This article is compiled from Goldman Sachs’ latest research report “Stablecoin Summer”

The summer of stablecoins has arrived.

The GENIUS Act recently implemented in the United States has established a federal stablecoin regulatory system.

Walmart, Asiason and large financial institutions are reportedly exploring the launch of their own stablecoins.And Circle, the issuer of the world’s largest stablecoin, the USD Coin (USDC), has recently been listed in a buzz.

So, is the summer of stablecoins endurance, and what might this mean for issuers, existing payment and banking systems, markets, and more general financial stability?

⾸First what are stablecoins and how are they used today?

In short, stablecoins are digital currencies operated on blockchain.Their value is usually pegged to fiat currencies in a 1:1 ratio, and the most commonly US dollar, which distinguishes them from other cryptocurrencies whose value is determined by the supply and demand of coins.

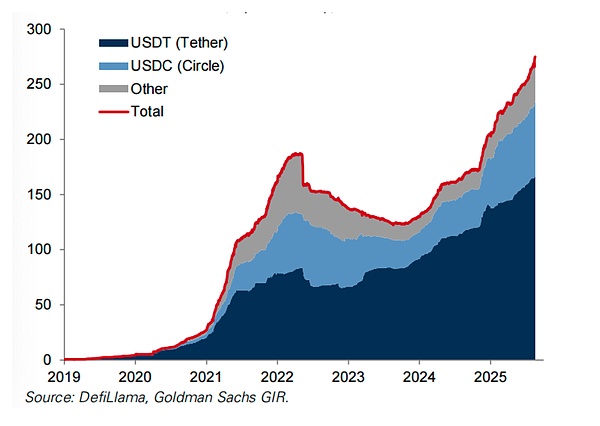

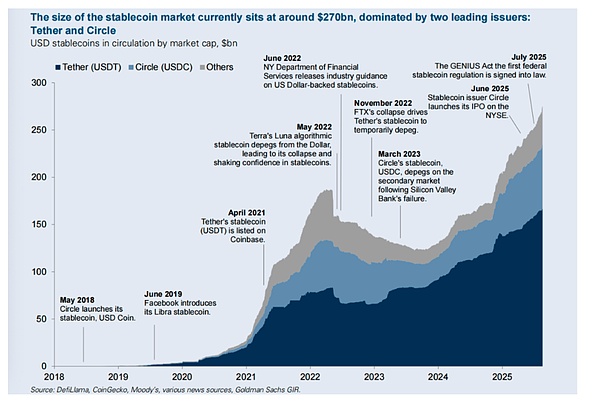

Since Circle launched USDC in 2018, the stablecoin market has grown significantly, with a total market value of about $270 billion, as stablecoins have become a means of cross-border transfer of funds and obtaining US dollars outside the United States.

So, will the stablecoin market continue to grow?

We interviewed Brian Brooks, former Office of the Supervisory Administration, who thinks it will.He expects a stablecoin “gold rush” to usher in a stablecoin “gold rush” after the recently passed GENIUS Act, which he said has created a new sense of security for the use of stablecoins, given that the bill requires stablecoins to be anchored with 1:1 high-quality assets such as U.S. Treasury and bank deposits.

So, what impact may this increase have?

James Yaro, a cryptocurrency and interbank market analyst at Goldman Sachs Brokerage, first elaborated on the business models and business opportunities of the entities closest to these digital assets, stablecoin issuers.He believes that as asset tokenization is still in its infancy, this opportunity will continue to increase.

Next, we explore what the popularity of stablecoins may mean for entities that seem to be most vulnerable to stablecoins—the traditional payment channels.

WillNance, a Goldman Sachs Payment and Digital Asset analyst, believes that the risks of existing remittance companies are exaggerated, noting that most of the costs in cross-border payments are concentrated in areas where stablecoins cannot directly solve, such as up- and down-chain costs and regulatory/compliance-related costs (although Brian Brooks notes that, as many places accept USD and cryptocurrencies, it is much easier to avoid some of these costs by holding blockchain-based assets in many developing countries than many think).

Nance said traditional consumer payment companies already play an important role in facilitating stablecoin trading, which is usually underrecognized, and he expects that this will continue.Therefore, Nance believes that many remittance/consumption payment companies that have underperformed in stablecoins that may undermine their business model are valuable.

