summary

This article focuses on discussing the application scenarios of stablecoins.Stablecoins have special advantages in payment scenarios, and the market is particularly concerned that stablecoins are focusing on traditional payment fields, especially cross-border payments.There are “non-homogeneity” characteristics among different stablecoins, which makes competition between stablecoins particularly fierce.At present, US stock tokenization and AI Agent are important tracks for application promotion and will have a siphon effect on liquidity in global financial markets.

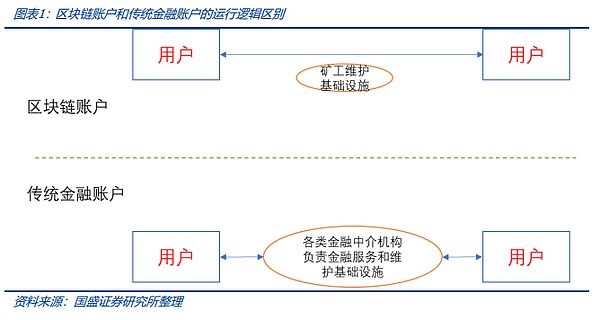

Stable coins have a simple account system, and Tokens are separated from the bank account system, making transfers and remittances between users extremely convenient, and have the characteristics of payment, that is, clearing – this forms another sharp contrast with the traditional financial system.Traditional financial accounts are provided by various financial institutions as centralized nodes to provide financial services. Financial institutions are responsible for maintaining users’ accounts and financial infrastructure, and at the same time charge users relevant fees.Transfers between stablecoin users are extremely convenient. Traditional cross-border remittances, international payments, and even stock transactions cannot be paid or cleared, and it will take a certain amount of time to complete the final settlement and delivery.On the other hand, the establishment of traditional financial institution accounts is much more complicated than blockchain accounts, and the light account characteristics of blockchain enable easy registration of an account as long as there are terminals such as the Internet and mobile phones.

The characteristics of “non-homogeneity” of stablecoins will make market competition very fierce.Although stablecoins of the same currency are equivalent in value, stablecoins issued by different issuers still have the characteristics of “non-homogeneity”.For example, as a stablecoin product under Coinbase, the USDC trading pair transaction volume is almost 1/8 of that of USDT.The market competition for stablecoins will be very fierce, which tests the scenario universality and promotion capabilities of stablecoin varieties.

Tokenization of US stocks is an important track that is expected to accelerate its implementation in the future. At the same time, the integration advantages of Agent and stablecoin accounts will have a siphon effect on global financial liquidity.Stablecoins, as an on-chain “fiat currency”, play an infrastructure tool. Stock tokenization is expected to become the next accelerated implementation of stablecoins and is the most planned promotional product in RWA.In addition, stablecoin accounts are naturally integrated with AI and are a very friendly choice for AI Agent payment.Stablecoins are built on blockchain light accounts and are native assets on the chain, which is very suitable for AI Agent to control accounts to achieve payment.These two application scenarios will have a siphon effect on global financial liquidity.At the same time, how do individual users and enterprises keep cryptocurrency assets?For enterprises, private key management is a complex issue.In short, this involves systematic construction such as asset security, internal control, compliance, and coordination among multiple countries.

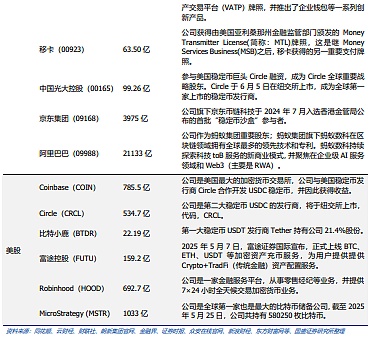

Investment Strategy:Stablecoins and RWA will still be hot topics in the market and will be catalyzed by the implementation of the US application and the process of issuing stablecoins in Hong Kong, China. The stock-based token and Agent interaction we mentioned is expected to become a new explosive point.It is recommended to pay attention to US stocks: Circle (CRCL), Robinhood (HOOD), Coinbase (COIN), Microstrategy (MSTR), Futu Holdings (FUTU), etc.; Hong Kong stocks: ZhongAn Online (HK6060), Lianlian Digital (HK2598), Hengyue Holdings (HK1723); A-shares: Sifang Jingchuang (300468), Zhongke Jincai (002657), Hengbao Holdings (002104), Langxin Group (300682), etc.

