Author: Cai Pengcheng

HashKey bell ringing scene, Xiao Feng is fifth from the right

In 1998, Xiao Feng, the 37-year-old deputy director of the Shenzhen Securities Regulatory Office (now the Shenzhen Supervision Bureau), chose to resign and go to work.When he received the appointment letter as general manager of Boshi Fund, he was holding one of the first ten public fund licenses in China’s capital market.That year, Boshi, together with ten peers including Southern, Cathay Pacific and HuaXia, kicked off China’s public fund industry.

26 years later, when this financial veteran stood in front of the Hong Kong Stock Exchange, this time he was holding a stack of compliance passes leading to the new world of crypto-finance—from license No. 1 (securities trading), license No. 7 (automated trading services) to VATP (virtual asset trading platform) license.The protagonist becomes HashKey, a financial group dedicated to global digital asset services that attempts to put encrypted finance into a compliance cage.

In China’s financial history, there are few people like Xiao Feng who not only have a regulatory background, but also fully experienced the turbulent era of traditional capital markets and the wild growth of encrypted digital assets.

After submitting the prospectus, Dr. Xiao Feng, chairman and CEO of HashKey Group, known as the “Godfather of China’s Blockchain,” accepted an exclusive interview with Barron’s Chinese.

In Xiao Feng’s view, “The era of wild jungle growth is over.” As regulation in various countries accelerates the implementation of regulations, the offshore model will gradually decline, and compliance is the only pass.

Based on this final judgment, HashKey has firmly chosen the “narrow door” of compliance since 2018, when there were no clear regulatory regulations in Hong Kong.This means that it must voluntarily give up the “asset-light, quick-to-make money” traffic dividends of offshore exchanges, and instead shoulder heavy regulatory costs and compliance obligations.The prospectus revealed that in the first six months of 2025, compliance costs are estimated to be approximately HK$130 million.The average monthly compliance cost exceeds HK$20 million.

But that’s not all.In Xiao Feng’s chess game, compliance is only the bottom line for survival. His real ambition lies in the reconstruction of the business model – he is never willing to be a simple matching exchange, but to use the new accounting method of distributed ledgers to try to build a set of “encrypted financial infrastructure” similar to the clearing and settlement model of digital cash transactions.

Xiao Feng recalled that before founding HashKey, he conducted in-depth research on many major stock exchanges around the world and concluded that the transaction matching business only accounted for less than half of the revenue of almost every large exchange.

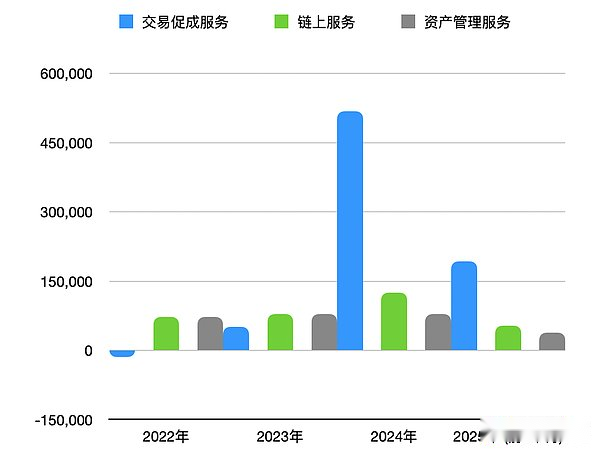

The prospectus outlines the entire business of this digital asset group: a composite system covering transaction facilitation, on-chain services and asset management. Trading business is still the core of its business, accounting for approximately 75% of Hong Kong’s 11 license market.The other two fronts – the on-chain service sector manages pledged assets of 29 billion Hong Kong dollars; in terms of asset management business, the management scale since its establishment has reached 7.8 billion Hong Kong dollars.

However, the revenue performance in the past three years shows that it has not completely escaped the violent cyclical law of the encryption market, and the growth curve shows certain high beta characteristics.

Data source: HashKey prospectus

In another slightly anomalous sign, the company’s revenue has doubled, but it’s still in the red.In addition to high compliance costs, huge investment in research and development is also an important reason.In 2024, HashKey’s R&D expenditure will reach HK$556 million, accounting for 77.1% of revenue.This ratio far exceeds that of Internet platforms and is even higher than that of many hard technology listed companies.

The reason behind this move is still that Xiao Feng does not regard HashKey as just a trading desk, but is trying to build a new financial infrastructure based on distributed accounting methods.A large amount of funds have been poured into the research and development of the underlying facilities of the blockchain (such as L2 network HashKey Chain) and related system capabilities.