So, what is the impact on Treasury bonds, which are the main supporting assets of stablecoins?

Brian Brooks expects stablecoins to provide a meaningful source of Treasury bond demand, noting that Tether, which did not exist before 2014, recently disclosed that it ranks among the top 20 global Treasury holders.

But William ⻢chelle and Bill Zhu, senior interest rate strategists at Goldman Sachs, found that the impact on Treasury demand will ultimately depend on the timing and scale of stablecoins adopted, the speed of stablecoins turnover and the source of funds flowing into stablecoins. Inflows from money market funds may have the least net impact on Treasury demand, while inflows from physical currency holdings, overseas investors seeking US dollar exposure, and bank deposits may have a greater impact.

Richard Rumsden, head of Goldman Sachs Financial Group, then assessed the potential possibility of a shift from Bank of America to stablecoins, who believes any major migration requires stablecoins to offer better economic or lower payment friction than traditional deposits, neither of which seem unlikely in the near future.

But in today’s world of fiat currency issued by governments, perhaps the most important question is whether the proliferation of private stablecoins will affect financial stability?

We interviewed Professor Barry Eichengreen of the University of California, Berkeley who feared that the GENIUS bill would cause “economic chaos” if it led to an unpopular, unacceptable stablecoins, which were priced at different prices.

In this regard, he was not at ease with the reserve requirements of the GENIUS Act, believing that in his opinion, the closest history to stablecoins, private banking bonds during the free banking era were intended to be completely secured by high-quality assets, but often not, which triggered bank panic.

Although he agrees that stablecoins may be a (marginal) source of Treasury demand, he fears that stablecoins could also exacerbate volatility in the Treasury market if large-scale redemption forces stablecoin issuers to quickly sell Treasury bonds in the crisis.

But Brian Brooks is firmly opposed to comparing stablecoins with the free banking era, explaining that in that era, also known as the Wildcat era, each bank issued its own banknotes and called it the US dollar, but the reserve assets of each bank vary.

He said the entire purpose of the GENIUS Act was to require all stablecoins to be supported by the same set of assets, which made it more similar to the National Bank Act of 1863, which ended the problematic era of wildcats by requiring all banks to hold government bonds at a certain proportion.

Given the debate over the pros and cons of stablecoins, Zhu then compared them to the often discussed alternative, the central bank digital currency (CBDC), which, while the recent U.S. law seems to have shut down the big picture in this area, many other countries are still advancing, finding some common ground, but also important differences.

Interview with Brian Brooks:

He is a director and CEO of the US Currency Comptroller in 2020-21, and a member of the board of directors of Strategy (formerly MicroStrategy).

He believes that with the passage of the GENIUS Act, stablecoins will usher in a gold rush.

Allison Nathan: How are stablecoins used now and how do you expect it to develop?

Brian Brooks: The most critical application scenario at present is the US dollar savings product.

In countries where dollar bank accounts are difficult to obtain, depositors and even institutional investors use stablecoins, a dollar-equivalent product that expands demand for the dollar and creates price stability in volatile or inflationary economies.

A classic example is Argentina, where many people prefer to hold Circle’s USD coins (USDC) than pesos.

Many businesses in Latin America and Africa are based on this premise, while many startups in the BRICS countries allow retail users to hold dollar equivalents through stablecoins.This use will increase significantly.

It is conservatively estimated that 2 billion adults worldwide live outside the United States, and they prefer to hold all their net assets in US dollars, but they do not currently hold them.

Remittance is another major application scenario, because stablecoins are digital manifestations of currency and can be transferred across borders.

If stablecoins don’t do anything other than helping consumers avoid paying cross-border remittance fees, this alone is extremely valuable in itself, as such fees on average are about 7%.

But the benefits go beyond that, as stablecoins are a convenient way for many developing countries to avoid foreign exchange trading.

When I traveled to parts of Latin America, I found that local financial infrastructure was lagging behind, i.e., small banks and low actual usage, which meant that almost every place accepted US dollars, consumers could shop without the need to exchange local currency, and many merchants also accepted cryptocurrencies.

Therefore, it is much easier to hold funds in the form of blockchain assets in developing countries than one might think, further demonstrating the advantages of stablecoins in cross-border payments.

