In the global personal consumer credit chain, borrowers are often like sheep that are kept in a gentle pen—accustomed to convenience but lacking a keen sense of interest rates and terms.There is no doubt that this is a lucrative market.As unsecured consumer credit gradually migrates to the stablecoin track, its operating mechanism will undergo fundamental changes, and new “shepherds” will also have the opportunity to get a generous share of the market-changing process.

Stablecoins are unique in that they sit at the intersection of three massive markets: payments, lending and capital markets.As we are entangled in the “Red Ocean” of stablecoin payments, and while waiting for the continued popularization of stablecoin market education, can we turn our attention to the field of financial lending?Because whether it is the value capture of market spreads or the reconstruction of the entire value chain, this is perhaps the simplest and most crude market.

1. The market is huge enough

The outstanding balance of unsecured personal loans has reached $232 billion, according to 2023 data from the New York Fed, an increase of $40 billion from 2022 and an $86 billion jump from 2021, demonstrating strong demand for this type of credit.Between 2021 and 2023, loan originations to subprime and below borrowers will continue to grow, with fintech platforms becoming the core force driving this expansion.

Rising awareness about unsecured personal loans among the younger generation is significantly driving the global market expansion.Many young people have fallen into financial instability due to factors such as student loans and rising living costs, so payday products such as high-interest personal loans and short-term cash advances have become a “shortcut” for them to quickly relieve financial stress.Easy application, few requirements, fast disbursement, and unlimited uses make payday loans an attractive and convenient tool.At the same time, the penetration rate of young customer groups has increased, and the continuous influx of new lending institutions has further accelerated market expansion.

Despite a challenging macroeconomic environment, the unsecured personal loan market continues to reach record highs and shows no signs of slowing down.According to an industry report released by TransUnion in May 2025, as of the first quarter of 2025,Unsecured personal loanMarket size reaches US$253 billion, totaling 29.8 million loans.Currently, 24.6 million people in the United States hold unsecured personal loans, with the average borrower carrying $11,600 in debt.

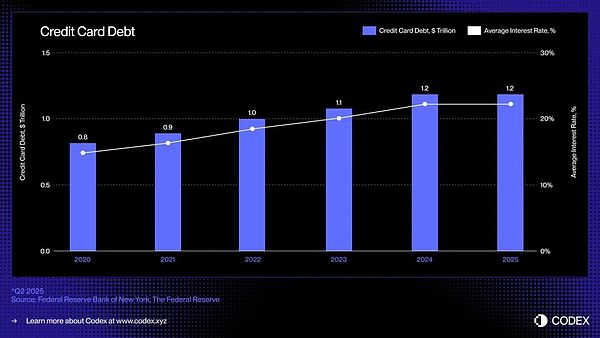

In the United States, the dominant form of unsecured lending is the credit card: a ubiquitous, liquid, and instantly available credit instrument that allows consumers to borrow money without providing collateral when making purchases.Outstanding credit card debt continues to grow and currently stands at approximately $1.21 trillion.

2. The nature of finance remains unchanged, but technology is upgrading

What is the nature of finance?It is the mismatch of value across time and space.This essence remains unchanged for thousands of years.But the service methods are changing: the “origin” of personal consumer credit is ancient credit, but what really turned it into “special money for ordinary people to buy things” was the installment payment in the early 20th century; later, credit cards combined “buy” and “borrow” into one plastic sheet, and then the mobile Internet split the credit limit into second-level micro-loans.Every technological upgrade makes loan thresholds lower, scenarios more fragmented, and risk control faster. It also drives interest rates to find a new balance between competition and supervision.

The new finance based on blockchain can greatly improve the efficiency of finance and realize an on-chain financial world that spans time, space, and asset categories.

Stablecoins and on-chain credit protocols bring a new foundation: programmable money, transparent markets and real-time financial financing.The combination of the three may finally break the old cycle and reimagine it in a digital, borderless economy.How credit is originated, funded and repaid.

The last major change in credit card lending occurred in the 1990s, when Capital One introduced risk-based pricing, a breakthrough that reshaped the consumer credit landscape.Since then, despite the emergence of new digital banks and financial technology companies, the basic structure of the credit card industry has remained almost unchanged.

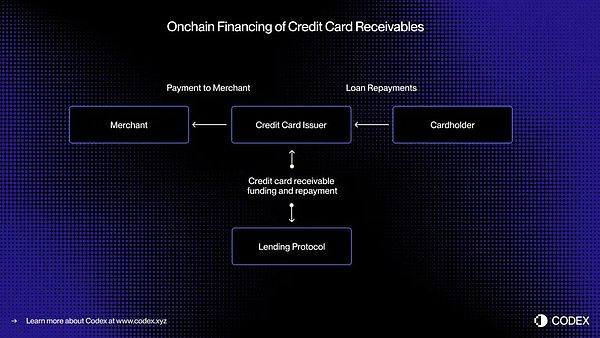

Here is a real-time example of using tokenization to finance credit card receivables:

In today’s bank card payment system, there is a time lag between transaction authorization (i.e. the transaction is approved) and settlement (i.e. the card issuer transfers funds to the merchant through the card organization).By migrating the financing process on-chain, these accounts receivable can be tokenized and funded in real time.