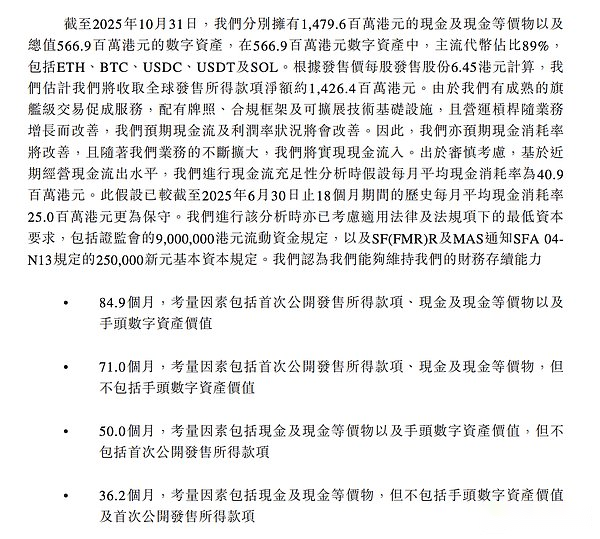

Xiao Feng denied that the choice to go public was due to losses or cash flow problems.Regarding the latter, the prospectus stated: As of October 31, 2025, the company held approximately HK$1.48 billion in cash and approximately HK$567 million in digital assets on its books.Even excluding digital assets and IPO fundraising, the existing cash is enough to support the company’s continued operations for 36.2 months at an average monthly cash consumption rate of HK$40 million.

“The second half of next year” is a key node that Xiao Feng mentioned many times in the interview, and is also regarded as the biggest driving force for HashKey’s listing.This time division comes from both Coinbase and Nasdaq announcing that they plan to launch tokenized stock trading services in the United States in the second half of next year.

Xiao Feng demonstrated here his macro vision as the “Godfather of Blockchain”.In his view, the second half of 2026 is the “singularity point” when the old and new financial orders transition.The logic behind it is that when tokenization on the capital side (stable coins, deposits, CBDC) and tokenization on the asset side (stocks, funds, bonds) converge on the chain, a closed business loop of an “on-chain financial market system” will officially run through.HashKey is the key infrastructure builder in this closed loop.”

What drives this process is fear and counterattack.He mentioned that Coinbase is trying to provide stock tokenized trading services to subvert the middle and back offices of Wall Street. This move has forced old giants such as Nasdaq to also launch stock tokenized plans to save themselves.U.S. legislation has almost cleared the obstacles, and the timelines of the giants all point to the second half of 2026.

The crypto world is advancing rapidly, and Xiao Feng’s judgment has not changed with the ups and downs of the cycle.In his view, one side is the revolutionaries (Coinbase) and the other side is the reformists (Nasdaq).But no matter which faction you are on, you have to admit: new financial market infrastructure is an irreversible trend.

The following is a conversation between Barron’s Chinese website and Dr. Xiao Feng, chairman and CEO of HashKey Group.

Stablecoins need to get rid of cognitive misunderstandings

Q: The recent news about the mainland’s crackdown on “illegal stablecoins” has triggered a lot of discussion.Will this affect the rhythm of Hong Kong?

Xiao Feng: These are completely two different things.Everyone must make a clear distinction: the mainland is cracking down on pyramid schemes and fraud using the concept of “stablecoins”; while Hong Kong is cracking down on compliant stablecoins under the legal framework.

Even my friends have asked me before: “Mr. Xiao, I also want to invest in stablecoins.”I asked him why, and he said: “Don’t stablecoins have fixed returns?”This is a misunderstanding. Real stablecoins (such as USDT) themselves do not earn interest, but they have become financial products with stable returns in the mouths of MLM organizations.

In fact, from the time the Hong Kong Monetary Authority began brewing the Stablecoin Bill two years ago to now, the entire tokenization market landscape has undergone tremendous changes.We can no longer look at problems from the perspective of two years ago.

Q: How has the tokenization market landscape changed?

Xiao Feng: Now looking at “currency tokenization” on a global scale, three clear approaches, or three models, have actually been formed:

The first type: Stablecoins of compliant commercial institutions.This is what Hong Kong’s stable currency law defines and what is discussed in the US Stable Currency Act, which is the tokenization of legal currencies by commercial institutions (such as Circle, Tether).This is currently the most mainstream model.The second type: central bank digital currency.This is directly done by the central bank and tokenizes the currency.The Central Bank of China is already working on digital renminbi, and the European Central Bank is also planning it. Although the Federal Reserve’s current attitude is unclear, this is undoubtedly an important aspect.The third type: Tokenization of bank deposits.This is a new force that has suddenly emerged in recent months.For example, the sandbox program launched by the Hong Kong Monetary Authority has already involved seven banks, including HSBC, Standard Chartered, and BOC Hong Kong.The core of this sandbox is to explore how to directly tokenize bank deposits.

Tokenized deposit sandbox involving seven banks in Hong Kong; Source: Official website of the Hong Kong Financial Supervisory Authority

Q: Why do banks have a positive attitude towards the tokenization of funds?

Xiao Feng:The banks are backed into a corner and must fight back.

Stablecoins (such as USDT) issued by commercial institutions have taken away the business of banks. The bank thinks: Since the market needs currency tokenization, my capital scale is larger than yours, I have more customers than you, and I have more application scenarios than you. Moreover, the tokenization of my deposits can also calculate interest for users, why don’t I do it myself?

