Author: Michael Nadeau, The DeFi Report; Compilation: Deng Tong, Bitchain Vision

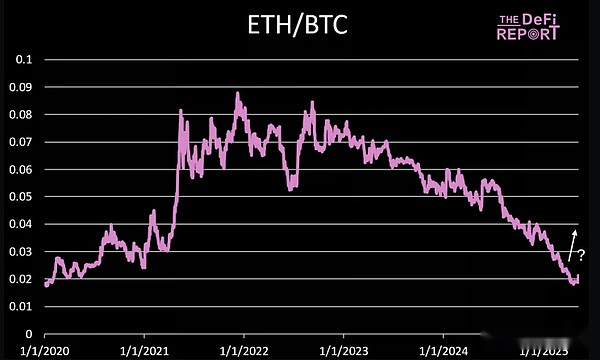

In January 2023, SOL’s trading price was 97% discounted to ETH.

By July last year, the discount had narrowed to 83%.

Now, nearly a year has passed.This gap is continuing to narrow as the market questions about Ethereum’s expansion roadmap and the assessment of Solana’s potential to “bring Nasdaq to the chain”.

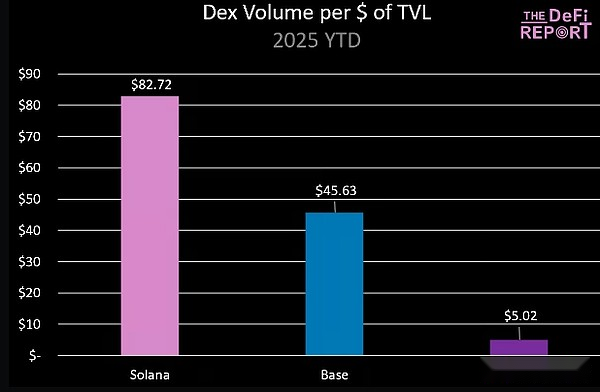

In past analysis, we focused on high-order KPIs such as fees, decentralized exchange trading volume, stablecoin supply and trading volume, total locked value (TVL), etc. to compare these two networks.

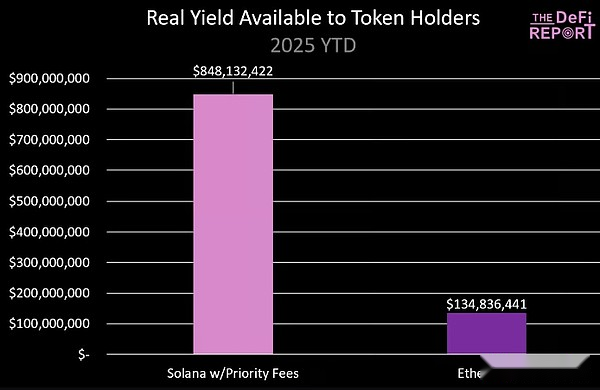

This week’s report will focus on the actual value available token holders.

The actual value available token holders

Solana

The actual value available to Solana token holder/stakeholder = Jito Tips (MEV) earned by the validator and shared with the stakeholder.This does not include newly issued SOL, base fees, priority fees, or MEVs retained by the searcher.

Solana’s $475 million is the net worth of Jito’s 6% handling fee charged to all validators running Jito Tips routers and block engines.If you hold SOL, you can stake to a trusted validator/LST, such as Helius (hSOL), which charges a staker a commission of $0.In this case, the SOL staker retains 94% of the MEVs run through Jito (95% of Solana’s stake runs on Jito).

Ethereum

Actual value available to Ethereum token holders/stakeholders = MEV + Priority fees earned by validators and shared with stakeholders.This does not include new ETH issuance, underlying fees, block fees, and MEV shares retained by searchers and block builders.

Ethereum’s $134 million net worth is deducted from 10% charges charged by Lido, the most trusted liquidity staking provider on Ethereum.

Key points:

Ethereum’s TVL is 6.6 times that of Solana and its stablecoin supply is 10 times that of Solana.

However, in terms of the actual value of year-to-date token holders, Solana is 3.6 times more valuable than Ethereum.

What is the reason?Execution and speed determine the actual value.This is how validators and token holders monetize TVL.

-

In TradFi, Nasdaq is responsible for execution and circulation speed.DTCC is responsible for hosting/closing.Ethereum is becoming more and more like DTCC (Accounting for Hosting + Settlement/L2 Transactions).Base and other L2 platforms are increasingly like NASDAQ (handling execution/circulation velocity).Solana is becoming more and more like a combination of the two.

-

Integrating Nasdaq + DTCC into one solution means SOL holders can get 100% of the execution/circulation velocity service value, while ETH holders can get about 10% of the value (acquired from the L2 platform by destroying ETH).

-

Ethereum owns these assets.But it needs to let them circulate on the chain.This has already started to work on the L2 platform and should continue to grow.The question now is whether ETH token holders will eventually get these values—and Solana has no such question yet.

-

In addition to some innovative LSTs on Sanctum, Solana validators will retain the 100% priority fees obtained from user transactions (not shared with stakers).Jito hopes to change this situation.DAO currently has a governance proposal that will update the tip router, including priority fees in addition to the MEV currently routed and paid to the stakeholder.According to Jito, the proposal is expected to be implemented in the coming months.