Risk warning:The research and development of blockchain technology is lower than expected; the uncertainty of regulatory policies; the implementation of the Web3.0 business model is lower than expected.

1. Core View

As a cryptocurrency, stablecoins have special advantages in payment scenarios. The market is particularly concerned that stablecoins are focusing on traditional payment fields, especially cross-border payments in international trade.At the same time, as a cryptocurrency, although different stablecoins (even anchored to the same fiat currency) are homogeneous tokens, they naturally have the characteristics of “non-homogeneity” due to different promotion channels and scenarios, which makes the competition among various stablecoins more fierce.From the current perspective, US stock tokenization and AI Agent will be the two important tracks for the promotion of stablecoin applications, which will have a siphon effect on global financial market liquidity.

This article analyzes the prospects of stablecoins entering the payment field, and provides an outlook on the role of US stock tokenization and AI Agent in promoting stablecoins, and explains the establishment of regulatory and compliance systems.

2. Stablecoins and traditional payments: two-way trip

2.1Stablecoins enter the traditional payment field: innovation in cost and settlement models

As a cryptocurrency backed by fiat currency assets, stablecoins are naturally characterized by peer-to-peer, decentralized blockchain accounts. Users have control over the account, and the blockchain infrastructure is maintained by miners.This is very distinct from traditional fiat currency (and other financial) accounts.Traditional financial accounts are provided by various financial institutions as centralized nodes to provide financial services. Financial institutions are responsible for maintaining users’ accounts and financial infrastructure, and at the same time charge users relevant fees.The simple account system of blockchain makes transfers and remittances between users extremely convenient and has the characteristics of payment as clearing – this is another sharp contrast with the traditional financial system. Traditional cross-border remittances, international payments, and even stock transactions cannot be paid as clearing, and it takes a certain amount of time to complete the final settlement and delivery. In addition to regulatory reasons, the working model of traditional financial institutions as centralized intermediaries limits their liquidation speed.On the other hand, the establishment of traditional financial institution accounts is much more complicated than blockchain accounts. For example, for many underdeveloped areas without banking services, it is not easy for people to obtain bank accounts. The light account characteristics of blockchain make it easy to register an account as long as there are terminals such as the Internet and mobile phones.

The above characteristics of blockchain are the advantages of stablecoins in the traditional payment field.Therefore, in communities in some underdeveloped countries, people can still register blockchain accounts through their mobile phones, use stablecoins to make daily remittances and retail payments, and especially the use of US dollar stablecoins can also deal with the depreciation of their own currencies.Interestingly, these regions may not even have banks that provide US dollar account services, but they can realize US dollar payments through US dollar stablecoins, which can be said to be “overtaking on the curve”.

As shown in the figure below, a transfer of about 2477 USDT was generated based on the USDT stablecoin deployed on the Ethereum blockchain. The miner charged a handling fee of about 0.23 US dollars (paid in ETH tokens). This remittance transaction was confirmed by the miner and entered into the blockchain after the transfer initiator initiated the remittance transaction, and the settlement was completed.

Of course, it is worth noting that the settlement speed of blockchain is limited by the impossible triangle (that is, decentralization, security and efficiency cannot reach the optimal value at the same time). When the network carries too many remittance transactions, the network settlement speed of blockchain will be limited to a certain extent, and the fee rate will also increase according to the situation.Therefore, if stablecoins want to be widely used in the payment field, they still need more expansion measures.

2.2Traditional giants are actively embracing stablecoins

Recently, many giants in the traditional Internet and retail sectors have shown great interest in stablecoins.Both Walmart and Amazon are exploring the issuance of their own dollar stablecoins to reduce payment friction, speed settlement and reduce costs associated with traditional financial channels; Hong Kong China’s Stablecoin Ordinance8moon1Japan will officially take effect. Ant International and Ant Digital Technology have stated that they will apply for a Hong Kong stablecoin license. JD.com’s stablecoin has entered the second phase of sandbox testing.Traditional large manufacturers actively embrace stablecoins.

