source:insights4.vc, compiled: Shaw bitchain vision

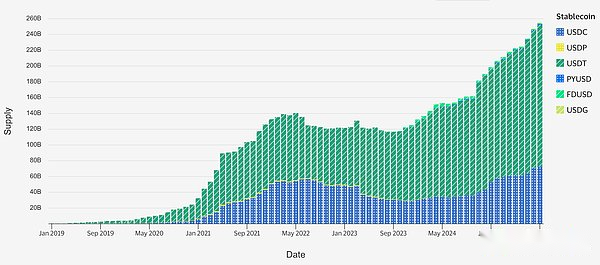

The institutional adoption rate has surged, with monthly active blockchain users increasing by 30%-50% year-on-year.Currently, the on-chain transaction volume of stablecoins in a single month (August 2025) has reached US$3 trillion, with a total market value of more than US$250 billion.Fintech payment companies are integrating stablecoins to enable fast and low-cost payments.A recent survey found that 71% of Latin American businesses have used stablecoins to make cross-border payments.With stablecoins, the average remittance fee (about 6.5% remittance through a bank is about 60%, which is already reflected in sub-Saharan Africa and other regions.PayPal’s US dollar stablecoin (PYUSD) and Visa’s ongoing USDC settlement pilot show that traditional businesses are adopting cryptocurrencies to improve financial and merchant settlement efficiency.

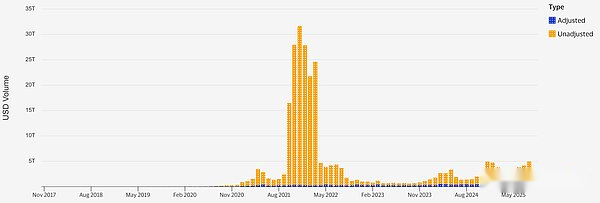

Stablecoin trading volume (adjusted and unadjusted)

Stablecoin supply, source: Stablecoin

Tokenization of physical assets accelerates: More than $26.5 billion in real-world assets (RWA) have been tokenized on-chain, up 70% since January.Nearly 90% of the assets are valued from private credit and U.S. Treasury bonds, and BlackRock’s Ethereum-based Money Market Fund (BUIDL) alone has an asset management scale of up to US$2.9 billion.

Large deals and cooperation:Traditional finance (TradFi) and cryptocurrency infrastructure are being integrated through mergers and acquisitions.Coinbase acquired crypto derivatives exchange Deribit for $2.9 billion in August 2025.Stripe acquired stablecoin platform Bridge for $1.1 billion earlier this year.Ripple’s attempt to acquire USDC issuer Circle for $5 billion is undoubtedly a warning to the stablecoin space.

Regulators establish new rules: The United States promulgated the first federal stablecoin law (GENIUS Act) in July 2025, establishing a licensing system for issuers and clearly stipulates that payment stablecoins with appropriate support do not belong to securities.Meanwhile, the EU’s Crypto Asset Market Regulation (MiCA) framework is introducing strict stablecoin reserves and regulatory rules, with Hong Kong regulators issuing licenses to stablecoin issuers starting from August 1, 2025. All of these measures provide more legal certainty for traditional participants.

Banks move from pilot to production: Banks are using blockchain technology to achieve core uses, such as 24/7 cross-border transfers, collateral markets and deposit tokens.JPMorgan’s Onyx network (deposit token system) currently settles approximately US$2 billion in internal transfers per day.In July, a consortium (Fnality), led by more than 20 banks, carried out intraday repurchase swap transactions of tokenized central bank funds and government bonds on the chain, realizing near-real-time currency-bank deal (DvP) settlement.

Large-scale tokenized funds for asset management companies: In 2025, major asset management companies launched on-chain fund shares.Franklin Templeton’s on-chain U.S. Government Money Fund (FOBXX) has grown to over $700 million in asset management (its share is traded on Stellar and connected to Polygon and Arbitrum L2).BlackRock’s USD Digital Liquidity Fund (BUIDL) has exceeded $2 billion on Ethereum, while Apollo’s new tokenized credit fund has raised $100 million in months.These measures shorten settlement time to T+0 and broaden the entry barriers for investors, such as the minimum investment through a wallet is about $100.

The technical foundation is becoming more mature: Public chain infrastructure is more suitable for enterprises.The throughput and fees of Ethereum L2 networks such as Base and Arbitrum are orders of magnitude higher than those of L1 layer, with transaction prices as low as $0.01, and the final confirmation time takes only 1-2 seconds, which attracts institutional users without sacrificing Ethereum security.Privacy and compliance add-ons (from zero-knowledge proof-scale blocks to licensed asset wrappers) are being gradually improved to meet bank-level requirements, allowing sensitive transactions and selective disclosures on the public chain.

