Author: Prathik Desai, Source: Token Dispatch, Compiler: Shaw Bitcoin Vision

Introduction

There’s a simple theory behind why companies keep cryptocurrencies on their balance sheets.If the assets they purchased appreciate in value, their stock prices should rise as well.The purpose of Corporate Cryptocurrency Holding is to provide investors with a clearer, more leveraged way to hold cryptocurrencies, managed by a trusted team.

This strategy works well in a bull market because almost any strategy will work in this market environment.But in a bear market, this strategy doesn’t work so well because the logic works the other way around.

By most traditional definitions, cryptocurrencies have officially entered a bear market.Bitcoin (down about 30%), Ethereum (down about 40%) and Solana (down about 55%) are all well below their peaks and have all fallen below their 200-day moving averages.Bitcoin spot ETFs, which were expected to represent stable, regulated demand, have experienced net outflows for three consecutive weeks.On-chain data indicators also confirm this.Bitcoin’s realized market capitalization ratio (MVRV) has fallen to its lowest level two years ago, with many holders already in the red.

If the majority of your company’s assets are in cryptocurrency, that’s not a good situation.What’s even worse is if the market no longer sees you as a company but instead sees you as a publicly traded cryptocurrency wallet and your employees as the source of its value.

This is what is happening right now with Digital Asset Treasury (DAT).This article will present a “what if” scenario that was once considered an extremely rare occurrence for DAT and is now a reality with the advent of the bear market.

DAT dilemma has emerged

Digital asset treasury (DAT) refers to businesses that intentionally or unintentionally become publicly listed cryptocurrency investment vehicles and have operating departments.For much of the past year, the market viewed it as a high-beta version of the underlying cryptocurrency.During a market downturn, a high beta becomes less attractive.

Now that the economic recession has arrived, the situation is quite serious.A few months ago, when I wrote my first quantitative analysis article, DAT stock had already retreated from its highs.The risks were clear at the time, but seemed far away.Now, these risks are imminent.

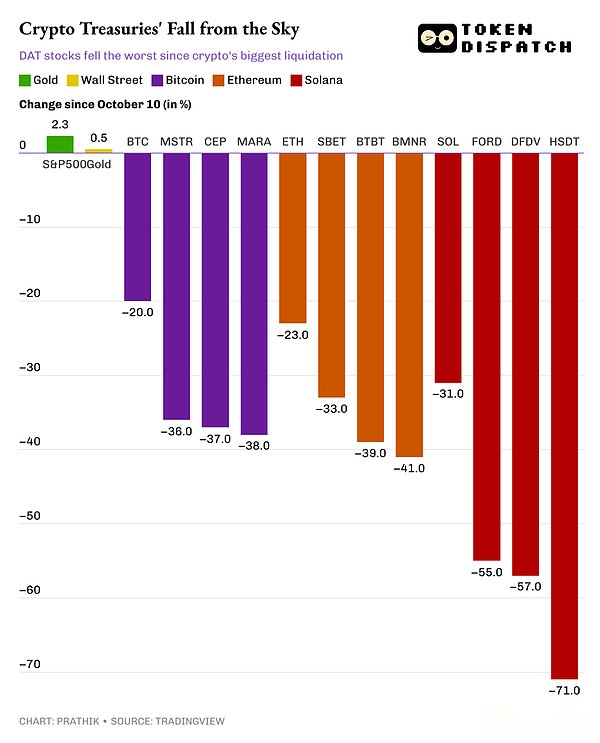

Since the worst liquidation in cryptocurrency history in October, DAT’s stock price has fallen far more than the price of the tokens it holds.

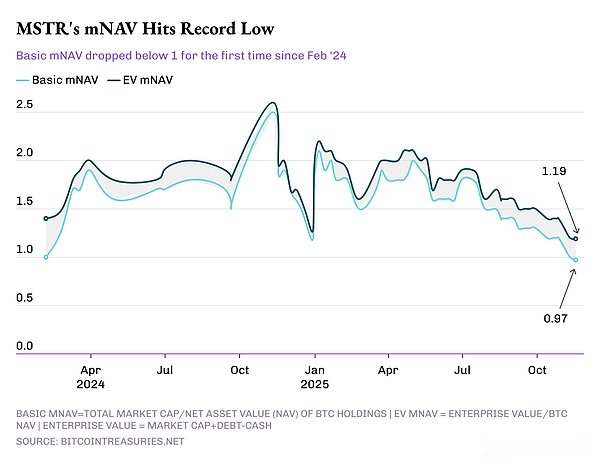

Their market capitalization to net asset value ratio (mNAV) – the simplest measure of the market’s valuation of their treasury reserves – has fallen to 1 or lower.Even Strategy (formerly MicroStrategy), the most well-known representative of corporate Bitcoin strategies, currently has its mNAV at its lowest in 21 months.

This is all expected and not shocking.It’s just that the bear market has transformed the theoretical risks of Bitcoin treasury trading, including dilution, leverage, cyclical fluctuations and investor patience, into observable and measurable realities.The “what if” question now appears in the mNAV chart.

The mNAV factor and why the market is suddenly paying attention to it

If you hold Bitcoin, you know what you own.But if you hold shares in a company that holds Bitcoin, the situation is a little more complicated.Different DATs may vary.Taking Strategy as an example, you may hold low-interest bonds, which you can choose to convert into company stock when they mature.