-

Consider a consumer making a purchase of $5,000.Transactions are authorized instantly.Prior to settlement with Visa or Mastercard, the issuer tokenizes the receivable on-chain and receives financing of 5,000 USDC from a decentralized credit pool.When settlement is complete, the card issuer transfers these funds to the merchant.

-

Subsequently, when the borrower repays the loan, the repayment funds automatically flow back to the lender on the chain through the smart contract – again in real time.

-

This approach enables real-time liquidity, transparent financing and automated repayments, reducing counterparty risk and eliminating the manual processes that are still heavily relied upon in consumer credit today.

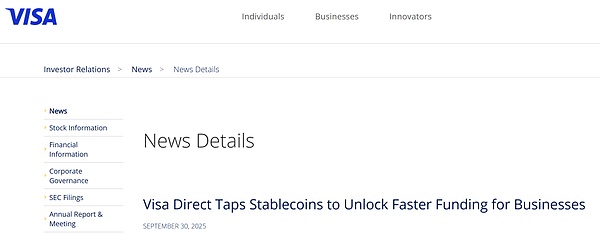

This is also the basic logic behind Visa’s recent official announcement that its Visa Direct will launch a stable currency advance business for accounts receivable.

3. From asset securitization to on-chain lending pool

For decades, consumer credit markets have relied on deposits and securitization to enable large-scale lending.Banks and card issuers package thousands of accounts receivable into asset-backed securities (ABS) and sell them to institutional investors.This structure provides deep liquidity, but also brings complexity and opacity.

Buy now, pay later (BNPL) platforms such as Affirm and Afterpay have demonstrated the evolution of how credit is assessed.themInstead of being granted a universal credit limit, each transaction is assessed individually as it occurs—Treat a $10,000 couch differently than a $200 pair of sneakers.

-

This transaction-level credit assessment generates discrete, standardized accounts receivable, each with clear borrower, maturity and risk characteristics, making it ideal forReal-time financing via on-chain lending pool.

-

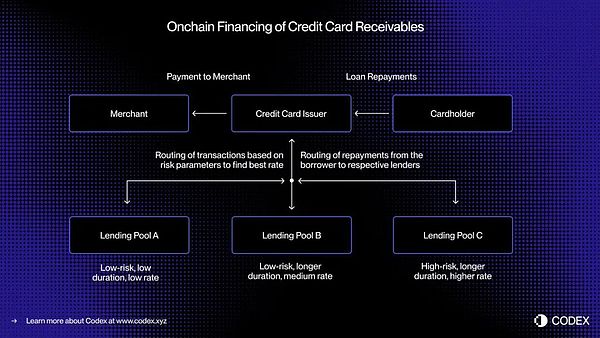

On-chain credit can extend this concept further,Allows for specialized credit pools designed around specific borrower profiles or consumer categories.For example, one pool might focus on providing small-transaction financing to prime borrowers, while another focuses on providing travel installment services to subprime consumers.

-

Over time, these pools may evolve intoHighly segmented credit market with dynamic pricing and transparent performance metrics, all participants can view it in real time.

This programmability paves the way for more efficient capital allocation, better borrowing rates, and an open, transparent, and instantly auditable global market for unsecured consumer credit.

4. Emerging on-chain credit stack

Reimagining unsecured lending for the on-chain era is not simply about “porting” credit products to the blockchain;The entire credit infrastructure needs to be rebuilt from scratch.In addition to card issuers and payment processors, the traditional lending ecosystem also relies on a series of complex intermediaries:

-

New approaches to credit scoring are needed.Traditional FICO and VantageScore may be moved to the blockchain, but decentralized identity and reputation systems may play a greater role.

-

Lenders also require a credibility assessment——On-chain rating mechanism similar to Standard & Poor’s, Moody’s or Fitch to assess credit quality and loan performance.

-

A less glamorous but crucial aspect of lending – collections – must also evolve.Debt denominated in stablecoins still requires enforcement mechanisms and recovery processes, and on-chain automation must be integrated with off-chain legal frameworks.

Overall, blockchain and stablecoins cannot change the business nature and risk coefficient of personal consumer credit. Credit rating mechanisms, risk control models, and legal structures are all indispensable. However, if we imagine the future, we can use this new on-chain credit stack to achieve global distribution of personal consumer credit, obtain global liquidity, achieve more efficient capital allocation, better borrowing rates, etc.

5. Write at the end

Stablecoin credit cards have built a bridge between legal currency and on-chain consumption; lending protocols and tokenized money market funds have redefined savings and income; introducing unsecured credit onto the chain has completed a closed loop – allowing consumers to borrow seamlessly and investors to transparently fund credit, all of which will be driven by open blockchain financial infrastructure.