Author: danny; Source: X, @agintender

Although this plunge was started by Trump, its catastrophic destructive power stems from the high-leverage environment within the native financial system of the crypto market.The high-yield stablecoin USDe, the recursive “revolving lending” strategy built around it, and its widespread use as margin collateral by mature market participants such as market makers, have jointly created a highly concentrated and extremely vulnerable risk node.

The USDe price de-anchoring event was like the first domino, triggering a chain reaction that spread from on-chain DeFi protocol liquidation to large-scale deleveraging in centralized derivatives exchanges.This article will break down the operating principle of this mechanism in detail from the two key perspectives of large position holders and market makers.

Part One: Powder Keg x Spark: Macro Triggers and Market Vulnerability

1.1 Tariff announcement: Catalyst, not root cause

The trigger for this market turmoil is: Trump announced plans to impose additional tariffs of up to 100% on all Chinese imported goods starting from November 1, 2025.The announcement quickly triggered a classic risk-off reaction in global financial markets.The news served as the catalyst for the initial sell-off in the market.

Global markets fell following news of the tariff war.With the Nasdaq plunging more than 3.5% and the S&P 500 down nearly 3% in a single day, the cryptocurrency market reacted much more sharply than traditional financial markets.Bitcoin prices plummeted 15% from intraday highs; while Altcoins suffered a catastrophic flash crash, with prices falling 70% to 90% in a short period of time.The total amount of cryptocurrency contract liquidation on the entire network exceeds 20 billion US dollars.

1.2 Existing situation: market abuses caused by speculative frenzy

Even before the crash, the market was already filled with speculative excess.Traders generally adopt high-leverage strategies, trying to “buy the bottom” on every correction to gain greater profits.At the same time, high-yield DeFi protocols represented by USDe have risen rapidly, and the ultra-high annualized yields they provide have attracted a huge amount of capital seeking returns.This has resulted in an environment of systemic vulnerability within the market, built on complex, interconnected financial instruments.It can be said that the market itself is already a powder keg filled with potential leverage, just waiting for a spark to detonate.

Part 2: Amplification Engine: Dismantling the USDe Circular Lending Loop

2.1 The Siren’s Song of Yield: USDe’s Mechanism and Market Attraction

USDe is a “synthetic U.S. dollar” (actually a financial certificate) launched by Ethena Labs. Its market value had grown to approximately $14 billion before the crash, making it the third largest stablecoin in the world.Its core mechanism is different from traditional US dollar reserve stablecoins. It does not rely on equivalent US dollar reserves, but maintains price stability through a strategy called “Delta Neutral Hedging”.The specific strategy is: holding a long spot position in Ethereum (ETH) and shorting an equivalent ETH perpetual contract on a derivatives exchange.Its “base” APY of 12% to 15% is mainly derived from the funding rate of the perpetual contract.

2.2 Construction of super leverage: step-by-step analysis of circular lending

What really pushes the risk to the extreme is the so-called “revolving lending” or “yield farming” strategy, which can amplify annualized returns to an astonishing 18% to 24%.The process usually goes as follows:

-

pledge: Investors will hold USDe as collateral in the lending agreement.

-

loan: Lending another stable currency, such as USDC, based on the platform’s loan-to-value (LTV).

-

exchange: Exchange the borrowed USDC back to USDe in the market.

-

re-pledge: Deposit the newly obtained USDe into the lending agreement again, increasing its total collateral value.

-

cycle: Repeat the above steps 4 to 5 times, and the initial principal can be magnified nearly four times.

This operation seems to be a rational maximization of capital efficiency at the micro level, but at the macro level it builds an extremely unstable leverage pyramid.