Despite attracting a lot of headlines, payment uses are the last and least important.

Stablecoins are designed to break down barriers between non-cash digital payment tools like USD, such as AppleCash, Starbucks and American Games membership rewards – and create universal payment features.

Most people in developed countries are already reasonably served through existing payment tools, so this is currently a relatively small market.However, given its speed and lower fees, stablecoins are likely to gain popularity as a payment tool.

AllisonNathan: Does the high fees of existing payment channels cover valuable services such as fraud protection?Do you expect stablecoin issuers to do the same in the end?

BrianBrooks: I believe that proper risk management can create a safe environment.

Today’s blockchain technology can significantly enhance fraud protection—the transparency and decentralized consensus mechanism of its inherent blockchain are its security.Therefore, traditional payment companies execute and make backend features that consumers think are security-related today may eventually become redundant.

Allison Nathan: Will the lack of interoperability between blockchains limit the increase in stablecoins as payment tools?

Brian Brooks: Indeed, blockchain is not universally interconnected at present, and the Solana blockchain does not communicate with Avalanche or Ethereum blockchain.

But since Circle launched USDC on the Ethereum network in 2018, significant progress has been made in developing “intercommunication layers” that allow communication between different blockchains.

Currently, there are three major players – Axelar, Wormhole and LayerZero – competing to win the universal interoperability competition.I expect to see a world like this soon, when all blockchains will be incommunicated as ATM networks initially, but now they can communicate with each other as they are.

But universal interoperability is only half the battle.

Stablecoins must also be substitutable, which means that each stablecoin must be fully accepted anywhere.

For example, I should be able to deposit USDC tokens as USD into my bank, which I cannot do at the moment.

However, similar to the experience that traveler checks were initially accepted only at issuers but later became generally accepted, I expect this substitutability to come with the general demand for stablecoins from consumers.And the GENIUS Act will play a key role here.

Allison Nathan: How does the GENIUS bill change the outlook for stablecoins?

Brian Brooks: The GENIUS Act has built a regulatory system similar to that of the state’s banks for stablecoins, which is crucial.

Many people don’t adopt stablecoins, mainly because they think banks are safer, and the FDIC insurance logo posted by bank branches lets customers know that even if banks go bankrupt, their cash will not be in danger.

Cryptocurrencies have never felt this sense of security.

But the GENIUS Act changed this by requiring all U.S. stablecoin issuers to be regulated by one of the three U.S. national banking regulators (Federal, FDIC and OCC) or state banking institutions to maintain their coins’ reserves at least 1:1. The reserves are composed of high-quality, liquid assets and disclosed their reserves every week.

This regulation will give a sense of security to stablecoins, which will drive large-scale market adoption.

AllisonNathan: How confident can we really be that federal regulators, especially state regulators, can regulate this innovative technology?

BrianBrooks: I am pleased with the fact that many crypto companies are now trying to become national banks by applying for national bank licenses, which are “continuously regulated”, which means bank inspectors are always on site and can conduct targeted inspections at any time.

The greater concern is whether bank inspectors are well aware of stablecoins and underlying blockchain technology to provide adequate supervision.But regulators are always a step behind new technologies, and that’s no exception.They will learn more tomorrow than today.The same is true for auditors. Almost none of the four auditing companies would audit a cryptocurrency company before the New Year.But now they all have cryptocurrency business practices because the field is already big enough to be worth the necessary learning.Government agencies will do the same.

Allison Nathan: But can regulators effectively regulate the potential thousands of stablecoin issuers that may enter the market now?

BrianBrooks: I don’t agree with this scale.The crypto-native stablecoins, Tether and USDC, which currently dominate the market, are likely to continue to dominate. Tether is about to issue a US version of token that complies with the GENIUS Act, thus enabling it to operate in the United States.

The banks I talked about are not going to launch a stablecoin with a market capitalization of $100 billion for people to participate in remittances or decentralized finance.

Instead, they view stablecoins as a means to reduce funding costs and enhance customer stickiness through loyalty program tools.

They can achieve both goals by issuing electronic tokens that will be converted to USDC or Tether for other purposes.

As a result, the stablecoin market may be polarized, consisting of two large global stablecoins and more locally based tokens that are more easily regulated.

