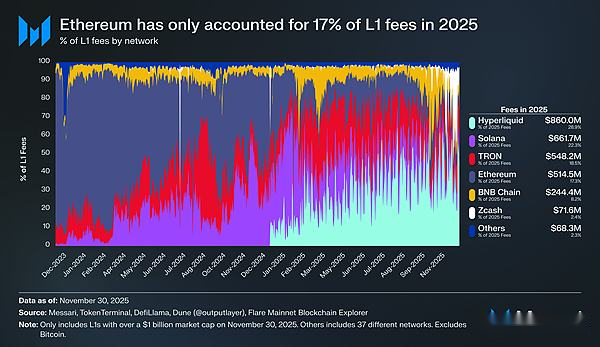

Worse, price action is only part of the problem.As competitor ecosystems rise,Ethereum’s share of L1 network transaction fees continues to decline.SolanaRegaining its footing in 2024,HyperliquidComing out of nowhere in 2025, theyTogether, they lowered Ethereum’s fee share to 17%, ranked fourth among the L1 trading platforms. Compared with the top position a year ago, it can be said to have fallen off a cliff.Transaction fees are not the measure of everything, but they clearly reflect the direction of economic activity, and Ethereum is facing the most competitive landscape in its history.

However, history shows that the most significant reversals in cryptocurrencies often begin when market sentiment is at its most bearish.While Ethereum was dismissed as a failed asset, much of its so-called “failure” was actually already reflected in the price.

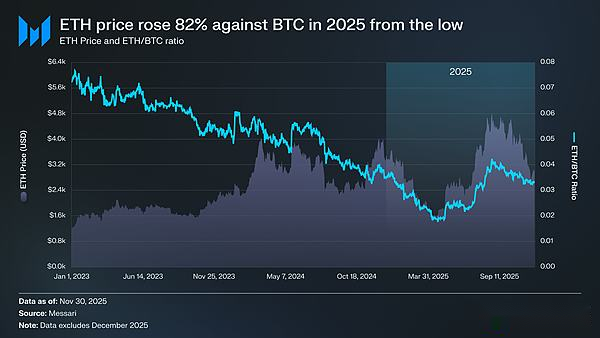

In May 2025, the market began to show signs of optimism, indicating that the market was overconfident in a bear market.During this period, both the ETH/BTC ratio and the Ethereum price against the USD began to reverse significantly.The ETH/BTC ratio climbed 139% from a low of 0.017 in April to 0.042 in August; while Ethereum itself rose 191% during the same period, from $1,646 to $4,793.The upward momentum finally peaked on August 24, with Ethereum hitting an all-time high of $4,946.

After this repricing, the overall trend of Ethereum has clearly shifted towards strength again.toEthereum Foundation leadership changes and emergence of Ethereum-focused digital asset reserve, bringing a confidence that had been lacking for much of the previous year.

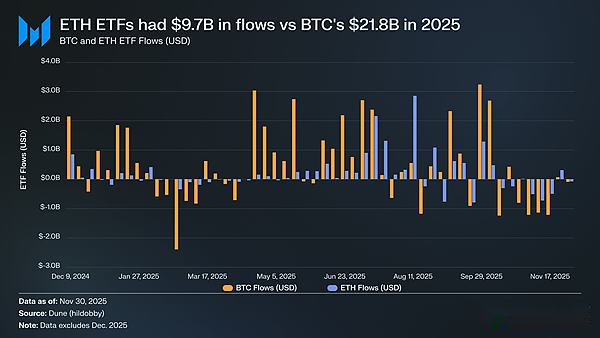

Prior to this rally, the differences between Bitcoin and Ethereum were most evident in their respective exchange-traded fund (ETF) markets.In July 2024, when the Ethereum spot ETF was launched, capital inflows were very weak.In their first six months, they raised just $2.41 billion, a figure that pales in comparison to the record performance of Bitcoin spot ETFs.

However, with the recovery of Ethereum, concerns about ETF capital flows have completely reversed.Over the past year, Ethereum spot ETFs have seen $9.72 billion in inflows, while Bitcoin ETFs have seen $21.78 billion.Considering that Bitcoin’s market capitalization is almost five times that of Ethereum, the difference in inflows between the two is only 2.2 times, which is much lower than many people expected.In other words, on a market-cap adjusted basis, demand for Ethereum ETFs exceeds that of Bitcoin, contrary to previous claims of a lack of interest in Ethereum from institutional investors.In some cases, Ethereum has even surpassed Bitcoin entirely.From May 26th to August 25th,Ethereum ETF inflows of $10.2 billion surpassed Bitcoin’s $9.79 billion during the same period, marking the first significant shift in institutional investor demand towards Ethereum.

