Author: Dave Hendricks, Vertalo CEO Translation: Shan Ouba, Bitchain Vision Realm

Although “tokenization” is currently the hottest trend in the encryption field, especially in the field of DEFI, this is actually only another form of “securities token”.Although it is theoretically feasible to transfer traditional assets to the chain, the actual operation is far more difficult than people imagine.

“Vigatization”, especially “Real World Assets” (RWA) tokens, has recently been promoted to be the next disruptive trend in the encryption field.However, most people do not realize that this trend is actually another form of securities tokens, and the term has rarely mentioned since 2018 (this is not without reason).

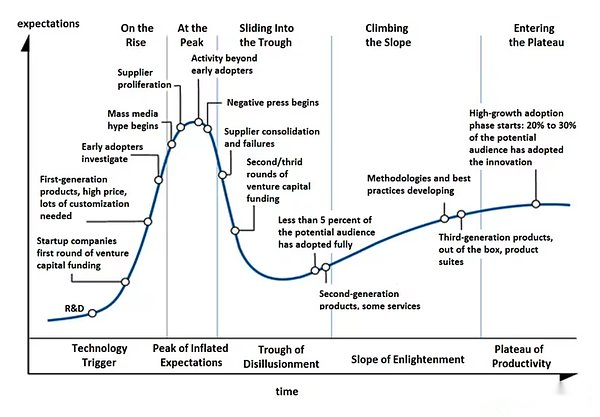

Most of the people who advocate the tokenization are wrong, but their starting point may be good.Some kinds of things should not blame anyone.However, if “securities tokens”, “tokens” and RWA are all the evolution routes of the same technology, then according to the “speculation cycle” theory of Gartner, another foam rupture may be coming.

>

Many current tokens are advocate from the former hype hotspot “Decentralization Finance” (DEFI).

Some traditional financial fields and CEOs have regarded tokens as a natural evolution of finance -for example, Berlaide CEO Larry Fink believes that the recently launched Bitcoin ETF is the “first step” of all things.However, the tokenization of “all financial assets” is much more complicated, and supporters and opponents are generally misunderstood.

The RWA Tokenization industry is about to usher in its eighth year, and its earliest dates back to the end of 2017.My company Vertalo launched a fully compliant REG D/S equity token project in March 2018, which is one of the earliest projects in the industry.Although we have encountered many challenges (unable to list them one by one), we have transformed from the original role “token equity issuer” to a “gold rush tool” enterprise software company, and is committed to “connecting and supporting digital asset ecosystems”.Essence

Since we have been engaged in the tokenization of physical assets, intangible homogeneous tokens (NFT) and decentralized finance (DEFI) have experienced large -scale atrophy of expansion and followers.NFT and DEFI are the applications that are easier to use by users.For example, in an easy -to -access market in Opensea, you can use tradable tokens to purchase computer -generated art.

If I let me map the development process of NFT to the hype period of the Gartner, I will put it in the peak period and quickly slide to the “disillusionment trough.”For example, OpenSea’s investor Coatue reduced its investment of $ 120 million to $ 13 million because the wealth of the exchange is decreasing.

Similarly, the once -hot DEFI market has also cool down -many projects now seem to be reshaping the brand and re -pay attention to the real world assets.These include the DEFI giant MakerDao and AAVE.

The team that preach the reputation of RWA now uses large traditional financial institutions as customers or partners, which makes sense, because many Defi founders emerged at Stanford University or Wharton Business School before entering the Wall Street Bank.

The DEFI movement is tired of providing a quantitative work for bond sales staff and stock traders, but they are also fascinated by the volatility and balance of work and life caused by decentralization. They are very familiar with the global financial world (and currency), butNot interested in its rules, regulations and strictness.

As a keen trend observer, the clever DEFI founder and their engineer mathematicians saw the ominous sign, and in 2022 withdrawn from the governance tokens investment game, and began to adjust their marketing and strategies to create “new”, New things”, that is, marked.result?Large-scale migration and use of RWA names, and quickly getting rid of any seemingly replicated and pasted things. This is the iconic measure and risk of the unpopular Defi world in 2020-22.

mostRWA projectGenerally managed assets and mortgages are mainly stable coins, not actual hard assets.

Vibration is not a quiet riots.If the current RWA market is mapped to the speculation cycle, it may just be in a “supplier surge” today.Everyone now wants to get involved in the RWA business and want to enter as soon as possible.

RWA’s tokenization is actuallyIt is a good idea.Today, the ownership of most private assets (RWA’s target asset categories) is tracked by electronic tables and centralized databases.If a certain asset is restricted to sell -such as public stocks, unknown bonds or cryptocurrencies -then there is no reason to invest in more easily sold technology.Old data management infrastructure in the private market is an inertial function.

According to RWA supporters, token has solved this problem.

Can I really solve this problem?

This kind of good faithful lies have a certain reason, but the absolute fact is that although the tokenization itself cannot solve the liquidity or legitimacy of private assets, italsoBring new challenges.The RWA tokens can easily avoid this problem, and they can easily do this, because most of the so -called real world assets that have been tokens are simple debt or mortgage instruments.The same compliance and report standards.

In fact, most RWA projects use an old process called “re -mortgage”. Among them, the mortgage itself is a cryptocurrency with a lighter supervision, and the product is a loan form.This is why almost all RWA projects use the yield of currency market types as their attractiveness.Just don’t pay too much attention to the quality of the collateral.

Borrowing is a big business, so I will not expect the future and long -term success of the tokenization.But it is inaccurate to bring the assets of the real world to the chain.It is just mortgage of crypto assets represented by tokens.Deputy currency is only a small part of this problem, and it is an important part.

When Larry Fink and Jamie Dimon talked about the tokenization of “each financial asset”, they were not talking about the encrypted mortgage RWA. They were actually talking about real estateAnd private equity, as well as the tokenization of the final public equity.This cannot be achieved through smart contracts.

First -hand experience

After more than seven years, a digital transfer agent and tokens have been established. The platform has carried out tokenization of nearly 4 billion units representing the interests of nearly 100 companies.many.

First of all, tokenization is only a small step in the entire process, which is relatively simple and not important.Hundreds of companies can already carry out assets of asset currency, which has made the tokenization itself a commercialized business, and the profit margin is quite limited.From the perspective of business models, the competition in the field of tokens will eventually evolve into a “cost reduction competition”. Because too many suppliers provide the same service, it will soon become a pure product.

Secondly, more importantly, there is a trustee responsibility when the tokenization and transfer of physical assets (RWA).This is the key part of the blockchain technology.

The distributed ledger has brought real benefits to the tokenization of financial assets by providing non -degeneration, auditability and credibility.This laid the foundation for prove that ownership and can immediately record all transactions.Without this, the financial use of tokens will have a revolution.

The trust created by the ledger will enable financial professionals and their customers to support the remarks of Larry Fink and Jamie Dimon, but this way is more likely to be adopted than DEFI and cryptocurrencies.

Therefore, before the start of the hype, look at what happened before and what would happen next.Don’t eventually go the wrong cycle, otherwise you will fall into the NFT version two.