pickwant

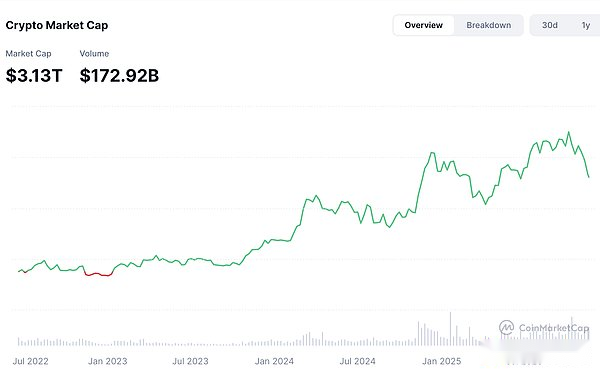

At the end of 2025, the crypto market was in a period of deep shock driven by a high degree of macroeconomics: Although Bitcoin is still in the high range of US$90,000, sentiment has fallen to the level of extreme fear since the 2020 epidemic. Huge single-day outflows of ETFs, structural changes in the hands of giant whales, and retail investors cut their flesh together to form a typical “chip redistribution” in the middle of a bull market.At the same time, expectations for U.S. interest rate cuts have been repriced, and concerns about maintaining high interest rates have significantly compressed the valuation of risky assets.Although external macro liquidity has not worsened – Japan, China, and Europe are all turning to easing – the pace relies more on single-point data, leaving the market in a rare combination of “liquidity-friendly and cold emotions”.The credit pressure of the AI bubble has also intensified cross-asset risk transmission, squeezing crypto assets in terms of funds, attention, and narrative.Against this background, the crypto market is entering a structural stage of migration from weak hands to strong hands, laying the foundation for the next cycle.

1. Macroeconomic Analysis of the Crypto Marketanalyze

At the epicenter of the market turmoil in the past few weeks, Bitcoin’s price and sentiment have experienced a rare and huge divergence: the price remains firmly in the historically high range above $90,000, but market psychology has fallen into the abyss of “extreme fear.”The Fear and Greed Index briefly hit 16 points, the coldest sentiment reading since the global pandemic collapsed in March 2020, and even with a slight recent recovery, it is struggling in the 12–18 range.The positive narrative of Bitcoin on social media has simultaneously declined, quickly turning from the previous firm optimism to complaints, anger and blame-shifting.This kind of dislocation is not accidental, it often appears in the middle and late stages of bull markets: players who entered the market early have already accumulated huge floating profits, and they choose to settle down once there is a macroeconomic disturbance; while the funds chasing higher in the later period are quickly locked up in the short-term fluctuations, and the floating loss sentiment further amplifies the panic and disappointment in the market.Bitcoin is currently about US$92,000, which is almost the same as the beginning of the year (about US$90,500). After experiencing a sharp rise and deep correction throughout the year, it has returned to near the starting point, showing a trend of “high fluctuations and staying put”.

On-chain fund flows provide a more direct signal than sentiment.First, the role of spot ETFs has changed from the “supercharger engine” driving the bull market to a short-term “drainage pipe.”Since November, ETFs have recorded cumulative net outflows of more than US$2 billion, with the largest single-day outflow reaching nearly US$870 million, setting a new record since its listing.The impact at the narrative level is far greater than the capital itself: before, the logic of “institutional long-term allocation” was the core support point of the market. Now this support has turned to reducing positions, making retail investors feel the insecurity of “having no adult to back them up.”The behavior of giant whales also shows obvious differentiation.Medium-sized whales holding 10–1000 BTC have continued to become net sellers in the past few weeks, selling tens of thousands of Bitcoins. It is obvious that veteran players who have made early arrangements and made huge profits choose to cash out.Super whales with a volume of more than 10,000 BTC are simultaneously increasing their holdings. On-chain data shows that some long-term strategic entities have bucked the trend and accumulated funds in the fall, reaching tens of thousands of BTC.