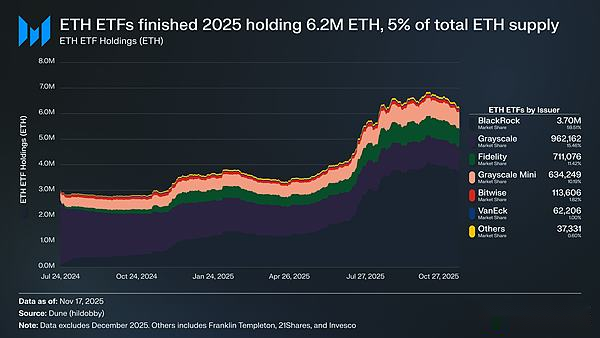

From an ETF issuer perspective, BlackRock has further solidified its dominance in the ETF market, withThe number of ETH it holds reaches 3.7 million, accounting for 60% of the total Ethereum spot ETF market share.This number is a significant increase from 1.1 million ETH at the end of 2024, an increase of 241%, and the annual growth rate exceeds that of all other issuers.Overall,The Ethereum spot ETF held 6.2 million ETH at the end of 2025, accounting for approximately 5% of the total supply.

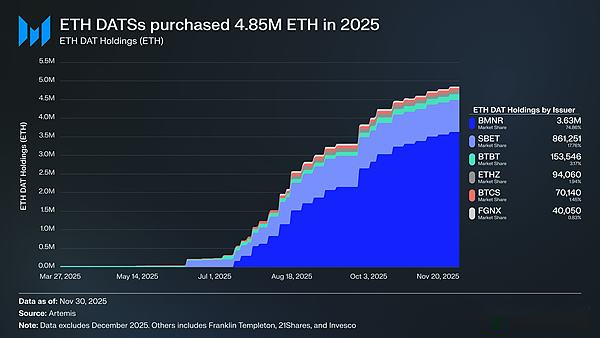

Behind Ethereum’s Strong Rally, the Most Important Development IsThe Rise of Digital Asset Reserves (DATs) Focused on Ethereum.DAT creates an unprecedented source of stable and sustained demand for Ethereum, anchoring Ethereum in an unprecedented way that no narrative or speculation can.If Ethereum’s price action marks a clear turning point, the accumulation of DAT is the deeper structural shift that contributed to it.

DAT has had a significant impact on the price of Ethereum,4.8 million ETH accumulated during 2025, accounting for 4% of the total supply.Among them, the Ethereum DAT with the most accumulation is Tom Lee’s Bitmine (BMNR).Bitmine, a former Bitcoin mining company, began converting its reserves and capital into ETH in July 2025.inBetween July and November, Bitmine purchased 3.63 million ETH, making it the absolute leader in DAT market share, accounting for 75% of all DAT holdings.

Although Ethereum’s rally was strong, it eventually cooled off.By November 30, Ethereum prices had fallen back from the August high to $2,991, even well below the previous all-time high of $4,878 in the previous cycle.Ethereum is currently in a much better position than it was in April, but this rally has not eliminated the structural concerns that initially fueled the bearish sentiment.In fact, the debate over Ethereum has only intensified.

On the one hand, Ethereum exhibits many of the same characteristics that Bitcoin did in its rise as a currency.ETF inflows are no longer weak.DAT reserves have become a constant source of demand.And, perhaps most importantly, more and more market participants view Ethereum as distinct from other L1 tokens, with some now viewing it as an asset within the same monetary framework as Bitcoin.

However, the headwinds that dragged down Ethereum prices earlier this year have yet to abate.Ethereum’s core fundamentals have yet to fully recover.Its L1 fee share continues to be under pressure from strong competitors such as Solana and Hyperliquid.Underlying trading activity remains well below the peak of the previous cycle.Despite Ethereum’s sharp rally, Bitcoin remains well above its all-time highs, while Ethereum remains below its all-time highs.Even during Ethereum’s strongest months, a significant number of holders viewed the rally as an opportunity to cash out rather than as a validation of its long-term monetary thesis.

The core issue in this debate is not whether Ethereum has value, but how Ethereum’s core asset, ETH, accumulates value from the Ethereum network.

Last cycle, it was widely believed that the value of ETH would be directly derived from the success of Ethereum.This is a key part of the “ultrasonic currency” argument: Ethereum will be so useful that ETH will be burned in large numbers, providing a clear and mechanically guaranteed source of value for the asset.

Now, we can say with a fair degree of confidence that this is not the case.Ethereum’s fees have dropped significantly with no signs of recovery in sight, and its largest sources of growth – real world assets (RWA) and institutional investors – primarily use USD as the base currency asset, rather than ETH.

