Author: Haseeb, managing partner of Dragonfly; Translation: @bitchainvisionxz

I often warn entrepreneurs: the feedback you get after your project is launched will not be hate, but indifference.By default, no one cares about your new public chain.

But now I have to stop saying that.Monad just launched this week, and I have never seen a newly launched blockchain suffer so much malice.I have been investing professionally in the crypto space for over seven years.Before 2023, almost all newly launched public chains I have seen received either enthusiastic or indifferent feedback.But now, the new public chain has been accompanied by overwhelming criticism since its birth.Projects like Monad, Tempo, and MegaETH have faced a lot of criticism even before the mainnet was launched – this is indeed a new phenomenon.

I’ve been trying to figure out: why is this happening now?What kind of market psychology does it reveal?

1, the cure is worse than the disease

Disclaimer up front: this will be the least metrics-focused blockchain valuation article you’ll ever read.I don’t have any fancy indicators or charts to sell you.Instead, I’m going to push back against the zeitgeist of the crypto Twittersphere — one that I’ve been on the opposite side of for the past few years.

In 2024, I feel that what I am fighting against is financial nihilism.This is the view that all assets are irrelevant, that they are all memes at the end of the day, and that everything we build is inherently worthless.

Thankfully, that atmosphere has dissipated.We broke that spell.

But the current zeitgeist is what I call financial cynicism: OK, maybe some things do have value, and maybe they’re not all memes, but they’re grossly overvalued, and it’s only a matter of time before Wall Street discovers the truth.Not all public chains are worthless, but they are probably only worth 1/5 to 1/10 of what they are currently trading at (have you seen these P/E ratios?), so you better hope Wall Street doesn’t call our bluff or it will all go up in smoke.

Today, many bullish analysts are trying to build optimistic one-tier network valuation models, raising price-to-earnings ratios, gross margins, and discounted cash flows to try to combat this sentiment.

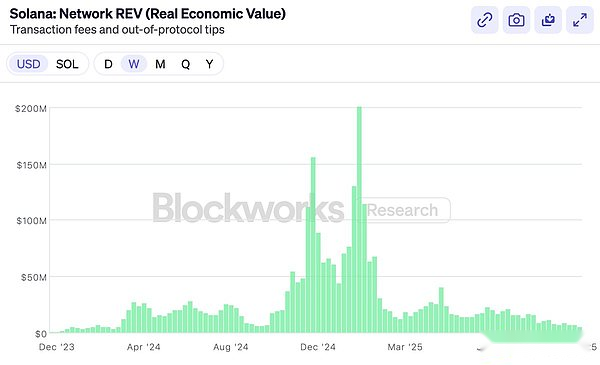

Late last year, Solana proudly adopted REV as the metric that ultimately justified its valuation.They proudly declare: We—and only we—are no longer calling Wall Street’s bluff!

However, as soon as REV was adopted, it almost immediately fell off a cliff (although it is worth noting that SOL performed better than REV).

It’s not that there’s anything wrong with the REV indicator itself.It is indeed a very clever measure.But the focus of this article is not on indicator selection.

Then Hyperliquid came on the scene.This decentralized exchange has real revenue, a buyback mechanism, and a price-to-earnings multiple.So everyone shouted – See, I told you so!Finally the first token with real profits and a reasonable price-to-earnings ratio has appeared (don’t mention BNB, we won’t discuss it).Hyperliquid will eat everything because clearly neither Ethereum nor Solana make money and we no longer have to pretend they have valuations.

Tokens that focus on repurchase, such as Hyperliquid, Pump, and Sky, are all excellent.But the market has always had access to exchanges—you could always buy Coinbase stock, BNB, or other underlying assets.We hold HYPE tokens and agree that it is an excellent product.

But that’s not the reason why people invest in ETH and SOL.The fact that the first-tier network does not have exchange-level profit margins is not their motivation to buy – if they were looking for profits, they could have bought Coinbase stock.

If you think this article is not a criticism of blockchain financial indicators, you may guess that I will condemn the original sin of the token industrial complex.

Apparently, everyone has lost money on tokens over the past year, including VCs.Altcoins have had a dismal year.So the other half of the mainstream voices on crypto Twitter are debating who to blame – who got greedy?Is the VC greedy?Wintermute greedy?Binance is greedy?Are Farmers greedy?Or is the founder greedy?

The answer is always the same: everyone is greedy.Venture capital, Wintermute, liquidity miners, Binance, KOL, including yourself, without exception.But that doesn’t matter because properly functioning markets never require anyone to act against their own interests.If we are right about the crypto industry, investing can still be successful even if everyone is greedy.Trying to analyze falling markets by identifying the “greedy” is as futile as launching a witch trial.I dare say that no one will suddenly become greedy in 2025.

Therefore this is not the topic to be discussed in this article.

Many people expect me to write an article arguing why MON should be valued at X or MEGA should be valued at Y.But I don’t want to write this kind of article, nor do I advise you to buy any specific target.In fact, if you don’t believe in them, you probably shouldn’t invest at all.