At the same time, the net inflow of small retail investors (≤10 BTC) is also slowly rising, which shows that although the most emotional novice users may be closing their positions in panic, another group of more experienced long-term retail investors are seizing the opportunity to increase their positions.The realized loss indicator on the chain even recorded the largest one-day loss record in the past six months. A large number of chips were forced to sell at a loss, and the typical “surrender selling” signal clearly emerged.Combining various on-chain indicators, what we see is not a complete withdrawal of the market, but a rapid redistribution of chips – from the concentration of short-term, emotional funds to entities with longer capital patience and stronger risk tolerance. This is a structural phenomenon that will appear in the middle and later stages of all previous bull markets.The market is currently in a period of high volatility in the second half of the bull market – although the market value has corrected but is still on a strong platform, sentiment has cooled significantly, structural differentiation has intensified, and high-quality assets are resisting the decline, but speculative assets continue to be cleared.The overall market capitalization of the crypto market is on a downward trend.

If on-chain and sentiment explain short-term fluctuations, then the real driver of this round of market trends is still macro interest rates – the real “bookmaker” of Bitcoin is not institutions or whales, but the Federal Reserve.In the last quarter, the market was widely betting that the Federal Reserve would gradually begin a rate-cutting cycle in the second half of 2024 to early 2025.Cutting interest rates means a recovery in liquidity and an increase in the valuation of risky assets, and therefore has become an important driving force for the last round of gains.However, a series of recent economic data and official statements have caused this expectation to be strongly repriced.Although U.S. employment and inflation have slowed, they have not yet reached a level that can support radical easing; some officials have even released hawkish signals of “cautious interest rate cuts,” causing the market to worry that interest rates may remain high for longer than originally expected.The cooling of expectations for interest rate cuts will directly reduce the discounted value of future cash flows, thereby compressing the valuation of risky assets. Highly elastic sectors such as technology growth, AI, and encryption are the first to bear the brunt.Therefore, the recent decline is not due to the lack of new narratives in the crypto industry, but at the macro level, which directly increases the “discount rate” of the entire risky asset universe, which is a violent valuation reduction.

2. The deep impact of the AI bubble on the crypto macro economyring

From 2023 to 2025, artificial intelligence will overwhelmingly become the core force in global risk asset pricing, replacing old narratives such as “Metaverse”, “Web3” and “DeFi Summer” and becoming the number one driving force for the expansion of capital market valuations.Whether it is Nvidia’s market value exceeding one trillion US dollars, OpenAI’s infrastructure ambitions, or the explosive growth of super data centers and sovereign AI projects, the entire market has completed a paradigm shift from “tech growth” to “AI craze” in just two years.However, behind this feast are increasingly fragile leverage structures, increasingly large capital expenditures, and financial engineering that increasingly relies on “internal circulation.”The rapid expansion of AI valuations has made the entire high-risk asset system more fragile. Its fluctuations are directly and continuously transmitted to the encryption market through risk budgets, interest rate expectations and liquidity conditions, profoundly affecting the cycle structure and pricing framework of Bitcoin, Ethereum and altcoins.

In the institutional asset allocation system, AI leaders have transformed from growth stocks in the traditional sense to “super technology factors” and have become the center of high-risk portfolios, even with endogenous leverage effects.When AI rises, risk appetite expands, and institutional allocations to high-risk assets, including Bitcoin, naturally increase; and when AI experiences violent fluctuations, valuation pressures, or credit concerns, risk budgets are forced to shrink, and model-driven and quantitative trading will quickly reduce overall risk exposure. Cryptoassets—as the most volatile part without cash flow support—often become the priority target for lightening positions.Therefore, the tug-of-war and correction in the later stages of the AI bubble will simultaneously amplify the magnitude of adjustments in the crypto market at the emotional and structural levels.This was particularly evident in November 2025: when AI-related technology stocks adjusted due to financing pressure, rising credit spreads, and macro uncertainty, Bitcoin and U.S. stocks fell below key ranges simultaneously, forming a typical “cross-asset risk transmission.”In addition to risk appetite, the liquidity squeeze-out effect is the core suppression factor of the AI bubble on the crypto market.In the macro environment of “limited capital pool”, this will inevitably mean that the marginal funds of other high-risk assets are compressed, and cryptocurrency has become the most obvious “fund victim”.