Allison Nathan: The GENIUS Act requires stablecoins to be backed by “safe” collateral, but this includes bank deposits, etc., and recent history has shown that these deposits are not always safe.Does this worry you?

Brian Brooks: If Bank of America deposits are not considered safe, then we have bigger problems.

Concerns about Circle’s $3 billion deposit held by Silicon Bank (SVB) did cause USDC to briefly dean during the 2023 banking crisis.But Circle didn’t lose any penny of the $3 billion.The market response is negative because the FDIC rules are not well understood.

Indeed, FDIC only insures up to $250,000 in deposit accounts.But Circle’s funds are covered by FDIC penetration insurance, which ensures that all the underlying customers of Circle deposited funds in SVB can receive up to $250,000.

To prevent such deposits from being fully insured in a future crisis, some crazy math is required.

So, I’m not particularly worried – insured bank deposits in the United States may not be completely safe, but they are safer than almost everything else.

Allison Nathan: Some people compare stablecoins to the free banking era, when the proliferation of private currencies led to multiple banking crises.What do you think?

Brian Brooks: I have a different view.Stablecoins differ from that period known as the “wildcat banking era”, partly because the main constraints on stablecoin issuance are the availability of government bonds and bank deposits.

In the era of Wildcat Bank, each bank issued its own bank vouchers and called it the US dollar, but the reserve assets of each bank vary.Therefore, the dollar of one bank does not have the same value as the dollar of another.

The entire purpose of the Genius Act is to require that all stablecoins must be supported by the same set of assets.In this sense, it is similar to the National Banking Act of 1863, which requires all banks to hold government bonds in a proportion to support bank bonds, ending the problematic wildcat banking era.

Allison Nathan: What might the popularity of stablecoins mean for commercial banks?

Brian Brooks: Some banks feel that stablecoins threaten them, while others feel that stablecoins give them power.

Community banks worry that stablecoins will draw low-cost deposits from the banking system, which is part of the reason they support the GENIUS Act’s prohibition of stablecoin issuers from paying interest to token holders.

But medium-sized banks and digital banks, which operate completely online, view stablecoins as both tools that attract deposits and enhance customer stickiness, which may enable other business lines, such as cryptocurrency trading businesses.

Therefore, with the popularity of stablecoins, the fate of various banks may diverge.

Allison Nathan: What about the need for the Ministry of Finance?

Brian Brooks: Stablecoins will provide an important source of Treasury demand.

Tether did not exist until 2014, and it recently disclosed that it has entered the top 20 global holders of Treasury debt.

As we have discussed, there is a huge global demand for the US dollar, especially in developing countries, and stablecoins are the digital manifestation of the US dollar.Now, whenever a new stablecoin is issued, a dollar of Treasury bonds must be purchased to support it.Therefore, the GENIUS bill will release unprecedented demand for US dollar, which will increase the demand for Treasury bonds to reach a percentage of the total issuance.

Allison Nathan: Can central bank digital currency (CBDC) provide a better alternative to stablecoins?

Brian Brooks: I think this is an ideological issue.I don’t want the government to have the right to review my transactions; neither the public or private department officials should be able to arbitrarily reject transactions they consider unethical or exclude people from the financial system for no reason.The beauty of stablecoins is that since they are based on decentralized consensus mechanisms, I prefer a world like that, so no one has to trust anyone.

Allison Nathan: When will the future state of the stablecoin you expected will become a reality?

BrianBrooks: With the passage of the GENIUS Act, I expect the future status to become a reality within two years and to scale within five years.Therefore, the next three years will be a gold rush.

Allison Nathan: Is there anything that could hinder this future plan?

Brian Brooks: The Fed may tighten monetary policy, which will limit the money supply, causing the stablecoin gold rush to end before it really begins.

Furthermore, while the current blockchain is difficult to be attacked by customers, I am worried that malicious actors may break through the blockchain network, manipulate or fraudulently create stablecoins.In the future of quantum computing, this situation is not impossible and may destroy market confidence.Despite these risks, I expect stablecoins to become ubiquitous as they solve practical problems, so I have confidence that they will overcome any potential obstacles.

Interview with Barry Eichengreen

Barry Eichengreen is an outstanding professor of economics and political science at the University of California, Berkeley.

He believes that the proliferation of stablecoins may undermine the “single currency” principle that is crucial to economic stability and introduce greater volatility into the Treasury bond market.