Manage new risks: Institutions are carefully advancing control measures.Stablecoin reform aims to eliminate the risk of runs by enforcing 1:1 reserves and audits.Leading custodians hold SOC 2 reports and use advanced key management technologies such as MPC key sharding and hardware security modules (HSMs) to prevent single point of failure.Smart contracts and cross-chain bridges are the largest areas of technology risk, reviewed through formal audits and restricted exposures.Early pilot projects implemented circuit breaker mechanisms (suspension switches) and redundant mechanisms (multi-chain or fallback systems) to ensure financial stability is maintained even when blockchain components fail.

Adoption

In 2025, blockchain network activity hit a record high, indicating that it has been truly implemented rather than speculative.In the main Layer-1 and Layer-2 networks, the number of active addresses per month has ranged from millions to tens of millions.It is worth noting thatSolana tops the list with about 57 million monthly active addresses,thisThanks to high throughput decentralized finance (DeFi) and NFTapplication.pictureEthereumAlthough such a mature network is expensive,The number of monthly active addresses is still about 9.6 million; and likeBase(launched by Coinbase) Such a newer Ethereum Layer-2 network, with ultra-low fees and an off-the-shelf user base,Already have 21.5 million monthly active addresses.

The number of on-chain transactions has also shown a similar growth trend: for example, those known for paymentsTron currently has an average daily transaction volume of 8.6 million, an increase of 12% month-on-month, indicating that stablecoins and game activity are active.Even Bitcoin, which is mainly a means of store of value, has more than 10 million monthly active addresses as institutional investors drive usage through the adoption of ETFs.The key trend lies in the differentiation between retail-driven networks (high transaction volume small payments and games) and institutional-oriented networks (lower transaction volume but larger amounts).

Stablecoin application

US dollar stablecoins have become the de facto settlement medium between exchanges, remittances and DeFi.The transfer volume of on-chain stablecoins is increasing.In August 2025 alone, about US$3 trillion was transferred on-chain through stablecoins, a month-on-month increase of 92%.This transaction volume is largely driven by some large networks.Ethereum and Tron handle most stablecoin transactions, with Ethereum being used for high-value DeFi and institutional flows, while Tron dominates retail USDT transfers (Tron processed 273 million stablecoin transactions in May 2025).Ethereum currently accounts for about 65% of the total stablecoin supply (driven by USDC and DAI), while Tron accounts for about 30% (mainly USDT issuance).The use of stablecoins has differentiated.On exchanges, they serve as quoted currencies contribute to approximately 80% of cryptocurrency trading volume.And on-chain, they support instant cross-border payments and earning farming.One development worth noting is the growth of non-dollar stablecoins for foreign exchange diversification, such as Singapore’s XSGD and Euro stablecoins, although USD-backed stablecoins still account for about 95% of the market share.Stablecoins are now an important infrastructure.Circle’s USDC and Tether’s USDT settle trillions of dollars each year, and more and more businesses hold it as digital cash.

Growth of tokenized assets and RWA

In addition to payments, 2025 is a breakthrough year for tokenized real-world assets (RWA).Against the backdrop of high interest rates, tokenized U.S. Treasury products and money market funds have grown particularly rapidly.As of April 2025, the total asset management scale (AUM) of tokenized treasury bonds and related funds on the public chain exceeded US$5.7 billion and continued to rise.By mid-2025, an estimated $26.5 billion of RWA will be launched, covering government bonds, private credit, real estate and fund shares.Several on-chain mutual funds have been launched.Franklin Templeton’s on-chain U.S. Government Money Fund is a “40 Act” fund investing in short-term Treasury bonds. As of August 31, 2025, its traditional AUM was $744 million and uses Stellar and Polygon as its share ledger.BlackRock’s USD Digital Liquidity FundLaunched at the end of 2024, (BUIDL) raised more than $2 billion in a year by providing tokenized shares of money market funds to crypto platforms.Even alternative assets are added.Private equity giants such as KKR and Apollo have tokenized some credit funds, enabling qualified investors to enter the market with lower minimum investment amount and faster liquidity.It is worth noting that by June 2025, the on-chain asset management scale of Apollo’s tokenized multi-credit fund (the stock code ACRED issued through Securitize) has reached US$106 million.These examples show that tokenization is no longer just empty talk, but is producing investable products with substantial assets, usually using public chains such as Ethereum and Polygon, while maintaining traditional regulation through a fund structure regulated by the U.S. Securities and Exchange Commission (SEC).

