Author: Les Barclays, compiled by: Shaw bitchain vision

In this post, I will dissect one of the most important financial developments that I think are happening right now…new stablecoin legislation and its possible role in helping the United States manage national debt, maintain dollar dominance, and put pressure on global markets.In my opinion, this is not only about cryptocurrency regulation, but also about bond markets, yield curves, macroeconomic strategies and the wider geopolitical game behind the scenes.

If stablecoins are included in the US fiscal and monetary policy system, their impact will not only be of great significance to the cryptocurrency field, but will have a huge impact on global trade, manufacturing, debt issuance and monetary policy.This could allow the United States to rebuild domestically at a lower cost while increasing financial pressure on competitors and re-attracting funds back to the U.S. system.

What is the GENIUS Act (why was it issued at this time)

Stablecoins can be considered as digital dollars that always value exactly $1.Currently, there are no clear rules on who can issue stablecoins and how they should function, which raises concerns about their security.

GENIUS Act (Senate Version): This bill establishes a regulatory framework for payment of stablecoins (digital assets that issuers must redeem at fixed currency value).Under the bill, only licensed issuers can issue payment stablecoins.Think of it as a special license required to print digital currency.

Key Differences

Who will be responsible: The Senate version concentrates supervision on the Treasury Department, while the House allocates power to the Federal Reserve, the Office of the Currency Regulatory Commission and other agencies.

Rulemaking: Under the GENIUS Act of the Senate, only the Office of the Supervisor of Currency (OCC) has the right to issue these rules.The House of Representatives’ STABLE Act will impose more requirements and will be collaborated by multiple agencies.

Both goals are:

-

Safety first: Only approved companies can issue stablecoins, which is similar to only licensed banks that can keep your funds.

-

Consumer Protection: The legislation will limit the issuance of payment stablecoins in the United States to the “approved payment stablecoin issuers”.

-

Market clarity: Designed to regulate the stablecoin market of approximately $238 billion and create a clearer framework for issuing digital currencies for banks, companies and other entities.

Current status: The GENIUS Act was passed with 308 votes in favor and 122 votes against.The U.S. House of Representatives passed the “Guiding and Establishing a U.S. Stablecoin National Innovation Act” (hereinafter referred to as the “GENIUS Act”) on July 17, 2025, and submitted the landmark bill to President Trump for signature.Therefore, the Senate version (GENIUS Act) eventually won and officially became the law, becoming the first cryptocurrency bill to be approved by both houses of Congress.

Essentially, both bills hope to create “traffic rules” for the digital dollar, but there are differences on which government agencies are to act as “traffic police.”

The House of Representatives’ STABLE Act and the Senate’s GENIUS Act are two tit-for-tat bills, but have a common goal: to include stablecoin issuers in the scope of regulation and clarify how much capital, liquidity and risk management are needed to be sufficient.They also aim to clarify which federal or state agencies are used to serve as referees.But there is another less compelling potential plot: How will the widespread acceptance of stablecoins by traditional global institutions affect the US Treasury market with a scale of $28 trillion?

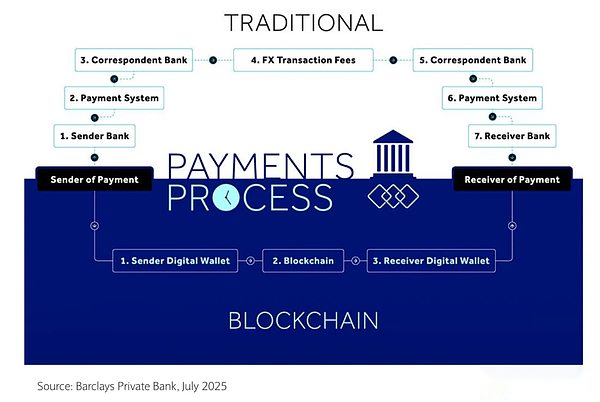

How stablecoins become hidden demand for Treasury bonds

Here’s the thing: Treasury bonds are the backbone of stablecoin reserves, because in terms of security and liquidity, few other assets can match it.If you offer a digital dollar, you need to support it with as close to risk-free assets as possible.It sounds a lot like hundreds of money market mutual funds issued by giants such as BlackRock, Fidelity and Pioneer, holding over $6 trillion in assets, most of which are Treasury2.But unlike money market funds issued by Fidelity, such as Fidelity, which may offer an annual rate of return of 4%, most stablecoin issuers have so far refused to provide any gain or income to their holders.This is why Tether, the largest stablecoin issuer, has extremely high profit margins and reported over $1 billion in operating profit in the first quarter of 2025.It does set a lot of standards for compliance with reserves, audits, disclosures, and anti-money laundering (AML) procedures, as it wants to address many concerns about illegal activities.It also involves restrictions on the fact that stablecoins are not allowed to be marketed as fiat currencies, while prohibiting payment of income or interest to individuals holding stablecoins, as this would greatly weaken the banking industry.