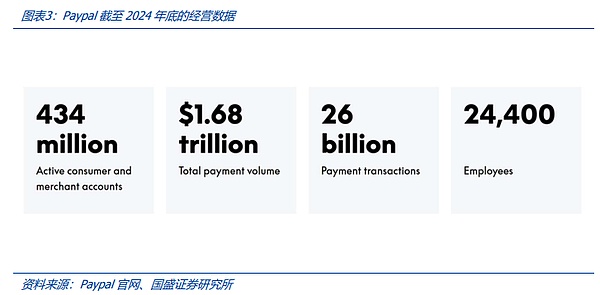

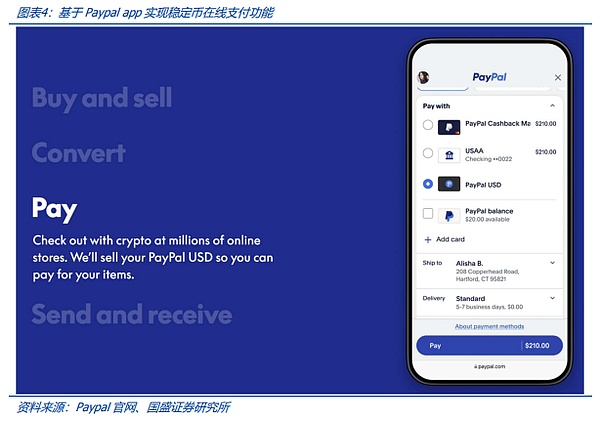

Taking payment giant Paypal as an example, as of the end of 2024, its company had more than 430 million active consumer and merchant accounts, with payments exceeding US$1.68 trillion.The US dollar stablecoin PYUSD (Paypal USD), a partnership between PayPal and Paxos, enables stablecoin payments in millions of online stores.Relying on such a payment giant’s application scenario, what is the current status of its stablecoin application?

But in fact, as of June 17, 2025, the supply scale of the stablecoin PYUSD was only about US$950 million, and its development was not satisfactory.This seems unexpected, but it is related to the competitive advantage of stablecoins.Taking the US dollar stablecoin as an example, different issuers promised to redeem their stablecoin products 1:1 against the US dollar, and there was no difference in value.We can compare it with fiat currency. In actual application, the US dollar in different bank accounts is no different, but even if they are both US dollar stablecoins, different currencies face inevitable competition. This is another manifestation of the programmability of stablecoins – from the perspective of computer program code, there are differences between stablecoins.We will explain the analysis of the competitive advantages of stablecoins anchored by the same fiat currency in the following article.

In short, as a new species, stablecoin products face special market competition logic.Even traditional large manufacturers, in the new field of stablecoins, want to promote products to seize the market, the challenges they face must follow different market logics.Therefore, whether it is a large company or a startup company, there will be certain potential possibilities in the stablecoin track.

3. The market competition for stablecoins will be very fierce

3.1 “Non-homogeneity” determines the universality of the scenario chain and is the key to competition

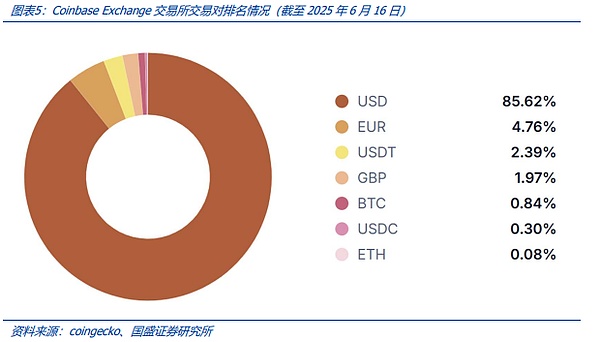

Although the stablecoins of the same currency are equivalent in value, the stablecoins issued by different issuers still have the characteristics of “non-homogeneity” – after all, from the perspective of blockchain programs, cryptocurrenciesThere are different codes in themselves.Taking the US dollar stablecoin as an example, although different types of stablecoins are promised to be pegged to the US dollar by their respective issuers, on the blockchain, just like the adaptation of different USB interfaces is not the same, stablecoin varieties also have certain “non-homogenization” characteristics.As the leading stablecoins, the transaction volume of stablecoins trading pairs in the Coinbase exchange is different. It is very interesting that the transaction volume of USDC trading pairs, as a stablecoin variety under Coinbase, has a large gap between the transaction volume and USDT trading pairs.As shown in the figure below, referring to the data on June 16, 2025, the transaction volume comparison of the stablecoin trading pairs on the Coinbase exchange is about one-eighth of the USDT.