If we add the priority fee ($372 million, minus the tip router fee), the figures so far this year are as follows:

It is not clear how enthusiastic validators are about choosing a shared priority fee, but we want to add them here so you can get a look at how the numbers change.

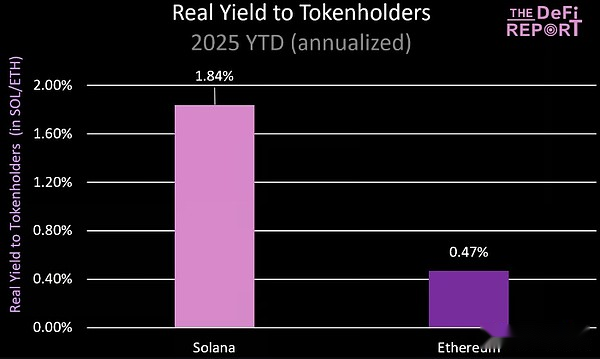

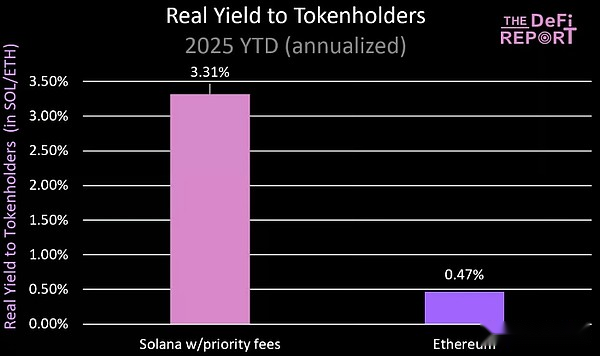

Actual rate of return percentage

Here is the data converted to annualized real rate of return (in SOL and ETH):

Preferential Fees for Using Solana:

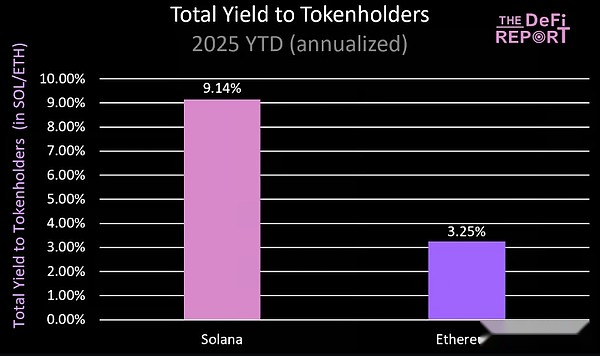

Total income (including issuance/network inflation):

Key points:

-

By pledging assets, token holders can obtain the supply/issuance of newly issued (used to incentivize validators/stakeholders to provide services).This is a key difference between an encrypted network and a company, as the company’s shareholders cannot avoid equity dilution.

-

Solana’s “Rate of Issuance” = 7.3%, based on actual network issuance as of June 5, 2025 (annualized).Ethereum’s “issuance rate” = 2.78%.

-

Solana has issued 9.4 million tokens that will be paid to SOLs pledged in validators on the network (as of June 5, 2025, the average pledge was 385 million).Ethereum has issued 329,380 ETH to the 34.3 million tokens pledged on the network to validators.

-

Due to the extremely low inflation rate of Ethereum (annualized yield is 0.64% based on actual data from year to date), its “issuance yield” has tended to normalize.Solana’s “issuance yield” will continue to decline as its network inflation is currently 4.5%, and it drops by 15% per year until it reaches a terminal inflation of 1.5%.

Source of true value

Solana

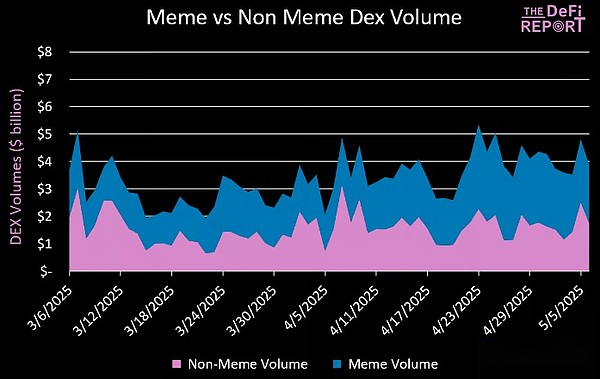

Memecoins accounted for more than half of Solana DEX trading volume (grown by 51% in the past few months).SOL/USD accounts for approximately 35% of DEX trading volume, while the remaining 14% consists of stablecoins, LST and other assets.

Is there any problem with this?

Yes, neither.

Obviously,Speculation/gambling is one of the most powerful use cases in cryptocurrencies.Solana finds a product/market fit by providing a better user experience.

We don’t think this will disappear in the near term.

Additionally, the memecoin transaction is stress testing the system and providing valuable feedback to infrastructure providers.

Memecoins today.Tomorrow’s stocks, bonds, currencies and private assets?

This is ultimately Solana’s goal.