Therefore, these three models—commercial institution stablecoins, CBDC, and bank deposit tokenization—will coexist for a long time in the future.As for whose vitality is more vigorous?In fact, it remains to be seen. Stablecoins may not necessarily win, nor may banks win.

The advantages of banks are very obvious: they have large funds, a large customer base, and many application scenarios. Moreover, the tokenization of bank deposits can calculate interest for users, which is something USDT cannot do.But a bank also has disadvantages: It is usually a closed system that can only serve its own network of customers.Unlike USDT, it does not rely on bank accounts and flows freely on the public chain, reaching far and wide.

So I believe that they will each have their own scenarios and tokenize currencies in their own ecosystems.

If you look at the overall financial market, the asset side is actually accelerating tokenization.Funds, bonds, and stocks are all trying to be tokenized, and I believe insurance will also join in the effort in the future.In this way, the capital side and the asset side are formed, and both sides begin to be tokenized.Over time, a closed loop between capital-side tokens and asset-side tokens on the chain will be formed.

Q: Regarding RWA, the first case of default occurred in the United States in November.What do you think about the authenticity and prospects of RWA?

Xiao Feng: In fact, everyone thinks of RWA too complicatedly. It is essentially an asset tokenization (AssetTokenization).The so-called “everything can be tokenized” is an unstoppable trend.I think its development can be clearly divided into three stages:

Phase One: Currency Tokenization.This history is very early and can be traced back to the birth of USDT in 2014, which is the tokenization of the US dollar.Later, USDC came out in 2016.This is version 1.0 of RWA.

The second stage: tokenization of financial assets, which began to explode last year.The most typical representatives are BlackRock and Franklin Templeton.They began to promote the tokenization of monetary funds and treasury bonds in the United States.At present, this stage is developing rapidly, and the technology and legal paths are relatively mature.

The third stage: tokenization of physical assets.This is RWA in a narrow sense, such as real estate and artwork on the chain.Frankly speaking, there has been no success story in this area so far.Why?Because there is a core technical problem that has not been solved: the oracle problem.How do you ensure that the tokens on the chain and the physical assets offline are always bound one by one and never become unanchored?The trust mechanism in between still needs to be explored.

I believe that the key to solving the problem of tokenization of physical assets may lie in DePIN (decentralized physical infrastructure).DePIN connects physical devices directly to the blockchain network.Only when IoT devices can transmit physical world data to the chain in real-time and reliably, and solve the trust problem of “on-chain”, will there be a complete solution to the tokenization of physical assets.

Source: HashKey prospectus

Listing, compliance and profitability

Q: Why did you choose to go public at this point in time?Is it the so-called “taking advantage of the trend” or “preparing food for the winter” under financial pressure?

Xiao Feng: To be precise, it is to “reserve food” to “take advantage of the situation.”

Why now?Because the on-chain financial market system just mentioned is ready to emerge.Nasdaq submitted a framework for tokenized trading of stocks to the SEC a few months ago.When the world’s largest capital market begins to launch tokenized stock trading in the United States, it means that a true “on-chain financial market” is established.

That’s why I’m optimistic about the future.On one end is the tokenization of funds (currency, deposits); on the other end, the tokenization of assets (funds, bonds, stocks) is also accelerating.When funds and assets are tokenized on the chain, at a certain point in time, the two will converge to form a closed-loop “on-chain financial market system.”That is: use the money on the chain to buy the assets on the chain, and the two parties will complete the transaction directly.

If we push the time back to July this year, we still couldn’t see clearly at that time.But looking back now, the situation has gradually taken shape.The asset side of stocks, bonds, and funds is moving, and the capital side of currency is also moving.I judge that by the second half of next year, this closed loop will be formed.The market system of on-chain finance will truly run smoothly.

Since it is a financial market, it cannot be without transaction intermediaries and infrastructure.HashKey does just that.

This year we deployed a set of compliance layer CaaS products (Crypto as Service) on HashKey Chain, including KYC, AML, privacy protection, information disclosure, etc.HashKey chain is a Layer 2 based on Ethereum, but unlike ordinary public chains, we have specially built a “compliance layer”.Because the bank partners reported to us: “All account information on the public chain is public, and we cannot accept this.” Therefore, we must add privacy protection.

Another important point is that we have added a “transaction rollback” mechanism to the chain.In the financial market, “fat finger” errors such as pressing the wrong decimal point and losing an extra zero are inevitable. There must be remedies to roll back the transaction.Traditional public chains do not have this, but it is necessary to operate in the financial market.

In addition to financial preparation, going public is also a “self-revolution”.Although HashKey is now a licensed institution and regulated by the China Securities Regulatory Commission, this is not enough.Becoming a listed company means that HashKey is subject to supervision by the entire society.When J.P. Morgan or other large financial institutions choose a partner, their requirements are extremely high.It often takes three to six months for these agencies to conduct due diligence on us.If we were a public company, the situation would be completely different.

Our prospectus is over 690 pages.After listing, financial reports must be issued every quarter and there are strict information disclosure obligations.This extreme transparency is our “passport” for cooperation with global heavyweight financial institutions.For emerging industries like Web3, transparency is the greatest trust.

