Author: Trading Strategy; Translation: @bitchainvisionxz

Stream xUSD is actually a “tokenized hedge fund” disguised as a DeFi stablecoin, claiming to adopt a delta neutral strategy.Now the fund is insolvent amid many doubts.In the past five years, multiple projects have followed the same routine and tried to bootstrap their token ecosystem through the income generated by delta-neutral investments.Successful cases include: MakerDAO, Frax, Ohm, Aave, Ethena.

Unlike many of its purer DeFi competitors, Stream has always lacked transparency about its strategies and positions.On portfolio trackers such as DeBank, only $150 million of its claimed $500 million total locked value is visible on-chain.The truth is that Stream invested funds in off-chain trading strategies operated by self-operated traders, and some traders were forced to liquidate their positions, leading to losses claimed to reach US$100 million.

1.CCNRelated reports

Monday’s $120 million Balancer DEX hack has nothing to do with this.

According to rumors (which we cannot confirm as Stream does not disclose it publicly), its off-chain trading strategy allegedly involves “shorting volatility.”In quantitative finance, “shorting volatility” refers to using a trading strategy to profit when market volatility decreases, remains stable, or when realized volatility is less than the volatility implied in the pricing of financial instruments.If the price of the underlying asset does not fluctuate significantly (i.e., a low-volatility environment), the option may expire, allowing the seller to retain the premium as profit.However, this method carries significant risks – a sudden increase in volatility can lead to huge losses, and is often described as “picking coins in front of a steamroller”.

2, detailed information about shorting volatility

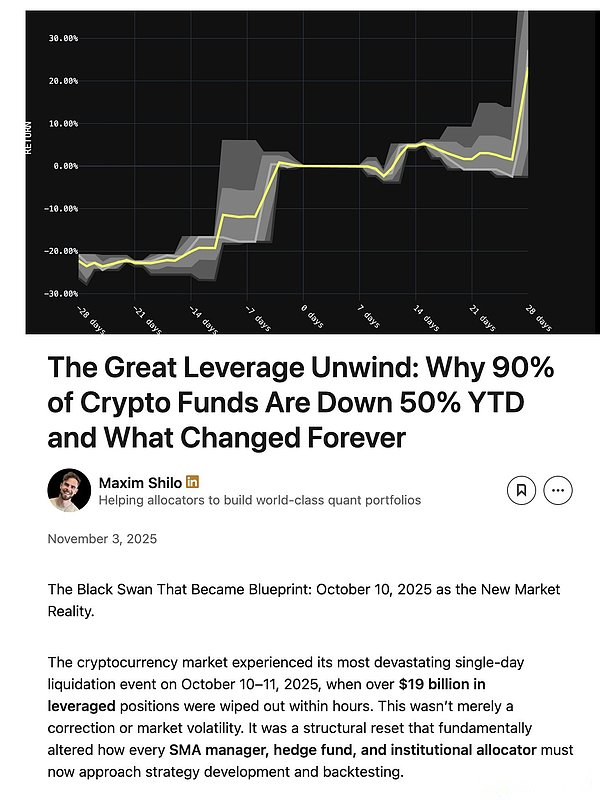

We are experiencing such a “volatility spike” on “Black Friday” October 11th.With the market frenzy driven by the Trump craze in 2025, the systemic leverage risk accumulated in the cryptocurrency market for a long time has reached a high level.When Trump announced new tariffs on the afternoon of Friday, October 11, all markets fell into panic, which quickly spread to the cryptocurrency space.In panic, selling safe-haven assets first becomes the rule of survival.The sell-off triggered a chain of liquidations.

Since the long-term accumulation of leverage risk has kept systemic leverage at a high level, the perpetual contract market lacks sufficient depth to smoothly liquidate all leveraged positions.In this case, the automatic deleveraging (ADL) mechanism kicks in and starts distributing losses to profitable traders.This further distorts an already frenzied market.

3, What is automatic deleveraging?

The volatility caused by this incident is a once-in-a-decade phenomenon in the cryptocurrency market.While not unprecedented – similar plunges have occurred in cryptocurrency markets as early as 2016 – due to the lack of reliable data from this period, most algorithmic traders have based their strategies on recent “smooth swing” data.Since there have been no such violent fluctuations recently, even positions with a leverage ratio as low as about 2 times have been broken down.