A simple way to measure this complexity is to use mNAV.It reflects how much extra shareholders are willing to pay for such packaging.

When the mNAV ratio is above 1, shareholders believe the packaging adds value to the company’s existing business.They may be bullish on the management team, growth prospects, or believe that a company with a Bitcoin balance sheet should have more upside potential than Bitcoin itself.Sometimes they just enjoy the volatility.Sometimes this is more attractive and a more direct path for traditional investors who have never dabbled in cryptocurrencies.

When mNAV is below 1, investors believe the company is worth less than the value of their cryptocurrency holdings.

Decline in value may be due to excessive cryptocurrency leverage, poor operating performance, or poor corporate governance.But the basic concept of an mNAV below 1 is simple: buying the company gives you less exposure to the crypto asset than buying the asset directly.

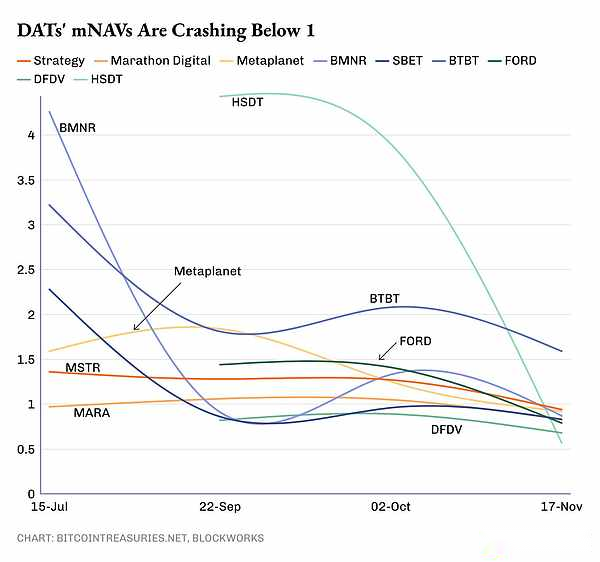

For much of 2025, the cryptocurrency treasury company’s mNAV has been slowly declining after experiencing the initial growth typically experienced by newly formed DATs.Since October, these companies’ mNAV has been close to or below 1.

It also becomes difficult to issue new shares at a premium when mNAV falls below 1, making it difficult to fund additional cryptocurrency purchases.Most DATs supplement their treasury through equity financing, including issuances at market price (ATM), follow-on issuances, or bonds convertible into equity.This economic model can only work effectively if the stock trades at a price higher than the value of the tokens held per share.

This pattern is prevalent across cryptoassets and companies of all sizes.Whether it is Bitcoin, Ethereum or Solana Treasury, its mNAV has tended to be close to 1, or even fell below.Small, experimental and flagship projects are not immune.The reasons may vary from person to person – some think it’s leverage, some think it’s dilution, others think it’s a business model issue.But the market has made it clear that this form of packaging has its own risks, while the underlying assets do not.

In some cases, investors still value a company for less than the value of its cryptocurrency holdings, even when taking into account its other businesses.Strategy is the best example.

A shaky Strategy?

Michael Saylor’s Strategy has been the world’s most high-profile proving ground for DAT strategies.It executes this strategy consistently and at scale.This is the purest corporate bet on Bitcoin’s long-term appreciation in the public markets.

However, its mNAV is currently at a 21-month low and is now below 1.

Throughout much of 2024 and into early 2025, Strategy traded at a considerable premium to the value of its Bitcoin holdings.Investors view its stock, MSTR, as a leveraged Bitcoin exposure vehicle with an operating business attached.In cyclical markets, this premium makes sense: companies accumulate Bitcoin, Bitcoin prices rise, and the leverage effect amplifies the stock’s upside potential.

The same logic now applies in reverse.

Strategy’s underlying mNAV fell below 1 for the first time since early 2024.The company has slowed its Bitcoin purchases over the past two months.But as I type this, my phone reminds me that Strategy has added 8,178 more Bitcoins to its treasury.However, the risks to the system remain significant.

Because of this example, the DAT route now looks riskier than ever.Cracks in the entire packaging strategy began to appear when investors became suspicious of projects that had a first-mover advantage and where the average purchase cost of Bitcoin was less than $75,000.

Bitcoin buying slows

Another worrying sign is that businesses are buying less Bitcoin.

Since August 1 this year, DAT has purchased a total of 115,000 Bitcoins, of which only 17,000 were purchased after October 11.This includes Strategy’s purchase of 8,178 Bitcoins at the time of writing.In the two months leading up to the October liquidation event, DAT had added 90,000 Bitcoin to its treasury.

While doing so is rational in a bear market, it also exacerbates the problem of mNAV premium.If a company does not increase its reserves when prices fall, this indicates negativity within the DAT management team.This could lead shareholders to question whether the company’s operations are strong enough to warrant continuing to add to their holdings.Once such doubts arise, the mNAV premium disappears.

Where to go next?

For much of the past year, DAT businesses and cryptocurrencies were viewed as interchangeable concepts.But this is not the case.Cryptocurrencies have no debt covenants or operating losses, whereas companies do not.These DATs still need to post good results to maintain investor confidence.

The bear market exposed old problems that have always existed with DAT and served as an important wake-up call for investors.

Cryptocurrency leveraged exposures will now appear more dangerous, and underlying operations will be thoroughly scrutinized.Continuous and stable accumulation will be difficult to package into a marketing slogan.All of this will be reflected in mNAV.