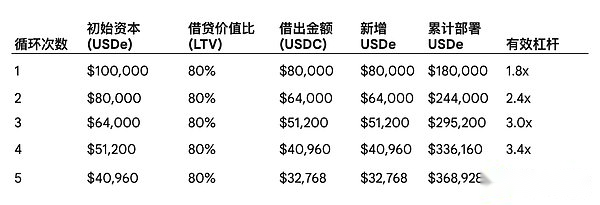

In order to more intuitively demonstrate the leverage effect of this mechanism, the following table uses an initial capital of US$100,000 as an example to simulate a revolving lending process assuming an LTV of 80%.(Data is not important, it mainly depends on logic)

As can be seen from the table above, an initial capital of only US$100,000 can leverage a total position of more than US$360,000 after five cycles.The core fragility of this structure is that just a small drop in the total USDe position value (for example, a 25% drop) is enough to completely erode 100% of the initial capital, thus triggering forced liquidation of the entire position that is much larger than the initial capital.

This circular lending model creates serious “liquidity mismatches” and “collateral illusions.”On the surface, a huge amount of collateral is locked in the lending agreement, but in fact, the real initial capital that has not been repeatedly pledged only accounts for a small part of it.The total value locked (TVL) across the system is artificially inflated because the same funds are counted multiple times.This creates a situation similar to a bank run: when the market panics and all participants try to close their positions at the same time, they are all scrambling to exchange huge amounts of USDe for the limited “real” stablecoins in the market (such as USDC/USDT), which will cause USDe to collapse on the market (although this may have nothing to do with the mechanism).

Part 3: The Perspective of Large Position Holders: From Yield Farming to Forced Deleveraging

3.1 Strategy Construction: Capital Efficiency and Revenue Maximization

For “whales” who hold a large amount of altcoin spot, their core pursuit is to maximize the income from their idle capital without selling assets (to avoid triggering capital gains tax and losing market exposure).Their mainstream strategy is to pledge their altcoins on centralized or decentralized platforms such as Aave or Binance Loans to borrow stablecoins.They will then invest these borrowed stablecoins into the strategy with the highest yield on the market at the time – the USDe circular lending loop mentioned above.

This actually forms a two-layer leverage structure:

-

Leverage Level 1: Lending stablecoins against volatile altcoins as collateral.

-

Leverage layer 2: Put the borrowed stable currency into the recursive loop of USDe and magnify the leverage again.

3.2 Preliminary shock: alarm of LTV threshold

Before the tariff news, the value of the altcoin assets used as collateral by these large investors was actually at a floating loss, and they were barely maintained by excess margins. When the tariff news triggered an initial decline in the market, the value of these altcoin assets as collateral fell.

This directly leads to an increase in their LTV ratio in the first level of leverage.As the LTV ratio approached the liquidation threshold, they received margin calls.At this point, they must replenish more collateral or repay part of the loan, both of which require stablecoins.

3.3 On-market (in-exchange) crash: chain reaction of forced liquidation

In order to respond to margin calls or proactively reduce risks, these large investors began to dismantle their revolving lending positions on USDe.This triggered huge selling pressure on USDe against USDC/USDT in the exchange market.Due to the relatively weak liquidity of USDe’s spot trading pairs on the exchange, the concentrated selling pressure instantly crushed its price, causing USDe to become severely unanchored on multiple platforms, with the price once falling to US$0.62 to US$0.65.

USDe’s destabilization within the market had two simultaneously devastating consequences:

-

Collateral liquidation: The plummeting price of USDe caused its value as collateral for revolving lending to instantly shrink, directly triggering the automatic liquidation process within the lending agreement.A system designed for high returns collapsed into a massive forced sell-off within minutes.

-

spot liquidation: For those large investors who failed to make margin calls in time, the lending platform began to force the liquidation of their initially pledged altcoin spot to repay their debts.This selling pressure directly hit the already fragile altcoin spot market, exacerbating the downward price spiral.

This process reveals a hidden, cross-sector channel of risk contagion.A risk originating from the macro environment (tariffs) is transmitted to the spot (USDe cycle) through the lending platform (altcoin mortgage loan), and is sharply amplified in the liquidation of collateral, and then the consequences of its collapse simultaneously backfire on the stablecoin itself (USDe de-anchored) and the spot market (altcoin liquidation).Risks were not isolated within any one protocol or market segment, but used leverage as a transmission medium to flow unhindered between different areas, eventually triggering a systemic collapse.