The views mentioned in the article are the personal views of the interviewees and do not necessarily reflect the GS.

Allison Nathan: You have said the GENIUS Act will cause economic chaos.What are your concerns about this method?

BarryEichengreen: My main concern is that the proliferation of stablecoins may undermine what economists call “monogeneity of currency” that every dollar should be traded at the same price and accepted anywhere, which is crucial for economic stability.

The GENIUS Act could lead to a flood of currencies and quasi-currencies that could be inoperable and could be traded at different prices, forcing merchants to carefully review the value of each stablecoin they receive.

This will introduce additional costs, inefficiency and risks to the payment system.

It is important to point out that the United States has tried private currencies in the past, which are essentially stablecoins and often have catastrophic consequences for financial stability.I’m worried that stablecoins might be the same path.

The United States has tried private currencies in the past, which are essentially stablecoins and often have catastrophic consequences for financial stability.I’m worried that stablecoins might be the same path.

Allison Nathan: Which of these past cases are the most similar?What lessons should we learn from this?

Barry Eichengreen: The most direct historical similar case was the Free Banking Period, which lasted from the mid-1830s to the early stages of the Civil War, when banks in many states could issue their own bank notes.

In principle, these banks must exchange gold of one dollar of equivalent value for one dollar of bank notes.But in reality, banks sometimes lack sufficient collateral to fully exchange their notes, resulting in different bank notes being traded at different values based on the expected exchange risk of the issuing bank.

When serious concerns arise about the ability of banks to exchange notes, a run occurs, resulting in bank runs and bank panic.Therefore, experience during the free banking era issued a harsh warning to stablecoins.

The same is true for the past events involving money market funds.In 2008, a large fund fell below one dollar and its value fell to $0.97 per share, causing chaos and contagious concerns that ultimately forced the government to prepare and guarantee the value of money market funds.

Similarly, in 2023, the collapse of Silicon Bank (SVB) was triggered by an increase in losses as interest rates rose, resulting in a deposit run, requiring the government to prevent feared financial contagion.

The government may also be responsible for the redemption of stablecoins and the taxpayer shall bear the costs.The bank pays the FDIC’s insurance fund, thus paying the fee that allows depositors to receive full compensation to the insurance limit.Stablecoins do not have similar mechanisms.Therefore, taxpayers will be directly implicated.

Allison Nathan: The GENIUS Act requires stablecoin issuers to hold collateral equal to or exceed the value of their issuance, and these collaterals must be high-quality, high-liquid assets.So, can this make you feel at ease?

Barry Eichengreen: This only provides some limited comfort, but history shows that assets considered high-quality today may become lower on the day.In the free banking era, the stocks of the banknotes circulating in the era of free banks and the troubled money market fund reserve primary fund should theoretically be fully collateralized by high-quality assets, but this is not the case in practice.

Although U.S. Treasury bonds account for the majority of stablecoin reserves, issuers are allowed to hold reserves in other forms such as bank deposits that could face risks.Some large stablecoin issuers will reserve deposits as deposits for Silicon Bank (SVB), and holders fear that these deposits will not be insured, causing their currency to fall sharply.This may happen again.And even if the stablecoin issuer does not fail to redeem its coins, doubts about whether it can be redeemed may still cause confusion.

Allison Nathan: The GENIUS Act only allows federal insurance banks to issue stablecoins, not bank entities must obtain special permission.Isn’t this a safeguard to prevent the blind spread of stablecoins?

Barry Eichengreen: That’s not enough.Various entities, including large tech companies and major retailers, may participate in stablecoin issuances, although they lack the expertise and protection mechanisms needed to manage such a significant financial instrument.

And I’m not sure that government agencies that might license hundreds of stablecoins can reliably regulate this novel and complex fintech.

If regulators fail to perform their duties, we will face many stablecoins with different face value in the worst case, and in the worst case, we will face crises that may damage the financial market and the overall economy.

Allison Nathan: Can giving stablecoin issuers permission to use the Fed’s main account solve these problems?

Barry Eichengreen: It is possible, but the GENIUS Act does not grant such permissions to issuers.