Capital markets and equity activities

Traditional capital markets also interact with blockchain through IPOs and mergers and acquisitions.In 2023, the first IPO of a cryptocurrency native company was ushered in, while in 2025, there were many established companies acquiring blockchain infrastructure.In the first half of 2025, there were more than 200 cryptocurrency-related mergers and acquisitions, with a total amount of approximately US$20 billion, while in 2024 it was only US$2.8 billion.For example, in August 2025, Coinbase (NASDAQ: COIN) acquired Deribit, the world’s largest cryptocurrency options exchange for US$2.9 billion, and Coinbase instantly became the world’s largest crypto derivatives trader.In the payments space, Stripe acquired stablecoin payment startup Bridge for $1.1 billion to integrate the interoperability of cryptocurrencies with fiat currencies into its merchant network.Traditional banks are also actively involved.

Standard Chartered has increased its stake in cryptocurrency custody platform Zodia, and Nasdaq has also made strategic acquisitions of a digital asset custody agency, although these transactions are small in scale and usually no transaction details are disclosed.Meanwhile, after Coinbase, no major cryptocurrency companies have made IPOs.Instead, some companies, such as Circle, attempt to acquire companies (SPACs) or go public directly, but are shelved due to market conditions.Overall, this trend has led to industry consolidation, with large and regulated players such as exchanges, fintech companies and banks expanding through the acquisition of capabilities such as derivatives platforms, custodians and tokenization technologies rather than building from scratch.This M&A trend is expected to continue, backed by a clearer regulatory environment and attractive valuations in cryptocurrencies.

Regulatory milestones

Since June 2025, several regulatory milestones have changed the pattern of blockchain use by banks, asset managers and fintech companies.In the United States, Congress passed the “Guiding and Establishing the U.S. Stablecoin National Innovation Act” (GENIUS Act) on July 17, 2025, the first federal law in the United States specifically targets stablecoins.The bill, signed by the President on July 18, 2025, defines payment stablecoins and requires the issuer to obtain permission through the U.S. Currency Complaints (OCC) or state government agencies, while meeting prudent standards such as 100% reserve support and monthly disclosure.The bill also excludes such stablecoins from the definition of securities, leaving them out of the SEC’s jurisdiction and provides clear guidance for banks considering issuing their own tokens.

The bill will come into effect at the latest in January 2027, 18 months after its enactment, or if regulators implement the relevant rules earlier, it will take effect in advance so that companies have a transition period to adjust compliance matters.In Europe, the Crypto Asset Market (MiCA) regulations have come into full effect in 2025, with rules regarding stablecoins (called asset reference tokens and electronic currency tokens) now in effect.MiCA requires that, among other things, stablecoins pegged to the euro maintain par value redemption without fees and conduct business within the EU, prompting some non-EU stablecoin issuers to withdraw or obtain permission.Additionally, MiCA requires crypto service providers, including exchanges and custodians, to obtain licenses by early 2025, which has forced banks and asset managers to work with regulated entities or obtain licenses on their own.

In Asia, the Hong Kong Monetary Authority issued a stablecoin regulatory framework in July 2025 and released an explanatory note on requirements such as audit and floating management at the end of July.Hong Kong aims to accept applications from stablecoin issuers and wallet providers, positioning itself as a regional hub under regulated protection, which is very different from the previous cautious stance.Singapore has introduced stablecoin issuance guidelines as early as 2022, such as the Monetary Authority of Singapore (MAS) reserve requirements, so by 2025, major financial centers will converge to similar standards.These regulatory measures directly affect the adoption of TradFi.Under US and EU banking laws, banks now have a clearer license to issue deposit tokens.Asset management companies can launch tokenized funds because they know that the distribution platform will be licensed.Fintech companies have clearer expectations for KYC and AML for crypto services.The overall impact is to reduce regulatory uncertainty.Executives can no longer use the excuse of waiting for regulators, but instead, the rules have been introduced and the priority is to comply with and enforce them.

bank

Priority use cases

In 2025, banks will focus on the application of blockchain technology in capital flow and settlement use cases, which are particularly prominent when traditional infrastructure is slow or fragmented..Among them, tokenized deposits are a digital embodiment of bank deposits and can be transferred on-chain immediately.This makes it possible to transfer money internally and across banks around the clock, which is crucial for corporate finance executives and internal liquidity management.JPMorgan Chase has been a pioneer in this field: its JPM Coin system (some products have now been renamed Partior/Kinexys) allows institutional customers to make global dollar transfers on licensed blockchains.As of mid-2025, JPMorgan’s network has transferred about $2 billion in on-chain deposits between its branches and customers every day, reducing cross-border settlement time from hours to minutes.