One thing I’ve been paying attention to for a while (but unfortunately I haven’t told anyone yet), is the relationship between stablecoins, US Treasury bonds and the Treasury Department.And why I think the government will push stablecoins first over other things.

In the chart below, there is one thing I want to emphasize:

I emphasize this now because stablecoins are probably one of the biggest buyers of U.S. Treasury bonds, which reduces bond yields.In short, with stablecoins, you can get the yield curve back to normal, and that seems to me exactly what the Trump administration wants to implement, as both Trump and Becent (who I’ll talk about later) are concerned about the country’s debt and the amount of refinancing needed by the end of the year.

Treasury bond angle

I think this is an interesting way to reduce the interest payments for debts mentioned above, and the reason it is extremely fascinating is that it will allow the United States to refinance Treasury bonds at lower yields, which will ultimately make financing Treasury bonds much easier.

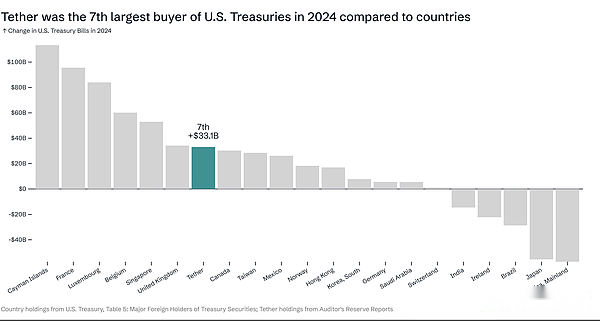

Now let’s talk about the situation of stablecoins compared to other countries.In 2024, Tether is the seventh largest buyer of U.S. Treasury bonds, as is the case with other countries that buy U.S. Treasury bonds.Imagine how many Treasuries Tether (or Circle or other institutions) can buy under this framework.There are some concerns surrounding stablecoins and central bank digital currencies, and other bills or bills are being drafted and passed, involving the United States’ non-support of central bank digital currencies.You can speculate that Tether or Circle may be disguised as central bank digital currencies, but this is another topic altogether, so I won’t go into it in depth.What I want to focus on is the impact of stablecoins on national debt.

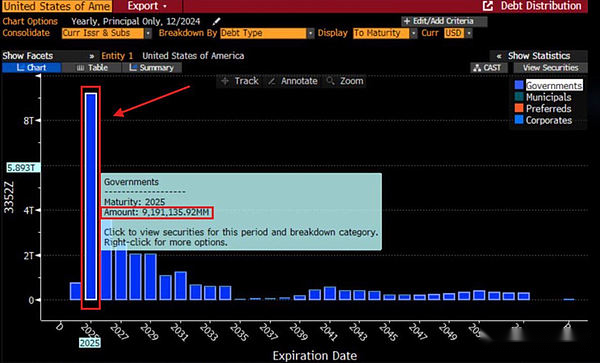

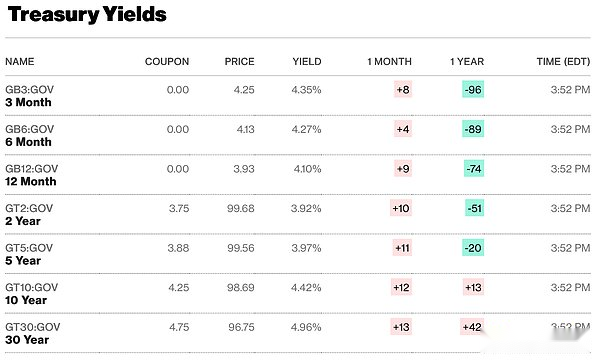

The Fed currently holds about 40% of Treasury bonds, which need to be rolled out at new interest rates.These Treasuries will have maturity dates in 2025 and 2026.Below I will attach a chart of US short-term Treasury bond interest rates for reference.