Maxim Shilo provides an in-depth analysis of the impact of this event on algorithmic traders and how “Black Friday” may permanently change the cryptocurrency trading landscape:

4,Maxim Shilotalk10month11How Japan is Changing the Cryptocurrency Algorithmic Trading Landscape

Now, the first victims of the “Black Friday” incident have emerged, and Stream has not been spared.

The definition of a delta neutral fund should be that there is no possibility of loss.If a loss occurs, by definition it cannot be called delta neutral.Stream once promised to remain delta neutral, but invested in a non-transparent, off-chain self-operated strategy without everyone knowing.Delta neutrality isn’t always black and white, and it’s always easy to judge after the fact.Many experts may consider these strategies too risky to be considered truly delta neutral – as they can backfire.And they do backfire.

When Stream lost principal on these failed trades, it fell into insolvency.

DeFi itself has risks, and some fund losses are acceptable.If the annualized return reaches 15%, even if there is a one-time drawdown of 10%, the principal can still be restored to 100%, which is not a devastating blow.However, Stream also pushed its own leverage to the limit through a “recursive loop” lending strategy with another stablecoin, Elixir.

5, What is a recursive loop?

Recursive loops (also known as recursive lending loops) are a leveraged yield farming strategy in the decentralized finance (DeFi) lending market.Its core mechanism is to borrow repeatedly with deposited collateral (often using borrowed assets as new collateral), thereby enlarging the exposure to interest rates, liquidity mining rewards, or income from lending protocols such as Aave, Compound, and Euler.This strategy creates a “circulation effect” that can double the actual deployed funds without additional external capital, essentially achieving a “self-borrowing and self-lending” fund cycle within the agreement.

6,StreamHow to increase leverage and how much?

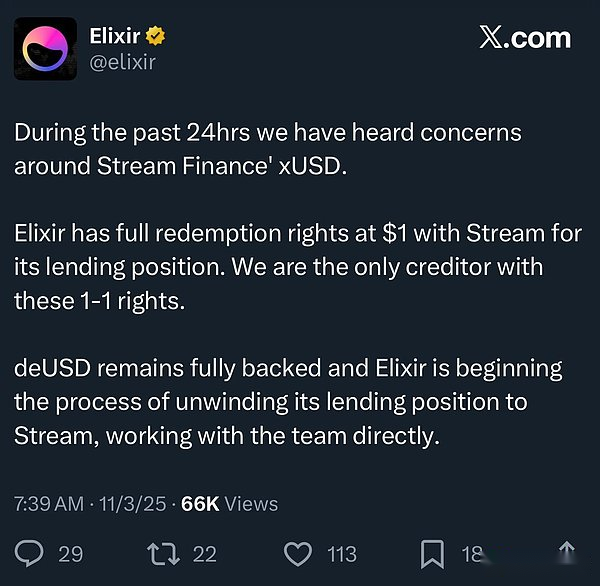

To make matters worse, Elixir claimed “priority for repayment” based on an off-chain agreement, that is, if Stream goes bankrupt, Elixir can first recover the principal.This will result in other Stream’s DeFi investors receiving less (or no access to) funds to repay.