The loose regulatory measures set out in the bill, which only require a reserve of self-report and annual third-party audits, may not be able to ensure the perfection of the system.The loose regulatory measures set out in the bill, which only require a reserve of self-report and annual third-party audits, may not be able to ensure the perfection of the system.

Allison Nathan: Do you think there are any potential benefits for stablecoins?

Barry Eichengreen: In the context of the United States, I don’t think there is any benefit or there is no benefit.Stablecoins have the potential to bring some value to people without bank accounts by providing financial services.But only about 4% of Americans are unbanked, and these people face obstacles that make it unlikely to adopt digital assets.

For the vast majority of Americans, existing banking and payment systems are already quite efficient and reliable, providing very few incentives to convert to stablecoins.While stablecoins can reduce transaction costs by eliminating credit card exchange fees and allowing consumers not to accept artificial low bank interest rates, credit card companies and banks provide consumers with packages of services.Card companies offer fraud protection and payment deferral options, bank deposits are insured at the highest amount, and stablecoins don’t have these situations.Therefore, any potential savings are likely to be offset by the loss of these valuable protections and services.

Stablecoins may have more potential outside the U.S. with a large unbanked population, but they are far from the only solution to such problems.For example, India passed a law in 2005 requiring banks to provide unbanked people with no surcharge, no fees.Still, stablecoins may offer a more attractive advantage in cross-border payments, as transaction fees may be as high as 5-7%.In this case, cost savings may be proven to be of value to use.

Allison Nathan: Will stablecoins increase demand for Treasury bonds help alleviate the growing debt burden in the United States?

Barry Eichengreen: Stablecoins may provide marginal support for Treasury bond demand, but are likely to have limited overall impact on the market.The U.S. Treasury Department said that with the support of the law, the U.S. stablecoin market may increase to $2 trillion by the end of 2028, a small but significant proportion, accounting for a very small portion of the $30 trillion outstanding Treasury bonds.However, Escent’s prediction is likely to be too optimistic.

In addition, stablecoins may also intensify volatility in the Treasury bond market.In a crisis caused by the loss of confidence in stablecoin collateral, mass redemptions could force stablecoin issuers to sell treasury bonds quickly, causing bond prices to fall, interest rates to rise sharply, and could trigger more general financial market turmoil.

Allison Nathan: What does the popularity of stablecoins mean for the US dollar?

Barry Eichengreen: In the foreseeable future, stablecoins are unlikely to have any meaningful impact on the US dollar.The market value of stablecoins will be trivial compared to the daily trading volume of the forex market dominated by the US dollar.

While stablecoins can very limitedly complement other USD-denominated payment methods and provide another set of payment channels, I suspect they will replace the already well-established international interbank market, agency banking systems and SWIFT networks.

Meanwhile, these systems have used crypto technology similar to stablecoins to enhance their existing payment capabilities and support faster and cheaper transactions.Therefore, this provides less motivation for users to switch to stablecoins.

Allison Nathan: So, what are the potential impacts on the banking system?

Barry Eichengreen: Stablecoins are unlikely to challenge the traditional banking system, and there are two main reasons.

First, if stablecoins have broad demand as payment mechanisms, existing banks can respond by issuing their own currencies, which are likely to dominate the market given their size and existing customer networks.

Secondly, as we discussed, banks provide services that go far beyond payment convenience, but also FDIC-guaranteed deposits and preferential mortgage benefits for customers in the long term, which are difficult for stablecoin issuers to easily replicate.

So while stablecoins may offer some benefits, they are likely to fail to outperform banks in the competition.

Allison Nathan: Can central bank digital currency (CBDC) provide a better alternative to private stablecoins?

Barry Eichengreen: Digital currencies (CBDCs) are more promising because they do not threaten the singularity of currencies.

Unlike private stablecoins, there will be no doubt about the value of the CBDC issued by the Fed, just as commercial banks’ dollar deposits at the Fed are undoubtedly worth ⾜.Moreover, the Fed can fully support CBDC just as it supports deposits stored in the Fed, thereby reducing the risk of bank runs.

However, under the current US political environment, CBDC seems unlikely to be achieved.This distrust can be traced back to President Andrew Jackson’s 1830s when Congress was reluctant to hand over more power to the central bank.

The American public also holds these concerns.Therefore, while other countries are actively promoting CBDC as a solution to the world where digital currencies operate on blockchain, the United States has chosen to do it through stablecoins, which is not the best option.