Currently, depending on the maturity examined, our debt ratio is about 4% to 5%.If this is short- to medium-term debt and is rolled out at the above interest rates, then this will become very unsustainable and thus fall into a debt spiral.If stablecoins become one of the biggest buyers of Treasury bonds, they can lower yields and will do so, especially in the short term.That’s why I think short-term demand, especially short-term Treasury bonds, is very eye-catching because it means they will basically become one of the biggest buyers of short-term Treasury bonds and will significantly alleviate the massive U.S. Treasury bond pressure.

In an interview, U.S. Treasury Secretary Scott Besent talked about the United States’ desire to become a leader in the digital asset field and use it as a means of putting pressure on global markets.

Obviously, Becent is a supporter of stablecoins.What could not be discussed a few months ago is that you don’t want to show your action plan to your opponent.I’m glad he’s one of the few people who figured out what the adoption of stablecoins in the United States might mean – given his background, it’s not surprising for those who know him and work in the financial field.I think he has a very advanced understanding of what a stablecoin might be or what it means to the US Treasury market.

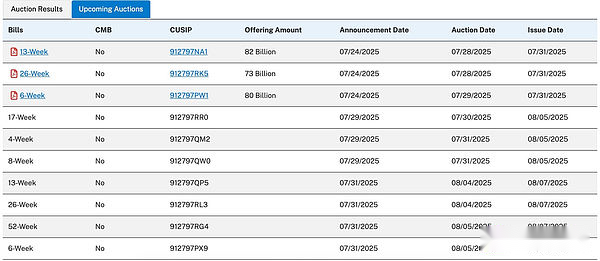

The U.S. Treasury Department is issuing different types of bonds, and on July 21, they auctioned $82 billion in 3-month Treasury bonds, which was a perfect auction.These are things that all people who work in finance or investing should pay attention to.

These auctions are very important because they reflect investors’ interest in buying U.S. Treasury bonds, both domestic and foreign.I also think Powell’s current approach is correct, namely, to cut interest rates less quickly, not only because economic data suggests that, but also because when interest rates remain high – especially the U.S. is the driver of the global economy – this will destabilize many other economies, mainly in Asia, Europe and South America.I say that because when interest rates are high, it will actually attract liquidity back to the dollar because investors will seek hedge.I think the current situation is that they want to force countries’ currencies to reconcile with the US dollar.So they can act in the bond market by keeping interest rates high.This could severely weaken the economies and/or currencies of these countries from a financing perspective, as the cost of capital in non-dollar denominated currencies becomes higher, making it harder to borrow.Therefore, those other countries will have to sell large amounts of assets to fund themselves and stabilize their economies.

When a country is in financial trouble—regardless of how it falls into that—it will be forced to sell assets to stabilize its economy, I’m sure the Trump administration is aware of that and is taking advantage of that fact.

Scott and the U.S. government seemed dissatisfied with Europe.They could have forced many countries to align with U.S. policies and everything proposed through means such as tariffs and bond markets, but the bond market is extremely important.

Financial stability or digital vulnerability?

Now, if the United States promotes stablecoin legislation and conducts tariff negotiations and trade agreements at the same time, I think there are many factors that will overlap, and the domestic pressure in Europe and Asia will be very high, and it may even trigger some kind of credit incident, which will basically lead to a decline in the stock market and everyone will flock to US Treasury bonds again.It depends on how fast and large-scale the stablecoins can develop, because if they develop too fast, we may encounter some kind of liquidity event (such as the money market fund run from 2008 to 2009, and even the brief decoupling of Tether from the US dollar in 2022), and even a spiral decline/run of liquidity, such as stablecoin redemption forcing short-term Treasury bonds to be sold.

In my opinion, some kind of event does need to happen.It’s like a compressed spring, or even a ball underwater.The deeper you press the ball, the more it wants to surface.This is what we see in Japan’s Treasury bonds and the UK’s debt market, etc.

An article written by a friend of mine at Barclays explores several key adoption risks for stablecoins.Stablecoins are digital assets designed to maintain stable value relative to reference assets.The main adoption risks highlighted by the article include:

-

Regulatory uncertainty: Stablecoins face huge regulatory scrutiny as regulators try to address issues surrounding their use, investor protection and risks posed to financial stability.In the absence of a clear regulatory framework, issuers, users, and financial institutions seeking to incorporate stablecoins into their business operations are facing ongoing uncertainty.