Q: The market is very concerned about HashKey’s profitability.The prospectus document shows that the company’s current cash flow is relatively healthy but still in a state of loss. When do you expect the turning point for HashKey to achieve full breakeven?

Xiao Feng: We do have ample funds on our books, with approximately HK$2.05 billion in reserves (approximately HK$1.48 billion in cash and nearly HK$567 million in digital assets).But this is not just about maintaining operations, but also about strategic opportunities for next year.

HashKey’s cash flow consumption assumptions; source: HashKey prospectus

Regarding profitability, I don’t agree with the statement that “you can’t make money if you comply with regulations.”It is true that compliance cannot make quick money like cutting leeks, but as long as it reaches a certain scale and the compliance costs are shared, it is still a good business.As for the specific break-even point, of course we have internal expectations, but as a company planning to be listed, it is not convenient to make public predictions now.

It’s really fun to do offshore business. The boss can do it all by himself.But in HashKey, it doesn’t matter what I say.If I want to do something, I have to ask the compliance officer or legal officer first.If they say, “Mr. Xiao, there are clear laws and regulations prohibiting this,” then I absolutely can’t do it.

Even if it is a reasonable demand like “shared liquidity”, we have been communicating with the regulator for more than half a year.Because this involves a lot of details: For example, if Hong Kong and Dubai are shared, how will the settlement be done in the middle?How can I transfer funds when the bank is closed on the weekend?These need to be solved one by one.Compliance is a process of slow work and careful work.

Question: In the early days of HashKey’s founding, Hong Kong’s encryption industry was still in a rash era. Why did it resolutely choose the most expensive and slowest compliance path from the beginning?After all, self-imposed limitations may cause HashKey to miss some bull market dividends.

Xiao Feng: I have never been confused.I have worked in the traditional financial system for more than 20 years and have also been a regulator. I understand why the world needs financial supervision.Financial activities naturally have huge negative externalities.You cannot expect practitioners to rely on moral self-discipline to eliminate this risk, that is impossible.Without laws and regulations, the world would be a “jungle world” where the law of the jungle would prevail.

Why was “cutting leeks” popular in the early Crypto circle?Because there is no regulation.But if you want to make this market reach a scale of 10 trillion US dollars, governments will never allow you to cut leeks casually.If you are small, you can be a casino, and everyone is willing to accept defeat; but if you want to become a mainstream financial market and serve the public, you must have rules.

Where did the law come from?It was established after countless investors were deceived and framed.It must have police, courts, and prison cells as deterrents.So, don’t use technology as a cover.”Decentralization” is just a technology, it is not a reason why you can defraud others casually.Even in a decentralized world, fraud is still a crime and still requires jail time.

Q: Compliance, while it may be the right path, is extremely costly and can even bring down the business.

Xiao Feng: Timing is indeed critical.If you were talking about compliance when Bitcoin first came out in 2009, it would be too early and impossible to do.But in 2018, we decided to apply for a license in Hong Kong because I saw a major trend.At the same time, this is a question of perception and belief: do you think cryptocurrency is just a cyclical speculation tool, or do you believe it will really change the global financial infrastructure?I have been convinced from the beginning that distributed ledger technology will reshape financial infrastructure.So I came to Hong Kong at the end of 2018. Even though there was no specific basis for licensing in Hong Kong at that time, I still wanted to find a compliant place to do it.

It was very interesting when I first came to Hong Kong. At that time, the Hong Kong Securities Regulatory Commission told me: “Hong Kong does not need to issue licenses now, and there is no legal basis to issue you licenses.”

Under Hong Kong’s common law, companies can “do whatever they want without being prohibited by law”, while regulatory authorities can “do nothing unless they are authorized by law”.At that time, the regulatory authorities even joked: “You can just turn left when you go out and open your business, and no one will care about you.” I asked jokingly at the time: “Doesn’t that mean no one will care about you at all?” The other party replied: “No, someone will care about it, and the police station will.”

His logic is very clear: If you defraud consumers, defraud investors, or misappropriate client assets, this is a criminal offense and is a matter under the jurisdiction of the police and does not fall within the scope of financial supervision governed by the China Securities Regulatory Commission.

Q: Where are the main compliance costs invested?

Xiao Feng: The cost of compliance is reflected in all aspects.The first is customer acquisition cost.Offshore exchanges are like Internet companies. You can register by filling in your email address; we can’t. The strict KYC process leads to slower customer growth than others, and naturally slower revenue growth.

Secondly, holding a license means that “a sparrow may be small, but it has all the internal organs.” You must have all the departments and systems required by regulations.

Another example is safety costs.Our hosting system uses HSM (Hardware Security Module), and the unit price of servers is in the million-dollar range.To open a server, six people must be present at the same time – three to open the safe house door and three to open the server.

There are also insurance costs.In order to comply with regulatory requirements, we purchased US$2 billion of customer asset insurance, which is among the top configurations in the world.