JPMorgan Chase is currently preparing to pilot JPMD, a deposit token based on public chains (probably Ethereum or L2 networks) designed to expand the service beyond its private network.Other major use cases include instant cross-border payments, such as the use of stablecoins or CBDC-like tokens to avoid delays in agency banking; collateral liquidity, tokenizing collateral for intraday or instant pledge and release; and intraday repurchase markets.In July 2025, several banks, including BNP Paribas and Lloyds, demonstrated on-chain intraday repurchase settlement: one bank’s treasury repurchases bonds to another bank for hours, using central bank currency tokens for payment, all operations are conducted on a distributed ledger technology (DLT) network and can be closed immediately.This indicates that in the future banks can optimize liquidity hourly (rather than just overnight) and potentially save capital and reduce transaction failures.Another use case that has attracted attention is forex settlement: projects such as Baton Systems and HSBC’s FX Everywhere have already implemented PvP settlement across currency transactions using shared ledgers without Herstatt risk.

Pilot projects and systems that are actually running

At present, some blockchain networks led by banks have been launched or are in the later pilot stage.In addition to JPMorgan’s Onyx, another prominent example is Fnality International, a coalition of about 15 large banks, including UBS, Barclays, Santander, Mitsubishi UFF Financial Group, etc., aiming to build a series of licensed payment systems backed by central bank deposits.In December 2023, Fnality’s UK network settled in pounds, obtained approval from the Bank of England and processed its first real-time transaction with Lloyds and Santander using the Bank of England’s integrated account.By July 2025, BNP Paribas joined Fnality’s UK system and made on-chain interest rate swap payments with Lloyds Bank, which was actually a payment for the swap cash flow through tokenized pounds. The entire process was completed in a few seconds and the full amount of the cash and bank deal was achieved, because the exchange of collateral was transferred simultaneously with the payment.It is a milestone to participate in the DLT payment utility at such a large scale, as it shows that regulated blockchain networks can fulfill true wholesale payment obligations.Another example is Partior, a cross-border interbank network jointly founded by DBS Bank, JPMorgan Chase and Temasek, which has provided real-time transfers of Singapore dollar, US dollar and Japanese yen on licensed chains in Asia.In the retail space, Signature Bank’s Signet platform (before Signature Bank’s closure) and Silvergate’s SEN platform showed Bank of America the practicality of tokenized deposit platforms in all-weather enterprise payments, and due to the disappearance of these platforms, other banks are now considering building a similar network under U.S. federal regulation.

Public chain and license chain, decision-making chart

A key strategic decision for banks is whether to use public or licensed, private or consortium chains in these use cases.To date, many banks tend to use license chains or quasi-private L2 networks because the participants of these networks are known and the rules can be enforced.For example, Fnality (members only, regulated by the central bank) and JPM Coin (operated by the bank).The licensed chain system provides guarantees in terms of privacy and control, but sacrifices the wide interoperability of the public chain.However, this trend is slowly changing.Banks are trying to use public chains for certain assets, especially when exposure to various counterparties, such as issuing tokenized bonds or deposits on Ethereum that any qualified investor can hold.To coordinate public chains with compliance, banks are adopting additional solutions, such as using license chain wrappers or smart contracts, transferring tokens to whitelisted addresses to secure KYC, or leveraging an L2 network that allows banks to run a set of license validators while anchoring to public chain L1.Privacy is another issue worth paying attention to, because blockchain transactions are transparent by default.Banks are evaluating privacy stacks such as zero-knowledge proof and viewing keys.Zero-knowledge proofs can verify that transactions meet certain conditions, such as anti-money laundering inspections or debt contracts, without revealing underlying details to the outside world.

Integrating blockchain with the core banking system is not easy.Leading institutions have established internal digital asset departments to connect the DLT platform with traditional ledgers such as general ledgers, payment centers, and custody systems.The key integration lies in the core banking business system.When a customer transfers $100 from a bank account to tokens, the core ledger must show that the deposit is reduced by $100, while the blockchain ledger shows that the $100 token was issued.This two-way link must be tight to avoid any mismatch, usually achieved through real-time updated APIs or middleware.Many banks initially ran pilot projects in parallel in shadow mode, using existing systems to measure key performance indicators (KPIs), such as settlement delays, settlement speeds of cross-border payments on blockchain with SWIFT (usually around 10 seconds, while recent pilot projects take several hours), failure rates (where the blockchain’s atomic settlement commitment failure rate is close to zero, one of the measures is the reduction of Forex settlement failure or mismatch transactions), reconciliation time (shared ledgers eliminate hours of reconciliation efforts, and some projects report 50% to 80% reduction in back-end reconciliation), and liquidity or capital efficiency.