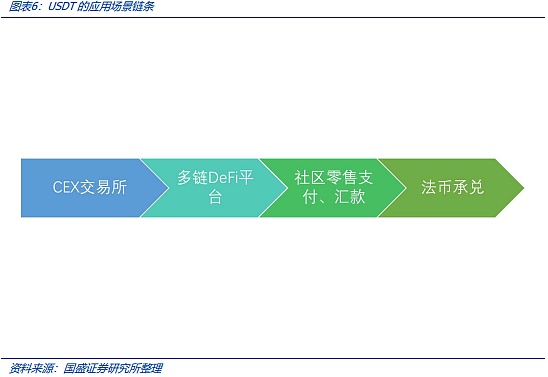

USDTAs the largest stablecoin variety, its versatility is the key to market competitiveness.As we all know, stablecoins are on centralized exchanges (CEX) and on multiple public chainsDeFiPlatforms (including decentralized exchanges)DEX, pledge lending platforms, derivatives platforms, etc.) have wide applications, not only that,USDTEven in underdeveloped communities,USDTIt also has the widest recognition and application habits.USDTHave more than in developing countries4100 million users, mainly used for remittances, providing services to unbanked users, and serving as a savings tool denominated in US dollars.Inhabitants in some parts of Africa, Central and South America are generally dependent onUSDT, to resist the depreciation of local currency, can be seenUSDTAcceptance services with fiat currency are also active as supporting services locally.

It is precisely the universality in this application scenario chain that makes USDT the most widely accepted tool and the largest US dollar stablecoin variety.As of June 17, 2025, USDT was over $156 billion, with the second-place USDC reaching approximately $61 billion.

Therefore, we believe that in the context of the introduction of stablecoin-related bills, there are not many thresholds for the issuance of stablecoins itself (and infrastructure is often based on existing public blockchain deployment). The key to large-scale lies in the universality of the scenario chain – that is, whether a stablecoin variety can be universal and multiple application scenarios and accepted by a wide range of user groups – this forms the moat of stablecoin varieties.This is an important reason why USDC’s trading volume is only one-eighth of USDT as a stablecoin product under the Coinbase Exchange.The aforementioned article mentioned that the stablecoin PYUSD supported by payment giant Paypal is less than US$1 billion, and we believe that the reason is that.

3.2Opportunities and challenges to open up a new payment system for stablecoins

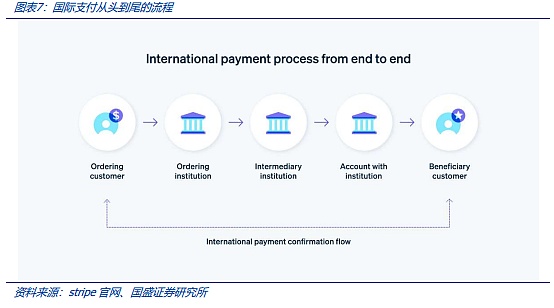

In the traditional payment system, the process of international payment is the most complex, involving multiple financial intermediaries such as payment institutions, intermediate financial institutions, and financial institutions where the user accounts are located, and involves conversion between multiple currencies.The light account system of blockchain payment, that is, cleared, is clearly different from traditional payment. Therefore, if stablecoins are integrated into the traditional payment system, corresponding infrastructure and services must be built.

The simplest scenario is, for example, the userAUS dollar stablecoin remittance to usersB, and convert it into Hong Kong dollar stablecoins, here it is bound to design exchange services between stablecoins.At the same time, it is also necessary to connect the stablecoin account system with the traditional fiat currency payment and clearing system.This requires the establishment of a payment system internationally, involving payment rules, regulatory regulations, financial service providers andITInfrastructure and other related construction.