But the good news is that regulation is also helping us reduce costs.For example, this year the Hong Kong Securities Regulatory Commission allowed global exchanges in the same group to share liquidity, which eliminates the need for each exchange to build a separate pool.Another example is allowing our custody system to serve external parties, not only serving exchange customers, but also family offices or other institutions.As scale increases, unit compliance costs will certainly come down.

“More than the exchange”

Q: HashKey has many business lines. Will the strategic focus be adjusted as it goes public?At the same time, the Crypto industry itself is highly cyclical, and listed companies require stable quarterly statements.How does HashKey solve the contradiction between “Crypto strong cycle” and “stock market stability”?

Xiao Feng: Our business lines are very clear, there are only three: 1. Transaction facilitation (exchange + OTC); 2. On-chain services (node verification + technical services); 3. Asset management.

Source: HashKey prospectus

Our business model is actually closer to Coinbase than to those single exchanges that only do matching.If you study the world’s largest exchange groups – Nasdaq, New York Stock Exchange, and London Stock Exchange, you will find a pattern: they are not just exchanges.

Trading commissions are only part of their income structure.The second and third largest sources of income are usually data services and technical services, and their proportion is not much different from commission income.For example, the London Stock Exchange owns FTSE Russell Index Company, whose indexes are used by funds with US$40 trillion in the world; Nasdaq has sold its matching system to more than 80 exchanges around the world.

HashKey is also a customer of Nasdaq, and what we buy is its market monitoring system.This system is very expensive and there is an annual service fee, but you have to buy it.Because the Hong Kong Securities Regulatory Commission has also installed this system, it must monitor the market in real time for abnormal transactions and manipulation.This gives us a great inspiration: HashKey will also become such a technical service provider in the future.We not only do transactions, but also export compliance technology and data services. This is a business model that can transcend cycles.

Real long-term investors pay great attention to the diversification of revenue mix when looking at an exchange group.If you tell me that you only rely on trading commissions, then the valuation will definitely be discounted.Because the market must have bull and bear cycles.When the bear market comes, the trading volume will be cut in half, and your income will also be cut in half.So there must be non-trading-related income to smooth out this fluctuation.

When I researched the history of exchanges, I discovered that Nasdaq sold its matching engine to more than 80 exchanges around the world and charged an annual service fee.This money is guaranteed to be harvested regardless of drought or flood, and has nothing to do with the quality of the market.HashKey is building such a model: not only doing transactions, but also selling technology and data.This is the path we must take.

Q: The prospectus shows that HashKey’s institutional clients contribute the vast majority of trading volume. How do you view the weak position of the retail side?

Xiao Feng: The local retail market in Hong Kong is indeed small, but HashKey already has the largest retail share among licensed exchanges.And the quality of our users is extremely high.

A retail investor has to go through such a tedious and strict KYC process. If it wasn’t “true love”, he would have run away long ago.Although the number of remaining customers is only a few hundred thousand, their value is very high. The value shared by a single user for the exchange is about ten times that of offshore exchanges.

In addition to retail investors and institutions, we also have a third unique type of customer: licensed brokers.

This is a phenomenon unique to Hong Kong.You cannot see Coinbase providing this kind of service to brokers in the United States, and it is difficult for brokers to access Coinbase as a broker.Why can’t Coinbase do it?Because Coinbase does not obtain a securities license, but a “money transmission license” (MTL) from each state.

In Hong Kong, HashKey has obtained two sets of licenses: one is license No. 1 and license No. 7 obtained under the Securities and Futures Ordinance, which establishes our legal status as a licensed trading system.With a securities license, we can connect with all securities firms in Hong Kong (as long as they upgrade their No. 1 license).

At the same time, we also hold a VATP (Virtual Asset Trading Platform) license under the Anti-Money Laundering Regulations.The dual license allows us to operate like a stock exchange and legally trade non-securities virtual assets (Tokens).This is our barrier.This is a phenomenon unique to Hong Kong: now there are about 40 licensed brokerage firms that have upgraded their licenses and can buy and sell virtual assets on behalf of clients.90% of these brokers are connected to HashKey’s trading system at the backend.Of course in this mode I can’t see who the customer is behind it.

Therefore, together with the “invisible customers” behind these dozens of securities firms, in our customer structure, institutions (including Omni-bus) account for about 80%, and retail investors account for 20%.This is also consistent with the data disclosed in our prospectus.

Question: In terms of future strategy, which end will you focus more on?

Xiao Feng: Both sides will develop.We will continue to expand retail investors, and will also vigorously develop institutional business such as Omnibus.As for the final proportion, we will not deliberately pursue a certain number.We will serve whatever structure the market develops and let it take its course.

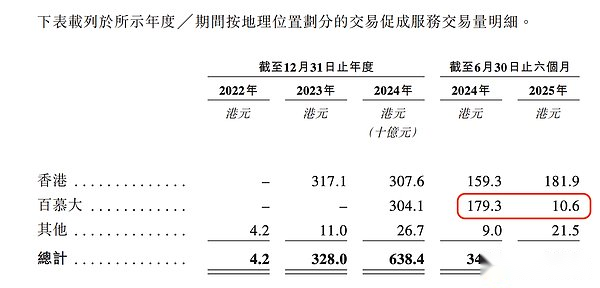

Q: What about the international strategy? The prospectus shows that the company is already operating in Bermuda and other places?