Stablecoins: Impact on UST

William Sher and Bill Zhu assessed the impact of the expanding stablecoin trail on the U.S. Treasury market.

The Genius Act requires stablecoin issuers to maintain full reserve support for paying stablecoins, raising questions about the impact of the expansion of stablecoins on the Treasury market.

The popularity of stablecoins should lead to an increase in demand for secure assets, including Treasury bonds, although the ultimate impact will depend heavily on the timing and scale of the stablecoin adoption, the speed of the stablecoin circulation, transaction volume, and the source of the traditional channel outflow.

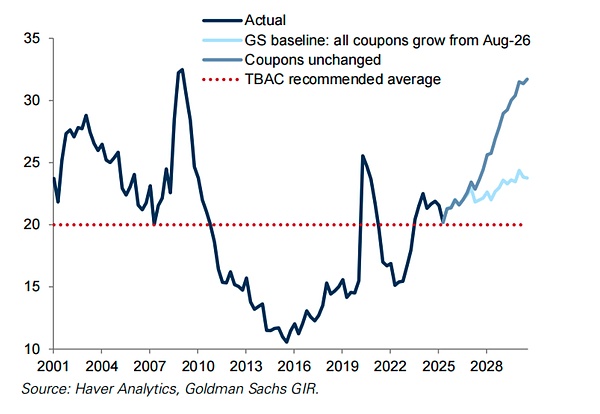

We expect the US Treasury Department to gradually increase the share of Treasury bills in the overall treasury issuance in the next year.

But we caution that excessive reliance on potentially volatile stablecoin demand for issuance decisions could complicate Treasury debt management and lead to higher maturity premiums over time.

The demand is all about the impact of the adoption of payment stablecoins on the demand for secure assets depends on its scope and speed, and the scope and speed of adoption are currently limited.

The use of stablecoins is still mainly limited to crypto asset transactions and is rarely used in consumer payments.Although adoption may increase as regulation and technology mature, the outlook remains highly uncertain.

In principle, stablecoins provide consumers with more potential incentives than traditional currencies, including through merchant rewards programs.However, similar offers already exist in gift card and credit card payments, which limits the values that motivate the pan-consumer adoption.However, a significant increase in the use of any stablecoin could lead to a significant increase in demand for secure assets.

The current stablecoin market size is approximately US$270 billion. The US dollar stablecoins in circulation dominated by two major issuers are calculated based on market value, unit: US$100 million.

Turnover speed will also affect the number of secure assets required to support the circulation of stablecoins.

For a given transaction volume level, faster turnover requires less stablecoin inventory and, accordingly, less demand for secure assets.By contrast, trading volume is lower and stablecoins require more reserves (i.e., safe assets).

Early evidence suggests that USDC trading volume is relatively low in total supply, meaning large reserves may be needed.However, as use cases turn to payments that are not related to cryptocurrency transactions, trading volumes can be reasonably expected to rise.

Finally, it is also crucial that the impact on the demand for secure assets depends on the source of funds on which stablecoins increase, in other words, the type of assets that users replace holding stablecoins and the composition of stablecoin reserves.

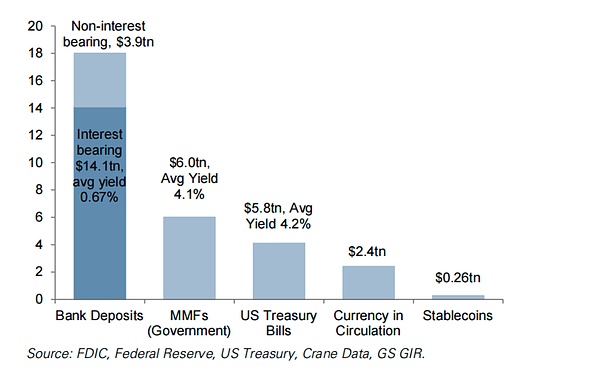

The inflow of payment stablecoins should mainly come from four traditional channels: money market funds (MMFs), bank deposits, physical cash, and external demand for US dollars.