The deeper influence comes from the competition of narrative systems.In the construction of market sentiment and valuation, the importance of narrative is often no less important than fundamentals.In the past decade, the encryption industry has gained widespread attention and a large premium by relying on narratives such as decentralized finance, digital gold, and open financial networks.However, the AI narrative from 2023 to 2025 is extremely exclusive, and its grand narrative framework – “the core engine of the fourth industrial revolution”, “computing power is the new oil”, “data centers are the new industrial real estate” and “AI models are the economic infrastructure of the future” – directly suppresses the narrative space of the encryption industry.At the policy level, media level, scientific research level, and investment level, almost all attention is focused on AI. Crypto can only regain its right to speak when global liquidity completely relaxes.This makes it difficult for the encryption industry to regain valuation premiums even if the data on the chain is healthy and the developer ecosystem is active.However, when the AI bubble enters the bursting or deep adjustment stage, the fate of crypto assets may not be pessimistic, and may even usher in decisive opportunities.If the AI bubble evolves along the path of the 2000 dot-com bubble—that is, experiencing a 30%–60% valuation correction, some highly leveraged, highly story-driven companies liquidating, and technology giants cutting capital expenditures, but the overall credit system is stable—then the short-term pain in the crypto market will be exchanged for major mid-term benefits.If the risk evolves into a credit crisis similar to that of 2008, although the probability is limited, the impact will be more severe.The break in the technology debt chain, the concentrated defaults of data center REITs, and the damage to bank balance sheets may trigger a “systemic deleveraging” and cause cryptocurrency to experience a waterfall-like plunge similar to March 2020 in the short term.But such extreme situations often also mean a stronger mid- to long-term rebound, as central banks will be forced to restart QE, cut interest rates and even adopt unconventional monetary policies.Cryptocurrency, as a tool to hedge against excessive currency issuance, will usher in a strong recovery in an environment of flooding liquidity.

Taken together, the AI bubble is not the end of the crypto industry, but the precursor to the next big crypto cycle.During the rising bubble period, AI will squeeze the funds, attention, and narrative of crypto assets; while during the bursting or digestion period of the bubble, AI will release liquidity, risk appetite, and resources back, laying the foundation for the restart of the crypto industry.For investors, understanding this macro transmission structure is more important than predicting prices; the emotional freezing point is not the end, but a critical stage in the migration of assets from weak hands to strong hands; the real opportunities are not in the hustle and bustle, but are often born around the time when the macro narrative switches and the liquidity cycle reverses.The next big cycle in the encryption market is likely to officially start after the AI bubble ebbs.

3. Opportunities and challenges under the crypto macro market changesfight

The global macro environment at the end of 2025 is showing structural changes that are completely different from those in previous years.After a two-year tightening cycle, global monetary policy has finally ushered in a synchronized turn. The Federal Reserve has implemented two interest rate cuts in the second half of 2025, and at the same time confirmed that quantitative tightening has officially ended and the balance sheet shrinkage has stopped. The market expects a new round of interest rate cuts in the first quarter of 2026.This means that global liquidity has shifted from “pumping” to “supplying”, M2 growth has returned to the expansion channel, and the credit environment has significantly improved.For all risk assets, such cyclical turns often mean that new price anchors are forming.For the crypto market, the time when the world enters the easing cycle coincides with multiple factors such as internal leverage cleaning, emotional freezing point, and ETF outflow bottoming out, forming the basis for 2026 to become a “restart point.”Synchronized global easing is uncommon, but the macro pattern in 2025–2026 shows a high degree of consistency.Japan launched a fiscal stimulus plan of more than 100 billion US dollars and continued its ultra-loose monetary policy; China further strengthened both monetary and fiscal easing under economic pressure and structural needs; Europe began to discuss restarting QE on the edge of economic recession.The adoption of easing policies by the world’s major economies at the same time is a super positive factor that has never been seen in crypto assets in recent years.The reason is that cryptoassets are inherently one of the most sensitive asset classes to global liquidity, and Bitcoin in particular has valuations that are highly correlated with U.S. dollar liquidity cycles.When the world enters a “loose + weak growth” environment at the same time, the attractiveness of traditional assets decreases, and liquidity spillovers will prioritize the search for higher-beta assets. It is under this macro-background that crypto assets have exploded in the past three cycles.