Xiao Feng: The Global website we build has a Bermuda license.Although Bermuda is considered offshore, it has a complete regulatory framework, and Coinbase also obtained a license there.

Of course, the Bermuda model is indeed different from Hong Kong’s “onshore model”.Hong Kong has a local market, but Bermuda has a population of only tens of thousands, so there is no local market at all.So it’s essentially 100% geared towards the international market.We started operating the Bermuda station in April last year, and encountered a big problem during the operation: no bank was willing to provide deposit and withdrawal services.But this year we solved the problem and identified two banks willing to support it.

With banking services solved, we have three major advantages in Bermuda that other offshore exchanges do not have: 1. Compliant legal currency deposit and withdrawal channels; 2. Ability to connect to Omnibus brokerage business (compliant brokers can only connect to compliant exchanges); 3. Ability to trade RWA tokenized assets (requires regulatory approval).

The Bermuda sector shrank significantly in the first half of this year; Source: HashKey prospectus

So next year, we will use these three major advantages to develop Bermuda’s “compliant offshore” business.

Q: How can banks and other traditional financial institutions maintain their competitive advantage in the B-side institutional market when they enter the tokenization market?

Xiao Feng: Cooperation is definitely greater than competition.

This is just like our core business – we are a transaction intermediary.No matter which institution issues tokenized products, as long as they are compliant, we welcome them and we are willing to help them distribute and trade them.

So far, the Hong Kong Securities and Futures Commission has approved us to play the role of a “distributor”.So over the past year, when asset managers in Hong Kong launched tokenized funds, we participated as a distributor.Now, we are working hard to prepare for the next step: on top of distribution, we will further provide secondary market trading services for these products.Of course, the premise is that these products must be approved by regulatory authorities, otherwise we will never touch them.

In this case, we are not launching products ourselves, but providing infrastructure services to the entire market.Therefore, there is definitely a cooperative relationship between us and traditional financial institutions.

Q: Why don’t you be the issuer of stablecoins yourself?

Xiao Feng: Yes.Last year or even the year before, no one had done tokenization in the market, and no one knew how to do it.At that time, we really needed to build some “model houses” and create some templates to let others see: “Look, this can be done.” But this does not mean that we have to do it ourselves all the time.

The most typical example is stablecoins.You will find that HashKey did not apply for a license to issue stablecoins on its own.We went to invest in a company and asked them to apply.Although we are the largest shareholder, it is a completely independent legal entity.

If I hold a stablecoin license tightly in my hand, open an exchange and issue stablecoins, what will other stablecoin issuers think?They will question: “You are both a referee and an athlete, will you open a backdoor for your own coins? Will you treat me fairly?” This will create a conflict of interest.

So we repeatedly weighed internally at that time: first, not participating in the stablecoin track at all?Inappropriate, this is infrastructure and cannot be absent.Second, do it yourself?It is also inappropriate and will harm the neutrality of the exchange.

Q: How do you want the market to define HashKey as a company?

Xiao Feng: I particularly want to emphasize this point.The outside world often misunderstands that HashKey is just an exchange.But in fact, we are a complete financial services group based on digital assets.As I have mentioned repeatedly before, we have three major business pillars: transaction facilitation (exchange business); on-chain services (infrastructure); and asset management.

The old order and revolution in the crypto world

Question: HashKey’s ability to establish a foothold and be listed in Hong Kong must rely on the judgment of industry cycles.Looking back on the past few years, the encryption industry has experienced wild growth and has also faced tightening regulations.Standing at the current juncture, what is your judgment on the trends in the encryption industry?

Xiao Feng: We have three major trends in the future of the industry:

The first trend: from “offshore” to “onshore”.The so-called “offshore” means that it is not subject to supervision or even avoids supervision; “onshore” means that it obtains a license and is subject to supervision in a specific jurisdiction.In the future, the space for “onshore” compliance business will grow rapidly, while the space for “offshore” business will be extremely compressed.

Why is there this trend?Because in the past year or so, more and more countries have begun to legislate licensing.Once a country legislates it, the logic is simple: if you want to continue to serve your own citizens offshore, sorry, that can’t be done.You can either get a license and stay legally; or you can leave without a license.

The new regulations “Guidelines for Virtual Asset Trading Platform Operators” that came into effect in Hong Kong on June 1, 2023 are the most typical example.Prior to this, HashKey took the initiative to voluntarily accept supervision. Although other offshore exchanges did not have a license, they were able to operate freely in Hong Kong and download the App at will.But after June 1, this changed from “voluntary” to “mandatory”.

In the past, all offshore exchange apps could be found in the Hong Kong App Store.But as soon as the new regulations came out on June 1, all these apps were removed.The SFC’s signal is clear: Do you want to continue serving Hong Kong customers?Come and get your license plate.If you indicate that you want to apply for a license, I will give you a 12-month transition period.If you decide not to apply, then I’m sorry, but I’ll give you a grace period (to withdraw by the end of May or August), and then you must completely withdraw from the Hong Kong market.