ETH’s value will now depend on how it indirectly benefits from Ethereum’s success.But such indirect benefits are far less certain.It relies on the hope that as the Ethereum ecosystem grows in importance, more and more users and capital will choose to view ETH as a cryptocurrency and store of value.

But unlike direct, mechanical accumulation of value, this phenomenon is not guaranteed to happen.It relies entirely on social preferences and collective beliefs, which is not a flaw in itself (after all, so does Bitcoin’s value accumulation).But it does mean that Ethereum’s appreciation is no longer tied in a deterministic way to Ethereum’s own economic activity.

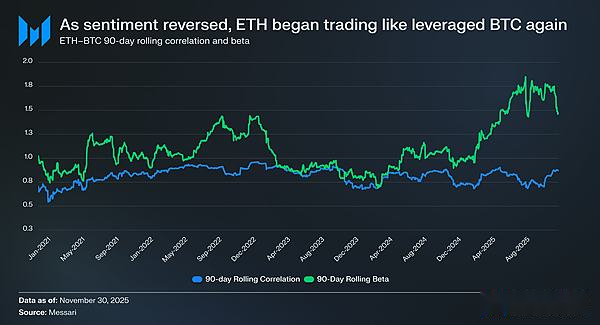

All of this brings the controversy over Ethereum back to its core contradiction.Ethereum may indeed be accumulating a currency premium, but it will always be lower than Bitcoin.The market once again views Ethereum as a leveraged manifestation of Bitcoin’s monetary theory rather than an independent monetary asset.Throughout 2025, ETH’s 90-day rolling correlation coefficient with BTC has hovered between 0.7 and 0.9, while its rolling beta has surged to multi-year highs, sometimes exceeding 1.8.Ethereum is more volatile than Bitcoin today, but is still dependent on Bitcoin.

This is a subtle but extremely important distinction.With Ethereum’s current monetary relevance, the monetary narrative derived from Bitcoin remains solid.As long as the market still believes that Bitcoin is a non-sovereign store of value, there will be a segment of market participants willing to extend this belief to Ethereum.If Bitcoin continues to strengthen in 2026, Ethereum is well positioned to catch up.

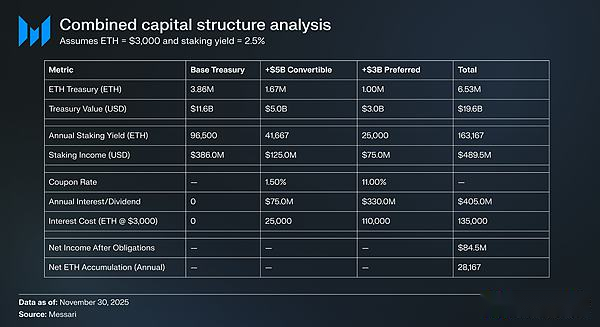

Ethereum DATs are still in their early stages of development, and so far they have primarily facilitated the accumulation of ETH through the issuance of common shares.However, in a new crypto bull run, these entities may explore other capital formation strategies, similar to those used by Strategy to expand its Bitcoin investments, including convertible bonds and preferred shares.

For example, a DAT like BitMine can issue low-interest convertible bonds and high-yield preferred stocks, and use the proceeds directly to purchase ETH, which is then pledged to generate ongoing income.Under reasonable assumptions, staking income can partially offset fixed interest and dividend expenses, allowing corporate treasury to continue accumulating ETH when market conditions are favorable, while increasing balance sheet leverage.Assuming a full recovery from the Bitcoin bull run, this potential “second life” of Ethereum DAT could become an additional source of support for ETH’s higher beta relative to Bitcoin in 2026.

Finally,The market still pegs Ethereum’s currency premium to Bitcoin’s currency premium.Ethereum is not yet an autonomous monetary asset with an independent macro foundation; instead, it is increasingly becoming a secondary beneficiary of Bitcoin’s monetary consensus.Ethereum’s recent resurgence reflects the willingness of a small group of investors to view Ethereum as an alternative to Bitcoin rather than a typical L1 token.However, even with Ethereum’s relative strength, the market’s confidence in Ethereum is inseparable from the continued strength of Bitcoin’s own narrative.

In short, Ethereum’s monetary story is no longer fragmented, but it’s still not settled.Under the current market structure, given Ethereum’s higher beta relative to Bitcoin, Ethereum could appreciate significantly if Bitcoin’s thesis continues, and structural demand from DATs and corporate funding would give it real upside in this scenario.But for the foreseeable future, Ethereum’s monetary value will still depend on Bitcoin.Unless ETH’s correlation and beta with BTC decreases (which it has never done), Ethereum’s premium will continue to fluctuate in Bitcoin’s shadow.