The latter is the key.For example, intraday repurchases on distributed ledger technology (DLT) allow banks to reuse collateral multiple times a day, potentially reducing the required peak liquidity.Early trials of Broadridge distributed ledger technology showed that banks could free up hours of additional liquidity usage, reducing the required buffer capital.Banks will closely monitor the impact of these pilot projects on indicators such as intraday interest costs, whether using tokenized collateral or reducing overdraft fees or intraday borrowing demand, as well as counterparty exposure, as shorter settlement cycles mean lower exposure.All in all, banks’ adoption of blockchain is shifting from experimentation to pragmatic deployment, which obviously saves time, money or capital, especially in terms of payment and settlement processes.

Asset Management Company

Tokenized funds and securities, asset management scale (AUM) and products: Traditional asset management companies now mainly put tangible assets on the chain through tokenized funds and RWA tokens.By September 2025, the cumulative AUM of tokenized funds had exceeded the $1 billion mark and was still growing rapidly.

It is roughly divided into two categories.The first category is tokenized money market and bond funds, providing access channels for low-risk and return tools on the chain.The second category is tokenized alternative assets, such as private equity, credit and real estate, provides liquidity and access to traditional illiquid assets.In the first category, several large companies have launched tokenized money market funds.

An example is Franklin Templeton’s on-chain U.S. government money fund, which invests in U.S. Treasury bonds, currently has assets under management of more than $700 million.Its innovation is the use of the public chain Stellar as the official share register, making it the first fund to be registered in the SEC and recorded on the chain.The fund’s shares (BENJI tokens) can now be traded on Polygon and Arbitrum, thus expanding the distribution scope.BlackRock launched the private liquidity fund BUIDL at the end of 2024, and its tokenized shares were launched on the Ethereum main network.It is reported that by mid-2025, BUIDL will become the world’s largest tokenized RWA product, with an asset management scale of nearly US$3 billion, distributed to qualified investors through Coinbase and other digital asset platforms.

Competitors like WisdomTree have launched tokenized Treasury bond funds, and even tokenized cash, such as WisdomTree’s Prime Fund.By mid-2025, WisdomTree’s various tokenized funds will have an asset size of approximately US$315 million.In terms of alternative investments, Hamilton Lane and KKR tokenize some private equity funds in 2022 and 2023, respectively, and these efforts are still intensifying.For example, Hamilton Lane reportedly launched a tokenized sub-fund for private equity investment funds, attracting hundreds of new investors and receiving tens of millions of dollars in subscriptions on the chain.

Apollo’s tokenized credit fund ACRED was launched on Ethereum through Provenance or Centrifuge platforms in early 2025, and by June, its on-chain investments quickly exceeded $100 million, including $50 million from crypto-income funds.Importantly, these tokenized funds are not independent crypto funds.They are the same pools of funds that traditional investors can purchase through conventional channels, but are now available in the form of digital tokens.Distribution strategies vary.Franklin and WisdomTree’s products are multi-chain to meet investors on different networks.BlackRock’s BUIDL and Apollo’s credit funds chose single-chain Ethereum and had a single transfer agent (usually a fintech partner like Security or Tokensoft) to simplify control.

We’ve seen it tooTokenization index and ETF will be released soon.BlackRock is exploring tokenizing a wide range of stock ETFs, such as the S&P 500 tracking fund, but with regulatory approval.If approved, this will free up trillions of dollars in stock assets and enable all-weather on-chain transactions.The current tokenized fund asset management scale may be smaller than traditional finance (TradFi), but the growth rate is very fast and the development direction has been determined.Even the conservative BlackRock has publicly stated that it will eventually tokenize all assets.

Technical building modules

Preferred Network (2025)

Organizations are inclined to select a handful of blockchain networks that best meet their throughput, finality, cost and ecosystem maturity needs.In the public chain field, Ethereum still dominates with its large developer base and liquidity and is the first choice for asset tokenization that requires extensive interoperability (such as funds and securities that may interact with DeFi).However, the limitations of Ethereum L1 (about 10-15 TPS, fee fluctuation) mean that most institutional activities occur either on L2 networks (such as the zero-knowledge proof networks of Arbitrum, Optimism, Base, and Polygon) or on other L1 networks optimized for enterprises.