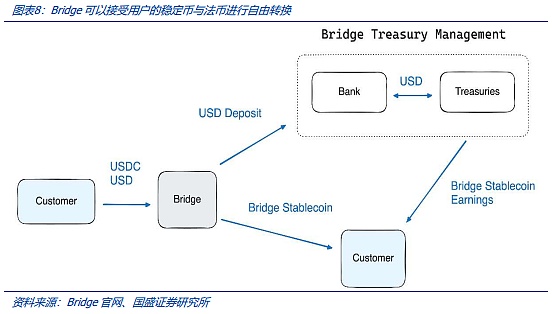

The integration of stablecoins and traditional payment systems requires the construction of hardware infrastructure and services.Currently, stablecoins are mainly used in retail payment and remittance scenarios. In the future, the more potential market is to expand stablecoins toB2BPayment and cross-border trade payment system.Stable CoinB2BThe payment and cross-border trade payment fields are potential markets that the industry continues to pay attention to.Previously, the payment giantStripeby11USD 100 million acquires stablecoin trading companyBridgeRecently, the company announced that it will adoptBridgeTechnology’s stablecoin financial account is now covered101A country/area.These institutions can collect payments through cryptocurrency or bank transfers and use stablecoins to make global payments.StripeWe are trying to connect stablecoin payment and traditional bank payment systems, which brings new development potential to stablecoins in the payment field.As shown in the figure below,BridgeUsers can useBridgeStable coins issued and managedUSDB(Bridge Stablecoin),BridgeThe stablecoins issued can be passedBridge Orchestration API(transfer, clearing address and virtual account) exchange with most stablecoins or fiat currencies.User usageBridge APITowardsBridgeSend fiat currency or stablecoin and you will receive itBridgeStablecoin (USDB),BridgeManaged in independent bank accounts and treasury escrow accountsUSDBReserve assets.

In other words, when users use the services provided by Bridge, they no longer deliberately distinguish between stablecoins (based on blockchain cryptocurrency accounts) or fiat currencies (based on traditional financial accounts). Bridge integrates the two account systems in terms of payment, remittance and clearing.

Therefore, it can be foreseen that in the process of stablecoins entering the trade payment and international payment systems, similar fiat currencies/Intermediate services for stablecoin convergence and conversion are indispensable, and this new demand is expected to create relevantITNew business models such as infrastructure providers and financial service providers.

Another challenge in stablecoin payment is payment efficiency.The traditional payment architecture is a centralized computing architecture, and a centralized architecture is beneficial to efficiency.Let’s take Alipay as an example. In 2017, the peak payments of 256,000 transactions per second were 256,000 transactions per second.It can be seen that traditional payment systems serve hundreds of millions of users, and the payment efficiency of 100,000 transactions per second is not a big problem.In contrast, blockchain cryptocurrencies naturally limit efficiency due to the characteristics of blockchain decentralized architecture.Taking the two public blockchains deployed by USDT, Ethereum and Tron as an example, the Tron chain can handle more than 2,000 transactions per second, while the Ethereum main network processes only double-digit transactions per second, and once the transaction popularity increases, it will be congested.The data here is still an ideal (network idle) state, and as the number of tasks carried by the network increases, the network will undoubtedly be congested.The blockchain network carries the payment efficiency of millions of users, which will surely become a key technical architecture issue that urgently needs breakthroughs.

4.Siphon Financial Liquidity: US Stock Tokenization (RWA) and Agent

Tokenization of US stocksRWAThe track is expected to accelerate its implementation in the next important track, which will drive the growth of demand for stablecoins, and at the same timeAgentThe advantages of integration with stablecoins will have a siphon effect on global financial liquidity.

4.1Tokenization of US stocks: New catalytics worth looking forward to in the second half of the year

Stablecoins itself are RWAs (Real World Assets) with cash as assets. They do not have investment value, but as an important on-chain “fiat currency” has the role of infrastructure tools. In addition to the stablecoin application scenarios described above, stock tokenization (Tokenized Equities) is expected to become the next major application market for stablecoins.

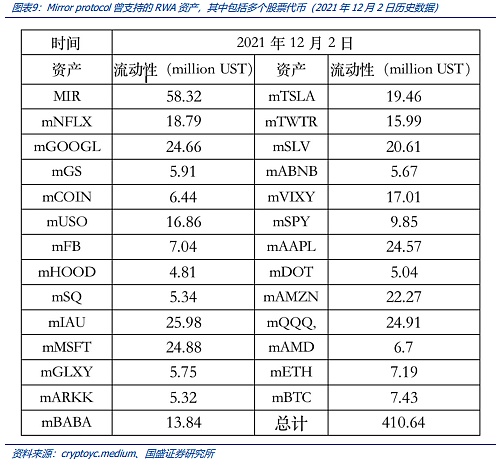

In the past few years, stock tokenization has been “a flash in the pan” in the development of the cryptocurrency market. The most representative one is Mirror protocol, whose platform provides users with various RWA products in the form of synthetic assets, including US stock tokenized assets such as Tesla, Google, Apple, Microsoft, etc. (as shown in the figure below).Later, due to regulatory and market fluctuations, stock tokenization gradually became silent.