Part Four: The Crucible of Market Makers: Collateral, Liquidity, and the Crisis of Unified Accounts

4.1 The pursuit of capital efficiency: the temptation of interest-bearing margin

The market maker MM maintains liquidity by continuously providing bilateral quotes for buying and selling in the market, and its business is extremely capital-intensive.In order to maximize capital efficiency, market makers generally use the “Unified Account” or Cross-Margin model provided by mainstream exchanges.In this model, all assets in their account serve as unified collateral for their derivatives positions.

Before the crash, it became a popular strategy among market makers to use the altcoins they marketed as core collateral (at different collateralization rates) and lend out stablecoins.

4.2 Collateral shock: Passive leverage and the failure of unified accounts

When the price of the altcoin’s collateral plummeted, the value of the account used by the market maker as margin shrank sharply in an instant.This had a crucial consequence: it passively more than doubled its effective leverage.A 2x leverage position that was originally considered “safe” could turn into a risky 3x or even 4x leverage position overnight due to a collapse in the denominator (collateral value).

This is where the unified account structure becomes a vector for collapse.The exchange’s risk engine doesn’t care which asset caused the margin shortfall, it only detects that the total value of the entire account falls below the margin level required to maintain all open derivatives positions.Once the threshold is hit, the liquidation engine starts automatically.Instead of just liquidating altcoin collateral that has plummeted in value, it will start forcing sales of any liquid assets in the account to cover the margin gap.This includes a large number of altcoin spot stocks held as inventory by market makers, such as BNSOL and WBETH.Moreover, BNSOL/WBETH was also broken at this time, so other previously healthy positions were further included in the liquidation system, causing collateral damage.

4.3 Liquidity vacuum: the dual role of market makers as victims and vectors of infection

While its own accounts were being liquidated, the market maker’s automated trading system also executed its primary risk management directive: withdrawing liquidity from the market.They canceled buy orders on thousands of altcoin trading pairs en masse, withdrawing funds to avoid taking on more risk in a falling market.

This created a catastrophic “liquidity vacuum.”At a time when the market was flooded with selling orders (collateral liquidation from large positions and unified account liquidation by market makers themselves), the market’s most important buyer support suddenly disappeared.This perfectly explains why altcoins experience such violent flash crashes: Due to the lack of buy orders on the order book, a large sell-to-market order is enough to knock the price down 80% to 90% in a matter of minutes, until it hits a sporadic limit buy order well below the market price.

In this incident, another structural “catalyst” was the liquidation robots that liquidated the collateral. When the liquidation line was reached, they would sell the corresponding collateral at the spot market, which caused the altcoin to fall further, triggering the liquidation of more collateral (whether it was the collateral of large investors or market makers), which in turn led to a spiral stampede event.

If the leverage environment is gunpowder and Trump’s tariff war announcement is fire, then liquidation robots are oil.

Conclusion: Lessons from the Cliff – Structural Vulnerabilities and Future Implications

Review the cause and effect chain of the entire incident:

Macro shock → Market risk aversion → Liquidation of USDe revolving lending positions → USDe unanchored → On-chain revolving loan liquidation → Market maker collateral value plummeted and passive leverage soared → Market maker unified accounts were liquidated → Market makers withdrew market liquidity → Altcoin spot market collapsed.

The market crash on October 11 was a textbook case that profoundly revealed how novel and complex financial instruments introduced catastrophic and hidden systemic risks into the market in the pursuit of ultimate capital efficiency.The core lesson from this incident is that the blurring of the boundaries between DeFi and CeFi has created a complex and unpredictable risk contagion path.When assets in one area are used as underlying collateral in another area, a local failure can quickly turn into a crisis for the entire ecosystem.

The crash is a harsh reminder: In the crypto world, the highest yields are often the compensation for hedging the highest and most hidden risks.