Can the new chain challenge be successful?No one knows.But if there is a real possibility of success, the market will price it accordingly.If Ethereum is worth $300 billion or Solana is worth $80 billion, then the price of a project that has a 1%-5% probability of becoming the next Ethereum or Solana will reflect this probability expectation.

Inexplicably, the crypto Twittersphere was outraged by this, but it’s not unlike the biotech world.For a drug with a probability of curing Alzheimer’s disease of less than 10%, even if there is a 90% chance that it will fail to pass Phase III clinical trials and its value will be reduced to zero, the market will still give it a multi-billion dollar valuation.This is where mathematical logic comes in – it turns out that markets are very good at calculations.Binary outcomes are priced based on probabilities, not growth rates or moral flaws.This belongs to the valuation philosophy of the “shut up and calculate” school.

I think there is no point in discussing this issue.”5% winning rate? Impossible, it’s obviously 10%!” For any individual token, the market is the best evaluator, not the article.

So what this article is really about is this: The crypto Twittersphere seems to no longer believe that public blockchains have value.

I don’t think this is because they question the ability of new public chains to gain market share – we just saw Solana rise from the ashes and dominate the market in less than two years.It’s not easy, but it can happen.

The deeper reason is that people gradually believe that even if the new public chain wins, there will be no prize worth fighting for.If ETH is just a meme and can never generate real revenue, then even if you win, you won’t get a $300 billion valuation.This contest is not worth participating in because all valuations are bubbles that will collapse before you claim your rewards.

Being optimistic about public chain valuations has become outdated.It’s not that no one is optimistic – there are clearly bulls in the market.What is sold must be bought. Although celebrities in the crypto Twitter circle are keen to badmouth the first-tier network, there are still people who feel comfortable buying SOL for $140 and ETH for $3,000.

But now there is a popular perception: the smartest people have long stopped buying smart contract public chains.A wise man knows that the trick is gone, either now or soon.The only ones buying now are the ones who have taken advantage of them – online ride-hailing drivers, Tom Lee and the like, and KOLs who talk about “trillion market value”.And maybe the U.S. Treasury Department.But it is definitely not smart money.

This is pure bullshit.I don’t believe this, and neither should you.

Therefore, I feel it is necessary to write a “Smart Man’s Manifesto” to explain the value of a universal public chain.This article has nothing to do with Monad or MegaETH, but is actually a defense of ETH and SOL.Because if you recognize the value of ETH and SOL, the rest of the inferences will follow.

It’s not my job as a venture capitalist to defend the valuations of ETH and SOL, but since no one wants to do it, I’ll do it.

2, perception of exponential growth

My partner Bo has personally experienced China’s Internet wave as a venture capitalist.Although I am numb to the argument that “the encryption industry is like the Internet”, every time I listen to him talk about the past, I am always reminded of the cost of misjudgment of trends.

He often tells a story: At the beginning of the 21st century, when all the early e-commerce venture capital investors (it was just a small circle at the time) got together to drink coffee, they debated how big the e-commerce market would be.

Will it mainly sell electronic products (maybe only geeks can use computers)?Can it appeal to female users (perhaps they value touch more)?What about fresh food (perishables may not be manageable)?For early-stage venture capital investors, the answers to these questions directly determine investment direction and valuation logic.

Of course it turned out – they were all wrong.E-commerce will sell everything, and its target customers are all over the world.But no one really believed this at the time, and even if some people did, they were too ridiculous to say it openly.

Only if you wait long enough, exponential growth will emerge.Even among those who believed in e-commerce at the time, few thought it could reach the scale it later achieved.And those few who firmly believe in it and insist on holding it almost all become billionaires.Other VCs—and Bo says he was one of them—sold out prematurely.

Today in the crypto space, believing in exponential growth is an outdated notion.But I believe in the exponential laws of the crypto world.Because I’ve experienced it myself.

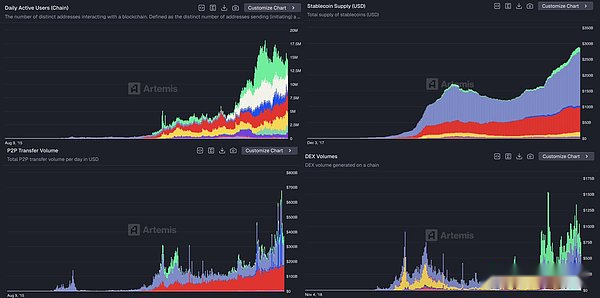

No one was using these technologies when I first started: they were small, full of bugs, and the experience was terrible.The total amount locked on the chain is only a few million dollars.When we invested in the first-generation DeFi projects—MakerDAO, Compound, and 1inch—they were still experimental products.I worked with EtherDelta which had only a few million dollars in daily trading volume and it was considered a huge success at the time.Today, the daily transaction volume on the chain regularly exceeds tens of billions of dollars.I used to think it was ridiculous that the circulation of Tether exceeded 1 billion and was reported by the New York Times as a Ponzi scheme on the verge of collapse. Now the scale of stablecoins exceeds 300 billion US dollars and is regulated by the Federal Reserve.