If you are curious, 1-2% of the current DEX trading volume on Ethereum Layer-1 is memecoins.Stablecoin swap transaction volume accounts for about half, while ETH/stablecoin swap and other project tokens account for about 20% of the transaction volume respectively.

Currently, about 50% of the DEX transaction volume on Base comes from emoticons, and the vast majority of them come from the new Meme coins.

MEV

Some cryptocurrency analysts believe that as the underlying expenses are compressed/commonized over time, MEV (the value users pay for time-sensitive transactions) is the only long-term value that can last in Layer 1.

We disagree with this view, but we do think that MEV will drive most of the economic benefits.Therefore, it is necessary to clarify the differences in how MEV operates on Solana and Ethereum, and the possible impact of Layer 2.

Ethereum

Ethereum has a memory pool that all transactions pass through before being sorted and submitted to the validator.

The MEV market is here.The main participants are as follows:

-

Searchers: These bots use machine learning algorithms to identify profit opportunities in memory pools.

-

Block Builder: Block Builder is responsible for building blocks.In other words, they sort transactions by block and accept “bribes” from the searcher in the process.

-

Verifier: The validator approves blocks after the block builder submits them (with tips).

Workflow:

User Submit Transactions —> Ethereum Memory Pool —> “Searcher” (bot) Identify Value (arbitrage, sandwich transactions, clearing) —> Submit additional transactions to the block builder (including tips) —> Block builder package transactions —> Submit to the validator (including tips) —> Verifier approves the transaction, retaining most of the tips (block builders and searchers retain part).

The biggest unknown of Ethereum: What happens to MEV if most of the transaction volume shifts to Layer-2 as expected?

We believe that the MEV will be transferred to Layer-2 through a priority fee.The following figure shows that 85% of Base’s handling fees come from priority handling fees.

Solana

Solana has no memory pool.Instead, it has dedicated validator clients like Jito that implement some form of rolling private memory pool.

How it works:

Jito’s block engine creates a very short (about 200 milliseconds) window where searchers can submit transaction packages to include them in the next block.This scrolling memory pool is not public, but it is accessible to searchers connected to Jito infrastructure, allowing them to discover and exploit potential arbitrage opportunities within this short window.

Searchers usually directly monitor on-chain status (e.g., order book, liquidity pool) by running their own full node or RPC endpoint.They detect arbitrage opportunities by observing state changes caused by confirmed transactions, rather than by looking at pending transactions in the memory pool.

When profit opportunities arise (such as price imbalances between DEXs), the robot quickly builds and submits its own deals or packages them to the next block leader (usually via Jito or similar relays), hoping to seize the opportunity before others.

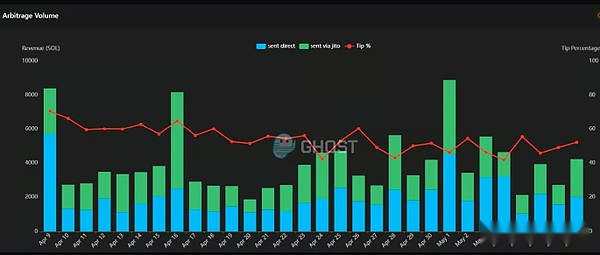

Currently, approximately 50% of the arbitrage MEV is done through Jito (this value is shared with the staker via a tip router):

If you are investing in these networks, you need to understand how MEVs accumulate for you through staking as a token holder.

We believe that SOL holders are currently more likely to receive MEV (and possible priority fees) than ETH holders.

Summarize

Should SOL trade at 65% discount to ETH (63.5% after complete dilution)?

From a fundamental perspective, it should not be.Even considering ETH’s excellent network effect, decentralization, Lindi agreement, asset guarantee and other factors, this discount is too high.

We conclude that, based on ETH’s network effects and total locked value (TVL), the market currently values ETH higher than SOL.

One of the highlights of ETH is that it will become the home of trillions of tokenized assets, covering stocks, bonds, currency/stable coins, private assets, etc.

This may be the case in the future.

But in the end,Investors need to pay attention to how ETH takes real value from these assets.

Why?

Because investors have a choice.If another chain can continue to bring more value to token holders, we should expect more capital to flow into the asset in the long run.

As Benjamin Graham once said:

“In the short term, the market is a voting machine. But in the long term, it is a weighing machine.”

One way ETH may catch up is through restaking and blob fee adjustments.With the launch of exciting new L2 layers, such as MegaETH (using EigenLayer for data access), ETH holders can get additional real value from these networks by restaking ETH.

We will conduct more analysis in these areas.

But we must be clear:

Today, crypto assets rarely trade based on fundamentals.

Although we believe this will happen, this is not the case at the moment.

Narrative, momentum, storyline, social influence and liquidity conditions are still factors driving the market.

Of course, ETH has been at a disadvantage in narrative games over the past few years.

But it feels like things are getting better.

A 20% volatility in a single day is nothing for assets worth more than $220 billion.

Remember: the cryptocurrency market is extremely reflective.Price —> Narrative —> Fundamentals.

Let’s wait and see if the recent fluctuations are just the beginning of a larger fluctuation.