This is not just Hong Kong, this will be done by countries all over the world.As countries enact legislation one after another, the space for offshore business will definitely be compressed.I dare not say that the offshore model will completely disappear in the future, but its space will definitely not be as large as before. The era of “barbaric growth” is over.

Why can’t I have fun offshore?Because governments will take action.There are two logics behind this: The first is taxation.It is impossible for any government to watch such a large flow of funds without collecting taxes.The second is to protect investors.As a responsible government, how can we watch our people being “cut off leeks” on unregulated platforms?Therefore, it is inevitable for each country to legislate licensing.

The second trend: extending from “digital native” to “digital twin”.”Offshore to onshore” is the business model of exchanges, and this trend is about the financial assets themselves, that is, the tokenization of assets.Bitcoin and Ethereum are “digitally native” assets.But now, the traditional financial market has an asset scale of more than 270 trillion US dollars, and these huge assets will gradually be tokenized.This is called a “digital twin.”

In fact, asset tokenization is essentially a process of securitization.Since it is a security, 99.99% of it requires regulatory approval.Do you think the assets approved for issuance by the China Securities Regulatory Commission will allow you to trade them on an unregulated offshore exchange?Absolutely impossible.So this is a huge opportunity for compliant exchanges.

The third trend is from Off-chain to On-chain.In the future, all financial institutions and financial markets will eventually converge into a unified “on-chain financial market system.”When tokenization on the capital side (funds) and tokenization on the asset side (assets) both develop to a certain scale, scale effects will occur, forming a closed business loop.The time point when this closed loop will be formed is the second half of next year just mentioned.

Of course, this does not mean that the market will be completely established by then.But the key is that if Nasdaq and Coinbase start to truly tokenize stocks in the United States, then funds and assets will be connected on the chain, and the closed loop will begin to operate.This also means that the prototype of the on-chain financial market will be officially available in the second half of next year.

Once the United States sets this example, what happens next is simple: countries around the world will learn, imitate, and follow.This is an inevitable process led by the United States and a global response.

Q: The global regulatory environment has changed a lot in the past two years. You also mentioned that regulatory tightening is an inevitable trend in the global market. Looking forward to the next 2 to 5 years, how do you predict the global regulatory trend in the short and medium term?

Xiao Feng: From a global perspective, there is no doubt that the United States is leading the world in legislation and system construction.

The legislative process in the United States is very fast, and it is expected that key bills will be implemented by the end of this year or early next year.The most noteworthy of these is the Crypto Market Structure Bill.The bill has passed the House of Representatives and is now being considered by the Senate.Even if it is too late in December this year, there is a high probability that it will be passed in January next year.

Why so sure?Because when the House of Representatives voted, we saw that this was a package that members of both parties supported highly.The same goes for the Stablecoin Bill.This means,Supervising the Crypto industry and establishing market structure is no longer a partisan dispute between the Republicans or Democrats, but a consensus among the elites of American society..Everyone believes that the United States must take the lead in Web3 and must do so.Once the bill is passed, I am optimistic that the industry will explode in the next two years.

First of all, the “legality” and “compliance” issues of all traditional financial institutions entering the Crypto industry will be completely resolved.What traditional institutions fear most is telling a good story but having flaws in compliance.If the law is not clear, they will not dare to enter the market in a big way.But if the legislation is completed and the obstacles are cleared, they will move in in a big way.

There was a clear sign recently: the U.S. Commodity Futures Trading Commission (CFTC) approved a federal-level cryptocurrency spot trading license.

CFTC approves federal-level cryptocurrency spot trading license; Source: CFTC official website

This is very critical.Under the new bill, regulatory authority over most crypto assets will be transferred to the CFTC.The fact that the CFTC dares to issue this license now shows that the legislation is a certainty – the regulation of crypto assets (except securities) must be under the jurisdiction of the CFTC.

Prior to this, there were no spot licenses at the federal level in the United States.In order to comply with regulations, Coinbase must apply for a “money transmission license” in each of the 50 states in the United States.Coinbase has a compliance team of hundreds of people to cope with the different regulatory rules of these 50 states.This is not only a huge monetary cost, but also a huge human cost.Now, with the CFTC’s federal license, institutions can carry out spot trading across the United States as long as they obtain this license.

Q: What impact will this series of actions by the United States have on the world, especially on China?

Xiao Feng: When the United States moves, the whole world will move.Europe is following suit, and so is Hong Kong, China.More importantly, this will definitely have an impact on mainland China.

This is competition at the financial market infrastructure level between old and new transaction clearing and settlement systems.When the world’s major economies are embracing distributed ledgers, embracing new financial infrastructure, and embracing tokenized financial assets, no one can stay away.In fact, the digital renminbi promoted by the mainland will also be a legal currency tokenization based on blockchain and distributed ledgers.

I think this is a trend we can definitely see in the next two years.