I believe in exponential growth because I’ve seen it happen time and time again.

But you may refute: The growth of stablecoins may be exponential, and DeFi transaction volume may be too, but the value has not been deposited in ETH or SOL.Public chains fail to capture these values.

My answer to this is: You still don’t believe in the law of exponentials.Because the answer to exponential growth is always the same: it doesn’t matter.The scale of the future will be far greater than imagined today. When great changes come, the scale effect will make up for everything.

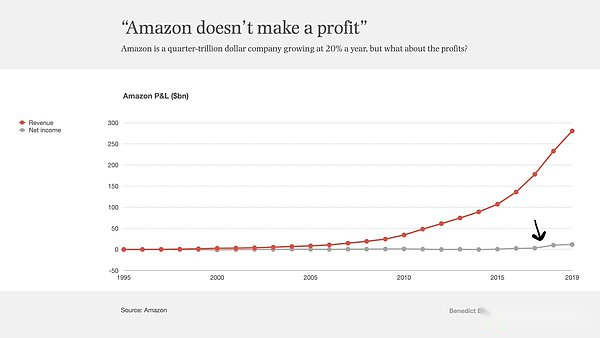

Please see the picture below.

This is Amazon’s income statement from 1995 to 2019, a time span of 24 years.The red line represents revenue and the gray line represents profit.See that little section of gray line rising slightly at the end?That was Amazon’s 22nd year when it started to truly make a profit.

When the gray line representing net profit first left zero, Amazon had been around for 22 years.Every year before that, there were op-eds, critics, and short sellers claiming that Amazon was a Ponzi scheme that never turned a profit.

And Ethereum just turned 10 years old.Here’s how Amazon stock performed in its first decade:

A decade of turmoil.During this period, Amazon has been surrounded by doubters and critics: Is e-commerce just a philanthropy subsidized by venture capital?They dump low-quality small goods at low prices to freeloaders, who cares?How can they actually make money like Walmart or GE?

If you were arguing about Amazon’s P/E ratio, you were in the wrong paradigm – it was the linear growth paradigm.But e-commerce is not a linear trend, so everyone who has argued about the P/E ratio in the past 22 years has been terribly wrong.No matter how much you bid, no matter when you buy, you are never bullish enough.

Because this is the law of exponential growth.With truly exponential technology, no matter how large you think it can reach, it will always exceed your imagination.

This is what Silicon Valley always knows better than Wall Street.Silicon Valley thrives on exponential growth, while Wall Street is steeped in linear thinking.Over the past few years, the center of gravity in the crypto world has shifted from Silicon Valley to Wall Street—and you can feel the change.

Admittedly, crypto growth is not as smooth as e-commerce growth.It is more explosive, with intermittent leaps.This is because encryption involves currency, is deeply tied to macro forces, and is subject to more intense regulatory tug-of-war than e-commerce.Crypto directly attacks the country’s lifeblood – currency – and therefore makes the government more uneasy than e-commerce.

But the inevitability of exponential growth remains undimmed.This is a crude argument, but if encryption is indeed exponential, then this crude argument is correct.

Look further away.

Financial assets crave freedom.They long to open up.They crave connectivity.Cryptotechnology converts financial assets into file formats, making sending dollars or stocks as easy as sending a PDF.It allows all things to talk to each other and realize an all-weather, global, and interconnected open ecosystem.

Openness will win out.This is the core rule I learned from the Internet era.Vested interests will resist and governments will bluff, but ultimately they will succumb to the ubiquity, creativity and extreme efficiency this technology brings.Just as the Internet has reshaped all industries, blockchain will engulf the entire financial and monetary system in the same trend.

Yes—given enough time—devour them all.

There is an old saying: People always overestimate the changes in two years but underestimate the changes in ten years.

If you believe in exponential growth, if you zoom out enough, everything still looks cheap.There are daily holders who outlast the sellers and naysayers – which should keep you humble.Big capital has a much longer time horizon than swing traders on crypto Twitter would have you believe.Historical lessons have taught big capital not to buck the trend and resist major technological changes.Remember the big story that first made you buy ETH or SOL?Big capital still believes that story and has never stopped.

So, what is my core argument?

I argue that applying price-to-earnings ratios to smart contract public chains (what is currently known as the “income meta-narrative”) is actually giving up on exponential growth.This means that you have classified this industry into a linear growth paradigm, which means that you believe that the 30 million daily active users on the chain and less than 1% of the total M2 currency are the end point – the encryption world is just one of thousands of industries and a marginal supporting role.It didn’t win, nor was it inevitable.

More importantly, I call on people to become believers in it.Not just a believer, but a long-term believer.

I firmly believe that this exponential change will transcend anything you are involved with in your lifetime.This is your “e-commerce revolution”.When you look back when you are old, you will tell your children and grandchildren – I have experienced this great change.Not everyone believes that social systems can be restructured, or that programs running on our collectively owned decentralized computers can revolutionize money and finance.

But it does happen.It changes the world.

And you were once one of them.