-

Operational resilience: The basic technical architecture of stablecoins, including smart contracts and support blockchain, must prove that they have strong stability, scalability and security.Operational risks posed by interruptions, technical failures and cyber attacks can undermine trust and usage.

-

Consumer Protection and Trust: Users must believe that the tokens are fully reserved and can be redeemed at the promised value.Inadequate transparency or poor reserve management may weaken confidence, resulting in value loss or other problems for holders.

-

Integration with existing systems: Stablecoins adoption may be hampered by the challenges of integrating new digital assets with traditional payments, banking and financial market infrastructure.To realize the advantages of stablecoins on a large scale, seamless interoperability is required.

-

Systemic risk: If poorly designed or under-regulated stablecoins are widely used, it may present new systemic risks to the wider financial system, especially if they account for a considerable share of payments or deposits.

These risks suggest that despite the broad prospects of stablecoins, their widespread use depends on clear regulatory standards, robust technology, transparent reserve management, and successful integration with existing financial ecosystems.

The politics of quietly monetization

Shashank Rai describes a phenomenon that can be called “quiet monetization”—how stablecoins create a secret way for a substantial increase in demand for U.S. Treasury bonds without expanding traditional government debt.Here is its mechanism:

Stablecoin issuers must fully support their tokens with current assets (the vast majority of them are short-term US Treasuries).As of early 2025, stablecoin issuers have held more than $120 billion in U.S. Treasury bonds, and this figure is expected to increase to $1 trillion or more by 2028.This creates what it says, “Even if the market is increasingly cautious about U.S. fiscal policy and long-term debt, short-term U.S. Treasury bonds will still become a structural and sustained source of demand.”

The UK has been slow to establish the necessary regulatory certainty around stablecoins.Stablecoins are a costly form of currency.They are expensive because they limit the monetary conduction mechanism (and thus reduce economic growth).The cost is high because they increase volatility in Treasury bonds (as well as the US dollar) and increase maturity premiums.The cost is high because they disperse liquidity.The cost is high because most of them have lower yields than money market funds.The cost is high, because blockchain transaction costs are an order of magnitude higher than domestic payment systems.

Stablecoins are a more risky form of currency.The risk is that they use the atomic swap model rather than the currency-currency countermeasure model.The risk is that its KYC process is much less regulated.The risk is also that blockchain has a concentrated risk around miners.

As a competitive form of currency, they should gain regulatory certainty and be included in the scope of regulation (this is different from the EU’s practice, which over-regulated, repeating its mistakes in the retail forex market, expelling the market overseas).However, the structure of stablecoins should not (as in the United States) understand the stability of the banking system or undermine confidence in the currency.Stablecoins properly regulated and operate within the scope of regulation will be able to fully interoperate with cash.In a capital market environment, this will eventually eliminate most stablecoins.Efficient markets, efficient liquidity, programmable currencies do not require blockchain-based stablecoins.

A good stablecoin regulatory structure requires:

-

Real-time Report on Redemption/Liquidity – Daily Net Assets Report

-

Regulatory capital based on RWA models (such as money market funds or banks)

-

Minimum short-term liquidity ratio (24 hours).

-

Regularly require transparent internal audits (systems and processes) – high-level personnel system (critical decision makers must be qualified).

-

CRO’s obligation to watch over regulators.

The stablecoin issuer should be able to fully access the central bank’s real-time full payment system, repurchase market and obtain central bank funds in a period of market pressure, just like banks.However, there should be no provision on the asset portfolio of stablecoins (except to meeting short-term liquidity needs).It should be transparent and decided by the market.

“Offshore quantitative easing” effect

The concept of “offshore quantitative easing” refers to the fact that stablecoins actually create demand for the US dollar globally without the need for the Fed to print more currencies:

Since stablecoins are driven by the market, users tend to choose the most stable and widely accepted stablecoins, so they naturally prefer strong currencies (mainly the US dollar) and may exclude weaker currencies.With the popularity of stablecoins, especially in emerging markets, the dollarization process may be further intensified.

The author believes that this will create “a new dollar-based game”, in which “fast and low-cost flows of stablecoins may marginalize weaker currencies, further consolidate the dominance of the US dollar, and reshape the international financial landscape by making the US dollar more accessible and liquid in cross-border transactions.”

Unlike traditional quantitative easing (QE) central banks that openly expand money supply, this operation is achieved through private market forces—stablecoin companies automatically purchase Treasury bonds to support their tokens, creating demand for Treasury bonds without government intervention.