For example, many tokenized bond pilot projects in Europe use Ethereum sidechains or licensed Ethereum instances to protect privacy, while funds like Franklin initially chose Stellar for its low cost and built-in compliance capabilities.Polygon is also popular in the tokenized assets due to its high adoption rate, low fees and compatibility with Ethereum virtual machines (EVMs).According to industry data, in 2024, before the emergence of Base adds more options to tokenized assets, Polygon, Ethereum and Arbitrum are the top three networks by RWA token value.We are also seeing more and more organizations using the Cosmos SDK chain or Polkadot parachain for more customized services.

Some European digital bond markets use licensed Cosmos chains and operate by selected validators, such as Euroclear’s DLT bond platform, which runs on custom ledgers.In terms of throughput and finality, institutions seek networks that can complete transactions and handle burst activities in 5 seconds.

Solana and Avalanche are often mentioned.Solana offers high TPS and about 400 milliseconds of block time, which is attractive for trading applications, and some TradFi trading companies are using Solana for on-chain options or forex experiments.Avalanche’s subnet allows custom networks to remain settled to Avalanche’s mainnet, and some banks have tried the regulatory sandbox network for KYC on-chain to test asset issuance.

Decentralization and control

Organizations care about decentralization from a pragmatic perspective.They want to ensure that no party can unilaterally change or terminate the ledger except itself in the private chain.Ethereum and Bitcoin are seen as highly decentralized, with a huge set of validators and nodes, thus providing censorship resistance.By contrast, the license chain may have only a few nodes, which makes co-conspiracy or failure more likely to occur.To alleviate this, a coalition chain like Fnality recruits a large number of member nodes and seeks legal recognition, such as obtaining final settlement protection from the central bank to enhance trust.In terms of performance purely, there has always been controversy over which is better and worse between high-performance Layer1 and Ethereum Layer2.Many enterprise developers tend to stick to the Ethereum ecosystem and scale through Layer2 or sidechains for easier interoperability rather than shifting to a separate technology architecture.This is evidenced by the rise of institutional-oriented Layer 2 solutions, such as Polygon zkEVM Permissioned or Consensys Linea, where rollups can run with enhanced privacy.

Privacy and Scale Blocks

Given strict regulatory requirements, adding a privacy layer to blockchain transactions is critical to many TradFi use cases.There are some methods available:Zero-knowledge proof is becoming the tool of choice.For example, before the transformation in 2023, AZTEC Network was used for pilot projects, allowing confidential asset transfers on Ethereum using zero-knowledge encryption, which not only hides identity, but also hides amounts.Organizations also use zero-knowledge proof to ensure compliance.Transactions can be conducted on the public chain while providing proof that the transaction takes place between two participants who have completed KYC without breaching the restrictions without revealing the identity of the participant.The Guardian project launched in Singapore from 2022 to 2023 proves this by providing investors with zero-knowledge-based verification credentials.Before the wallet performs a DeFi transaction, the smart contract checks whether the wallet has valid KYC credentials issued by a trusted institution without revealing the wallet’s identity on the chain.

Viewing a key or selective disclosure is another way to.Some enterprise-oriented chains, such as R3 Corda (which is a kind of DLT instead of a blockchain), use peer-to-peer encryption, so only the parties involved can see the transaction details.Some newer agreements allow the provision of keys to third parties, such as regulators, to check transactions if needed.In IBM’s World Wire payment network built on Stellar, participating banks can view transaction details for anti-money laundering checks using encrypted memos that only regulators can decrypt.On Ethereum, ERC-1404 and other token standards allow restrictions and potential off-chain data exchange to accompany transfers, such as sending identity information while transferring.There is also the development of a privacy pool using zero-knowledge circuitry, similar to Tornado Cash but compliant, where funds can be pooled and mixed to protect privacy, but users in the pool are KYC-verified and operators can unanonymize when needed.Some EU banks tested this concept in 2025 to see if decryption can be mastered by intermediaries to meet both GDPR privacy and AML traceability.

Compliance token expansion is common.Security tokens usually contain the logic of checking whitelists or prohibiting transfers that exceed a certain limit.An example is the Tokeny platform used in Europe, where each token on this platform contains a smart contract that references a registered contract from a qualified investor.If Bob tries to send tokens to Alice and Alice’s wallet is not in the registration center as an approved investor, the transfer fails.This ensures compliance with the on-chain securities laws.Similarly, Fireblocks introduces an engine that can enforce information on transfer rules, where metadata about promoters and beneficiaries can be attached to institutional stablecoin transfers and can only be read by the receiving agency, addressing the issue of the Financial Action Task Force (FATF) transfer rules on the chain.