At the same time, the endogenous structure of the crypto market has gradually returned to robustness from the turbulence of 2025.Long-term holders (LTH) did not see a sharp sell-off, and on-chain data showed that chips were moving from emotional sellers to high-conviction buyers; whales continued to accumulate funds when prices dropped deeply; the large-scale outflows of ETFs mainly came from retail investor panic, rather than institutional retreat; the Funding Rate in the futures market returned to the neutral or even negative range, and leverage was completely squeezed out of the market.This combination means that the market’s selling pressure mainly comes from weak hands, while chips are concentrating on strong hands.In other words, the crypto market is in a similar position to Q1 2020: valuations are suppressed, but the risk structure is far healthier than it appears.However, the other side of the opportunities is challenges.Although the easing cycle is returning, the spillover risk of the AI bubble still cannot be ignored.The valuation of technology giants is already close to an unsustainable range. Once there is a deviation in the capital chain or profit expectations, technology stocks may undergo drastic adjustments again, and crypto-assets, as high-risk peers, will inevitably passively withstand “systemic beta selling.”Furthermore, Bitcoin lacks decisive new catalysts in the short term.The ETF model of 2024–2025 has been fully traded by the market, and the new main narrative needs to wait to see whether the Federal Reserve starts QE, whether large institutions return to the path of accumulation, and whether traditional finance accelerates the deployment of crypto infrastructure.The continued outflow of ETFs reflects the extreme fear of retail investors. It will still take time for the panic index to fall to the extreme value of 9 to complete the “capitulation bottom”, and the market needs to wait for new incremental signals.Based on the macro environment and market structure, from a time perspective, the crypto market will continue to fluctuate and bottom out from 2025 Q4 to 2026 Q1.AI bubble pressure, ETF outflows and macro data uncertainty have jointly pushed the market to maintain a weak and volatile pattern.However, with the acceleration of interest rate cuts in the first and second quarters of 2026 and the return of substantial liquidity, BTC is expected to return to above $100,000, and in 2026 Q3–Q4, with the superposition of factors such as QE expectations, the new DePIN/HPC narrative, and the national reserve of BTC, a new bull market cycle will be confirmed.Such a path means that the crypto market is moving from a “valuation killing phase” to a “repricing phase”, and a true trend reversal requires liquidity and narrative resonance.

Investment strategies in this landscape need to be recalibrated to cope with volatility and capture opportunities.Divided positioning (DCA) has the best statistical returns in extreme fear zones and is the best way to hedge short-term noise and emotional fluctuations.In terms of position structure, the proportion of altcoins should be reduced and the weight of BTC/ETH should be increased, because altcoins will fall deeper when risk control is compressed, and the ETF accumulation mechanism will continue to strengthen Bitcoin’s relative advantage in the medium term.Given that technology stocks may experience another round of “Internet bubble-style” deep adjustments, investors need to retain an appropriate amount of emergency funds in order to obtain the best entry point when macro risk events trigger excessive declines in crypto assets.From a long-term perspective, 2026 will be a critical year for global liquidity redistribution and a year when the crypto market returns to the main stage after experiencing structural purges, and the real winners will be those who persist in discipline and patience when emotions are at their coldest.

Four.knotOn

Combining the on-chain structure, sentiment indicators, capital flows and the global macro cycle, this round of decline is more like a violent change of hands in the middle and late stages of the bull market, rather than a structural reversal.The repricing of interest rate expectations has put pressure on short-term valuations, but the world’s entry into a clear easing channel, synchronized stimulus in Japan and China, and the end of QT mean that 2026 will be a key year for liquidity to re-expand.The AI bubble may continue to bring short-term drag, but its bursting or digestion will release occupied capital and narrative space, providing new valuation support for scarce assets such as Bitcoin.It is expected that the market will still be dominated by shocks in 2025 Q4-2026 Q1, and 2026 Q2-Q4 driven by the interest rate cut cycle will become a trend reversal window.Disciplined DCA, increasing the weight of BTC/ETH and retaining emergency positions are the optimal strategies to ride through fluctuations and welcome the new cycle.