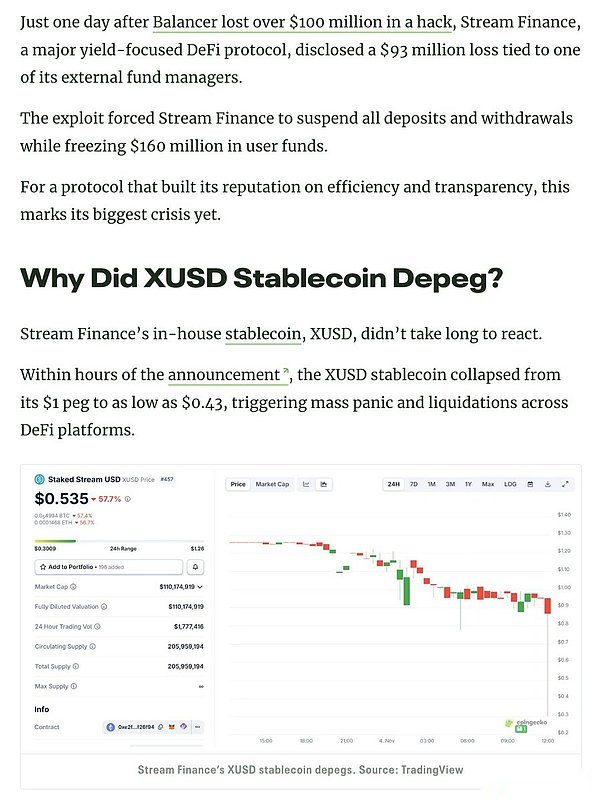

Due to the lack of transparency, recursive loop operations, and self-operated strategies, we actually have no way of knowing the exact losses of Stream users.The current price of the Stream xUSD stablecoin has dropped to $0.60 per US dollar.

Because these risks were not disclosed to DeFi users, a large number of users were extremely angry with Stream and Elixir – not only did they suffer losses, but they were also forced to ensure the continued profits of American elites with Wall Street backgrounds due to the loss of the social distribution mechanism.

This incident also affected the loan agreement and its curators:

“Everyone who thinks they are doing a secured loan on Euler is actually doing an unsecured loan through an agent” – @infiniFi Rob

In addition, because Stream did not disclose its position and profit and loss on-chain data, users began to suspect that Stream had fraudulently misappropriated user profits to the management team.Stream xUSD stakers rely on their self-reported “oracles” to obtain returns, and third parties cannot verify whether the calculations are accurate and fair.

How to deal with it?

Incidents like Stream could have been avoided, especially in emerging industries like DeFi.The “high risk, high reward” rule is certainly true, but the prerequisite for applying this rule is to understand the nature of risk – not all risks are worth taking, and some risks are unnecessary.There are currently several reputable yield farming, lending, and “stablecoin-tokenized hedge fund” type protocols that enable full transparency of risks, strategies, and positions.

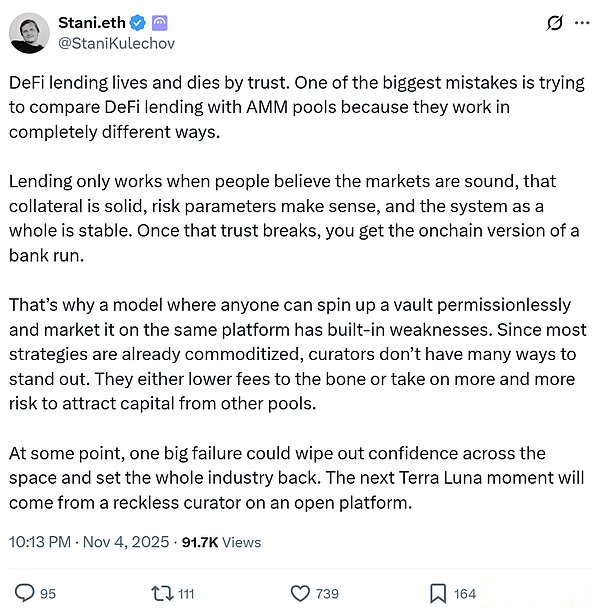

7,AaveFounderStaniDiscussDeFiCuration mechanisms and conditions for excessive risk-taking:

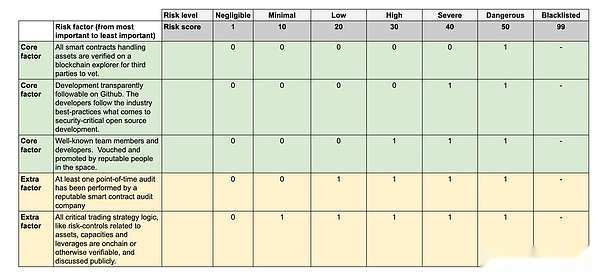

In order to more clearly distinguish between “high-quality vaults” and “low-quality vaults”, Trading Strategy has begun to publish its independently developed vault technology risk score in the DeFi vault report.

8, Regarding the treasury risk framework:

Technical risk refers to the possibility of losing investment funds in DeFi vaults due to technical execution flaws.The Vault Technology Risk Framework provides an intuitive tool for classifying DeFi vaults into high- and low-risk categories.Although this technical risk score cannot eliminate market risks such as trading errors and risk transmission, it can ensure that third parties can assess these risks.

As the quality of information available to DeFi users improves, capital allocation will be tilted towards high-quality participants, and the severity of incidents like Stream will weaken in the future.