Hosted infrastructure

For any institution, it is crucial to choose a digital asset custody solution.The threshold is very high.The custodian provider must provide bank-grade security and demonstrate strong internal control.Usually, institutional custody involves many aspects such as technology, laws and regulations, and insurance.In terms of technology, leading hosts use hardware security modules (HSMs) or multi-party computing (MPCs) to protect private keys.The HSM is a tamper-proof physical device in which the key can be stored and signed without leaving the device.MPC allows multiple parties to hold key fragments, such as hosting agencies, clients and recovery services, each party holding one fragment.The transaction signature is generated by multiple parties, so neither party can have a complete private key.This reduces the risk of single point failure, and companies such as Fireblocks and Zodia also believe this is the reason why banks use HSM with peace of mind.

Key sharding and geo-redundancy are standard.Institutional custodians typically store key materials in multiple data centers or even multiple countries.For example, Coinbase Custody might store key shards in New York, Dublin, and Singapore so that the keys are not lost in a catastrophic event in one place.They also have disaster recovery procedures in place.If the server that stores shards is corrupted, you can use the protocol to regenerate the key from the backup saved in the secure vault, which usually requires approval from multiple executives.In terms of internal control, many custodians have obtained SOC 1 Type 2 and SOC 2 Type 2 certifications, which are independent audits of financial reporting controls and security controls.These proofs, along with ISO 27001 certification, indicate that the custodian’s processes, such as employee reviews and withdrawal approvals, meet industry standards.

In addition, regulatory franchise is also crucial.Some of the top cryptocurrency custodians have obtained bank or trust charter.Anchorage holds a charter of National Trust Bank.Coinbase Custody is a New York State Trust Company.These charter provisions capital requirements and regulation.Client assets are legally isolated and cannot be used in bankruptcy, which is similar to how securities custodians operate.

Insurance is crucial.Most institutional custodians purchase criminal insurance, covering certain limits of digital asset theft, such as a $100 million policy.Gemini, for example, stressed that it purchased more than $200 million in cold storage wallet insurance through an exclusive insurance company.Insurance does not cover all situations, such as hacking in some countries, but for many risk committees, insurance is essential.

Operational considerations include the ability to provide 24/7 support, withdrawal SLA (Service Level Agreement), such as ensuring that assets can be transferred out within about one hour after a hot wallet request, and about 24 hours after a cold wallet request, as well as providing reports and APIs to integrate with portfolio systems.A big difference now is the reserve proof or on-chain proof.Some custodians, such as BitGo, provide customers with tools to independently verify whether their assets are held one-to-one by viewing on-chain addresses or auditor proofs.Institutions asked their custodians to remain transparent after the FTX crash in 2022 to ensure they do not re-collateralize or abuse their assets.Custodians also adopt accounting controls, such as daily checking of on-chain balances with customer ledgers, and physical security measures similar to vaults to protect any manual key fragments, some custodians are still using deep cold storage, engraving the keys on steel and storing them in bank vaults.

all in all,The standard list for hosting includes regulatory compliance, technical security, auditability, insurance coverage, operational resilience, and scalability.Many organizations choose multi-source hosting, using two to three hosting agencies to avoid vendor lock-in and provide backups.Currently, large companies like Bank of New York Mellon are entering the digital asset custody space, and Nasdaq is also planning to enter the digital asset custody space (although currently suspended), indicating that over time, digital asset custody will be integrated into the same companies as stocks and bonds and follow the same strict standards.

Risk and constraints

Despite some progress, adopting blockchain as the core infrastructure will bring new risks in addition to traditional risks.For executives planning to deploy, it is crucial to have a clear understanding of these risks and develop mitigation strategies.

Market risk

The cryptocurrency market is known for its volatility, but in traditional finance, market risks come from the volatility of the assets under the target when holding crypto assets, and the decoupling of stablecoins.For example, businesses that use USDC for fund management need to believe that USDC will maintain its $1 value and will not experience a brief run like in March 2023.Mitigation measures include insisting on holding fully reserved and regulated stablecoins, such as new legislation such as the GENIUS Act, requires stablecoin issuers to hold 100% cash or U.S. Treasury bonds, which should reduce risks and set a cap on the holding of stablecoins relative to liquid cash.

Another market risk is liquidity risk.If an institution tokenize assets (such as loans) and relies on on-chain sales, they may face liquidity tightening once the blockchain market freezes or splits.DeFi liquidity has dried up in past economic downturns.If secondary market transactions are weak, asset management companies may not be able to redeem tokenized bonds quickly.To mitigate this, companies retain alternate liquidity tools, such as providing bank credit lines when on-chain sales fail, and often limiting tokenized issuances to structures with less liquidity dependence, such as closed-end funds that investors promise to hold a certain period of time.