Today, when RWA is rapidly promoting regulatory follow-up, the market is no longer satisfied with the returns of Treasury bond tokens, but instead pursues more flexible stock tokenization.Obviously, stock tokenization is a more attractive and huge market, providing more configuration options for cryptocurrency investors with different configuration needs.This direction has gained consensus between traditional financial institutions and cryptocurrency institutions, and stock tokenization is expected to gain stronger regulatory lobbying.Traditional financial institutions and cryptocurrency institutions represented by BlackRock are actively making suggestions to regulators to promote the implementation of stock tokenization.Recently, cryptocurrency exchange Coinbase is seeking approval from the U.S. Securities and Exchange Commission (SEC) for providing users with “tokenized stocks” transactions. The possible benefits of stock tokenization to cryptocurrency exchanges are self-evident.

Before that, the veteran cryptocurrency exchange KrakenIt plans to provide tokenized US stock trading options to non-US customers. On May 22, the full crypto exchange Kraken announced that it will cooperate with Backed Finance to launch a tokenized stock and ETF trading service called “xStocks”, covering more than 50 US-listed stocks and ETFs including Apple, Tesla, Nvidia, etc.

It can be foreseeable that stock tokenization is expected to be implemented at an accelerated pace, which will become an important application scenario for stablecoins, and the scale of the US stock market is enough to promote the rapid expansion of the scale of stablecoins.

4.2AI Agent Payment is another potential market

Stablecoins are a very friendly option for AI Agent payments.In the future AGI world, AI Agent will replace people to complete a lot of work, which inevitably involves payment.The payment process of traditional financial accounts, such as bank accounts, often requires user authorization, financial institutions’ review and other processes.This complex multi-node authorization workflow is not friendly to AI Agent.In many applications, AI Agent does not involve direct control of accounts and payments – payment operations are still operated by staff, while stablecoins are built on blockchain light accounts, which is very suitable for AI Agent to control accounts to achieve payments.

We believe that the introduction of smart contracts by Ethereum not only opens up the scripting capabilities of blockchain, but also perfectly integrates AI intelligent decision-making and account payment.In other words, AI Agent is no longer just an intelligent assistant providing analysis and advice, but can directly combine it with user accounts to realize the Agent’s manipulation of the account.This is reflected in many blockchain applications.

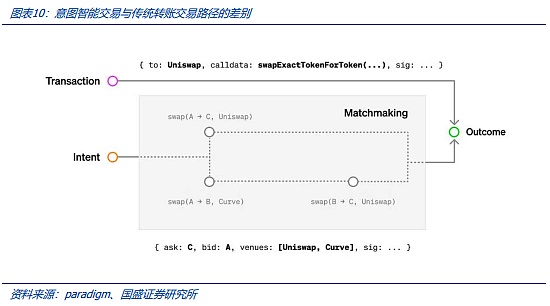

Let’s take Intent-centric applications as an example to see how AI intelligence integrates decision-making with payment.For example, the user wants to exchange Token A (A token) for Token B (B token) according to a certain expected ratio (note that there may not be any ready-made A/B trading methods as expected by the user at this time). The user only needs to provide this demand goal. As for the path through the process and which liquidity pool is used, the user does not need to consider it.Intent application is an intelligent AI agent that helps users conduct intelligent analysis and find the best trading path (or trading opportunity). Through Intent, the AI agent can finally achieve the result as long as the user signs and authorizes “one-click” signature.In the specific process, the Intent Protocol will use AI algorithms to optimize and solve the possible liquidity “routing” to find the best path to achieve user goals – this may involve multiple transaction pools (i.e. exchanges on the blockchain) and other transaction path methods.

From the above analysis, we can see that the signature transactions of blockchain accounts are highly integrated with AI algorithm solutions.This provides a certain basis for AI Agent to directly operate user accounts, that is, users can authorize “one-click” to authorize users, which can authorize users’ operation rights to AI algorithms.And this kind of fusion is universal, that is, blockchain accounts are naturally a smart contract, which has the genes of AI, including Lightning Loan, the core protocol of decentralized exchange DEX – AMM protocol (auto market maker, Auto Market Maker), etc., which reflect this feature.After stablecoins enter the payment field, the AI Agent can be used to promote blood circulation, which is expected to liberate users’ hands and have a certain room for imagination.