Q: Although traditional finance does have an inherent operating logic and has many problems, crypto finance (stablecoins, RWA) does have many advantages.But does this necessarily mean a “disruptive impact” will occur?After all, when you mentioned “distributed commerce” more than ten years ago, changes did not happen immediately.

Xiao Feng: You can regard the more than ten years from the birth of Bitcoin in 2009 to today as a huge social engineering experiment.Reconstructing the financial market system and turning “off-chain” into “on-chain” cannot be completed in three to five years.

But this experiment gave traditional finance the biggest revelation: Blockchain, as a new transaction clearing and settlement system, is feasible and extremely efficient.It takes three days to send money from New York to Hong Kong with the traditional system, but only two minutes with the blockchain.From a business perspective, when the new infrastructure reaches this level of efficiency and low cost, it is inevitable that it will replace the old system.

Q: Who will initiate the revolution that will replace the old order?

Xiao Feng: It must be a “spoiler.”Coinbase is such a disruptor.Coinbase’s current market capitalization was once larger than that of the New York Stock Exchange (NYSE).This is like a new “spoiler” saying to a century-old store: “I’m younger than you, but my market value is higher than yours, and I’m eating into your market.”Faced with this situation, if the traditional giants still can’t wake up, or are unwilling to give up because of vested interests, they can only watch being killed..But they cannot sit still and wait for death.

Nasdaq submitted plans to tokenize stock trading two months ago.This is 100% due to the stimulation of Coinbase.

In the first half of this year, when Coinbase submitted a plan to the SEC to conduct tokenized stock trading in the United States, Wall Street’s reaction was that it was “done” instantly.Why?Because comparing the two solutions, Coinbase’s solution is 100% based on the new transaction clearing and settlement system.

Wall Street’s existing system relies on DTCC (Depository Depository and Clearing Corporation), which operates through central registration, central depository, central counterparty trading and central clearing.The plan submitted by Coinbase is: “I don’t want DTCC, and I don’t want a central counterparty. I’ll do it all on the chain.” It is a point-to-point transaction, “transaction is settlement”, and settlement on a transaction-by-transaction basis.This is like if I give you 100 yuan and you give me two packs of cigarettes, the money and goods will be paid in full, and no third-party accounting is required.This is a “digital cash” transaction clearing and settlement model.

If Coinbase follows Coinbase’s plan, all the middle and back-office departments that keep Wall Street running will not be needed.This means that half of the people on Wall Street will lose their jobs.Those who do trading in the front office may be fine, but those who do liquidation in the back office will definitely lose their jobs.At that time, the entire Wall Street was in a panic.

I made a special call to a friend on Wall Street. He was responsible for the middle and back-office business of a large financial institution.I asked him: “I saw that Coinbase proposed a plan for tokenized stock trading. Does this have a big impact on you?” He told me: “Mr. Xiao, the entire Wall Street has been discussing that plan in the past two days. Everyone feels that it is over. Now their jobs are really not guaranteed.”

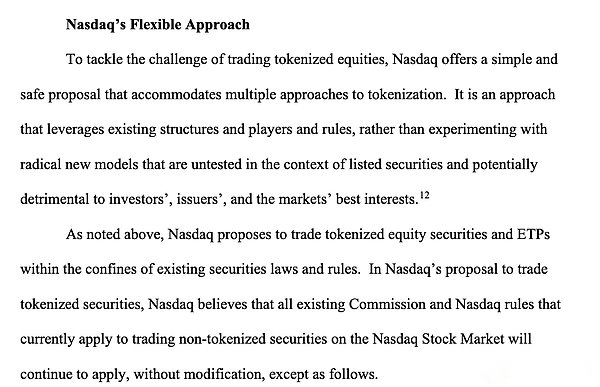

Nasdaq said that to address the challenges of tokenized stock trading, it provides a simple and secure solution that is compatible with multiple tokenizations.Source, SEC official website

Faced with this existential crisis, Wall Street began to fight back.Everyone thought: We can’t sit still and wait for death?So there is an alternative proposed by Nasdaq.The 40-page proposal can still be found on the SEC’s official website.Nasdaq proposed a completely different path from Coinbase: improvement.

Its core is: retain DTCC (Depository and Clearing Corporation), continue to do the central settlement of tokens, and let DTC be responsible for the tokenization and token settlement of custody assets.This means that it retains the original structure of Wall Street. Although it cannot be said that it has saved 100% of everyone’s jobs, it has at least saved the jobs of a large part of the people.

There are two sets of plans on the table now: Coinbase’s revolutionary faction, and Nasdaq’s reformist faction.

But please note that even if Nasdaq retains DTCC, it must adopt tokenization.Why?Because only tokenization can achieve 7×24-hour trading and clearing.If you can’t do it 24/7, you will definitely be doomed in the future competition.

To achieve real-time liquidation, tokenization is necessary.Because 24/7 transactions are only possible on new token-based financial infrastructure.

This is a very classic case: one side is the revolutionaries (Coinbase), and the other side is the reformists (Nasdaq).But no matter which faction you are on, you have to admit: new financial market infrastructure (blockchain/tokenization) is an irreversible trend.