Operational risks

These risks include smart contract vulnerabilities, process failures, and human errors.Vulnerabilities in smart contracts can cause assets to be locked or exploited.Flawed custodial smart contracts may be stolen.To control this situation, any critical smart contract must be audited and formally verified, usually requiring multiple audit companies to participate and conduct testnet simulation runs.Some companies will also set up off-chain security networks.For example, tokenized funds may contain legal provisions that in the event of a contract failure, the transfer agent can be restored to a manual process and issue new tokens or traditional stocks to investors.Failed key management is another risk, such as loss or stolen private keys.

Solutions such as MPC and multi-signature with approval workflow reduce single-person operation risk.Many institutions implement hierarchical key systems.Large amount transfers require the enforcement of multiple signature approvals from multiple senior executives.Daily small transfers can use restricted automatic signatures.In addition, there is a risk of reconciliation errors.While blockchain provides a single source of fact, if not careful, integrating it with legacy systems can lead to mismatch in data.The company solves this problem by building a real-time reconciliation dashboard and using an oracle to input blockchain data into the internal system.The operational risk worth noting is blockchain downtime or fork.Some networks (such as Solana) have experienced interruptions.If you rely on the chain for payment, you need contingency measures such as using an auxiliary chain or falling back to SWIFT when the interrupt duration exceeds a set threshold.

Similarly, chain restructuring or 51% attacks can theoretically lead to transaction reversals.This is currently extremely unlikely for mainstream blockchains like Ethereum, and there are finality checkpoints, but for security reasons, critical applications usually wait for a certain amount of confirmation, or use Layer-2 with proof of validity to ensure finality through encryption.Private chains avoid restructuring risks through licensed nodes and instant finality protocols, but only if these nodes must be trusted.

Regulatory and legal risks

Even with new laws, regulatory risks still exist.The law may change.The new government may tighten regulations on autonomous custody or DeFi.The cross-jurisdictional problem persists.Practices permitted in Singapore may violate EU rules.Institutions respond through geofencing, ensuring that their blockchain activity is only available to jurisdictions where they feel reassured, and confirming by obtaining legal advice on tokenization tools, for example, tokenized notes remain the same securities under law.A huge legal risk in smart contracts is the uncertainty of responsibility.Who will be held responsible if the DeFi protocol fails and causes losses to the asset management company’s funds.Many management companies build on-chain businesses through regulated subsidiaries, or invest only a small portion of their funds in DeFi to limit liability, and they will clearly disclose these risks to their clients.The compliance department is also concerned about AML anti-money laundering and KYC risks.Interactions with public blockchains may inadvertently involve illegal funds.To solve this problem, the company uses blockchain analytics to filter addresses and transactions in real time.For example, before accepting stablecoins from customers’ wallets, they are scanned to check whether they are related to sanctions or illegal activities.This is similar to using new tools to screen wire transfers.

Technical risks

In addition to smart contract risks, scalability and performance limitations are also crucial.If an institution suddenly conducts millions of daily transactions on Ethereum, the cost of handling fees may soar and throughput may be blocked.Scalability risks can be reduced by choosing the right network (such as Layer2, high-speed Layer or shard architecture) and using batch processing as much as possible to aggregate transactions, asynchronous processing in small transactions that do not require immediate finality.Interoperability and cross-chain bridge risk are also important because institutions often need to transfer assets across chains, such as putting tokenized assets on one chain and liquidity on another.Cross-chain bridges are well-known points of failure, losing billions of dollars in past hacking attacks.Therefore, institutions will minimize the use of third-party cross-chain bridges.Some organizations will choose a destruction casting program operated by trusted parties.Circle’s cross-chain transfer protocol reduces custody risks by destroying on the source chain and minting on the target chain to avoid holding assets in the cross-chain bridge.When third-party cross-chain bridges are needed, institutions prefer cross-chain bridges with strong security, such as multi-signature mechanisms that support multi-signature, insurance as much as possible, and auditing.Some agencies also require cross-chain bridge providers to conduct risk assessments, and there are frameworks that can rate the security of cross-chain bridges.

in conclusion

Blockchain has evolved from the proof of concept stage to the actual production stage of capital flows, collateral and fund allocation.Regulatory transparency in the United States, the EU and Hong Kong reduces policy risks, while the increase in stablecoin trading volume and tokenized fund asset management scales indicate real demand.Short-term winners will be banks and asset management companies that combine public chain coverage with licensing control, measurable KPIs and strict custody.Current execution focuses on supplier selection, privacy design and risk control rather than participation.