5.Regulation and compliance of stablecoins: Compliant payment systems still need to be established

The establishment of a stablecoin payment system is a systematic project.How do individual users and businesses keep cryptocurrency assets?Individual users can manage blockchain assets through private keys, but considering the threshold for the use and management of blockchain wallets, this is not a universal solution – after all, if an individual loses or forgets the private key, he will completely lose the cryptocurrency assets in the account (blockchain is a decentralized account and does not have central server or super account permissions). For enterprises, private key management is even more complex. People who have private keys have absolute control over blockchain account assets, and there is moral risk here.Of course, companies can choose to entrust cryptocurrency assets to professional institutions, such as IBIT, the Bitcoin spot ETF product issued by BlackRock, and its underlying Bitcoin spot assets are entrusted to professional institutions such as coinbase.If it is a payment application, stablecoin custody seems to bring many inconveniences in the payment process.In short, this involves systematic construction such as asset security, internal control, compliance, and coordination among multiple countries.

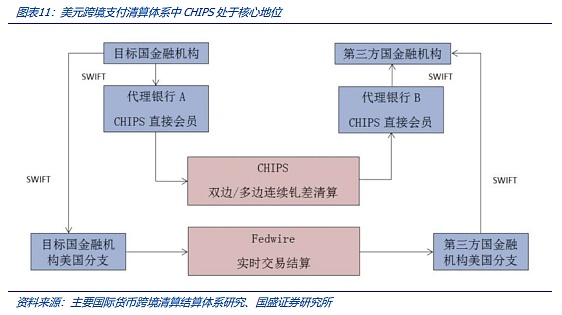

Many regulatory challenges brought by stablecoin payments, especially the offshoreization of fiat currencies.At present, the regulation of stablecoins in the payment flow process is in a blank state.The most direct consequence of the widespread use of stablecoins is the offshoreization of fiat currency.Globally, the cross-border clearing of US dollar is mainly responsible for US dollar cross-border clearing (CHIPS system) (New York Clearing House Interbank Payment System), and the US dollar transaction volume processed accounts for about 95% of the total global US dollar transaction volume (2020 data).Therefore, the United States can regulate the circulation of US dollar payments and circulation almost globally, which is also the basis for the long-arm jurisdiction of the US dollar business.The US dollar stablecoin issued on blockchain has the characteristics of “payment is clearing” and decentralization, and its payment and clearing are completed by the blockchain decentralized ledger.The United States does not have effective regulatory and control methods for blockchain cryptocurrencies—almost any cryptocurrency payment transfer is not controlled by the government and any other individual.

Therefore, the US dollar stablecoins issued on the blockchain are not subject to regulatory constraints, and the United States cannot control its liquidation.In the previous description, you can see the natural anti-regulation and anti-censorship characteristics of blockchain ledgers.Therefore, the dollar stablecoin is equivalent to the “offshore” dollar.This is a hidden concern that cannot be avoided in the development of stablecoins.UNODC) released a report in January 2024 saying that the US dollar stablecoin USDT has become the main tool for Southeast Asian criminals to launder money and fraud due to its ease of transfer and widespread acceptance.This is a microcosm of the offshore USDT caused USD to be the one that caused USD to be offshore.

In short, the current status of stablecoins is in the stage of first applying and running in with regulation.In any case, the application needs and business logic of stablecoins have basically matured. The regulatory policies of the United States and Hong Kong authorities in China will only play a normative role in the development of stablecoins, and provide a clearer business development logic for traditional financial institutions.

6. Investment advice: Pay attention to RWA and stablecoin related sectors

We believe that under the promotion of regulatory bills related to stablecoins in the United States and Hong Kong, China, the rapid development of the RWA and stablecoin markets will be ushered in.Stablecoins and RWA are still mainly based on theme investment. The market should pay attention to the implementation of applications such as tokenization of US stocks and the issuance of stablecoin licenses in Hong Kong, China, and other catalysis. It is recommended to pay attention to the related targets of RWA and the stablecoin industry chain.At the same time, for innovative applications native to blockchain, we should pay attention to its catalysis and changes to the financial market.

7. Risk warning

Blockchain technology research and development is not as expected: Bitcoin’s underlying blockchain-related technologies and projects are in the early stages of development, and there is a risk that technology research and development is not as expected.

Uncertainty of regulatory policies: The actual operation of blockchain and Web3.0 projects involves a number of financial, network and other regulatory policies. At present, the regulatory policies of various countries are still in the stage of research and exploration, and there is no mature regulatory model, so the industry faces the risk of uncertainty in regulatory policies.

The implementation of the Web3.0 business model is less than expected: Web3.0-related infrastructure and projects are in the early stages of development, and there is a risk that the implementation of the business model is less than expected.