The net impact of stablecoins adoption on demand for safe assets will mainly depend on the source of funds, the market value of stablecoins, current circulating safe assets and average yield, unit: trillions of dollars

The inflow of money market funds has the least impact on the demand for safe assets, because both money market funds and stablecoins are fully supported by safe assets (assuming it is a government money market fund, which represents more than 80% of the market).

While stablecoins and money market fund shares appear to be similar alternatives, both are not covered by deposit insurance, are fully supported by short-term assets, and can be tokenized, money market fund shares pay interest, while stablecoins are not paid.

This may limit how much demand the stablecoins can ultimately attract from money market funds, although stablecoin issuers can offer non-monetary rewards to incentivize adoption and partially compensate for yield disadvantages.

Since money market funds are already fully supported by secure assets, any funds flowing into stablecoins simply transfer the demand for secure assets from money market funds to stablecoin issuers, keeping the overall demand for secure assets unchanged.

However, demand preferences within the secure asset pool (e.g., Treasury bonds and repurchases) may differ between stablecoin issuers and money market funds, affecting the relative pricing of these assets.

Inflows from bank deposits may increase demand for safe assets, similar to shifting from deposits to money market funds.

While bank deposits can be tokenized, unlike stablecoins, they usually provide interest, are generally insured (up to $250,000), and importantly, they are not entirely backed by secure assets.

Incremental demand will depend on the size of deposit outflows and how banks manage their asset portfolios.In a frictionless world, deposits withdrawn by individuals to purchase stablecoins should eventually return to the banking system in the form of deposits or other sources of funds, with the net effect being to increase the security asset demand of stablecoin issuers.

But in scale, the characteristics of the bank’s fund may change, coupled with inter-bank heterogeneity (i.e., different levels of perceived liquidity and security), which may trigger adjustments if, for example, the overall cost of bank funds becomes more expensive.

If funds flowing to stablecoins cause the bank to sell secure assets, this will represent the transfer of ownership to the stablecoin issuer, and there is little incremental demand relative to the status quo.However, larger deposit migrations may have potential negative impacts on credit intermediaries.

Inflows from property currency holdings initially increase demand for secure assets due to instant conversion of currency flow to reserves (issued through stablecoin), although their last-term impact is unclear.

When the stablecoin issuer receives cash, subsequent funds flowing through the financial system should reduce currency circulation and increase reserves on the central bank’s balance sheet, similar to depositing cash into money market funds, thereby creating new demand for safe assets.

However, in the long run, the decline in demand for physical money will drive up reserves, which may lead to a shrinking balance sheet of the central bank. Whether it will affect the demand for additional safe assets depends on the extent of reserve loss.

However, it should be noted that the reduction in reserves may not be fully proportional to stablecoin migration, which may lead to a net increase in demand for safe assets in the past period.

Foreign investors seeking US dollar exposure could lead to a net increase in U.S. security assets demand.From a mechanism perspective, foreigners obtaining a US dollar stablecoin is similar to first conducting a foreign exchange transaction to purchase US dollars, and then conducting a US dollar transaction to purchase US dollar stablecoin (the issuer then purchases US dollar safe assets).This will increase the overall demand for USD secure assets to increase the number of stablecoin transactions.

But we are a little doubtful that given the potential capital flow restrictions, stablecoins can release a large amount of foreign capital that was previously untouchable, and they may also apply to dollar stablecoins if capital controls effectively limit the acquisition of traditional US dollars.

Potential changes in the supply structure of government bonds

⼴The general use of payment stablecoins may also affect the issuance decisions of the supply of secure assets.Increased demand for safe assets can be fulfilled by higher prices (lower short-term interest rates), increased front-end supply or both.

Early evidence suggests that commercial paper (CP) issuers have expanded their supply to meet demand driven by stablecoins, resulting in relatively little change in CP interest rates.

While other secure assets, including Treasury bonds, have limited evidence in this regard, the Ministry of Finance may also decide to satisfy the demand for secure assets powered by stablecoins by tilting the issuance to the short term.

This may reduce the expected cost of debt, but at the expense of greater volatility in the cost of capital in the business cycle.Therefore, any move towards such supply portfolio must weigh the potential risks of increased interest rate sensitivity financing demand and fiscal uncertainty (which may push up the maturity premium).

Our benchmark expectation is to increase the bill amount starting in August 2026, allowing a steady increase in bond share…

The share of government bonds in the total amount of issued government bonds is %

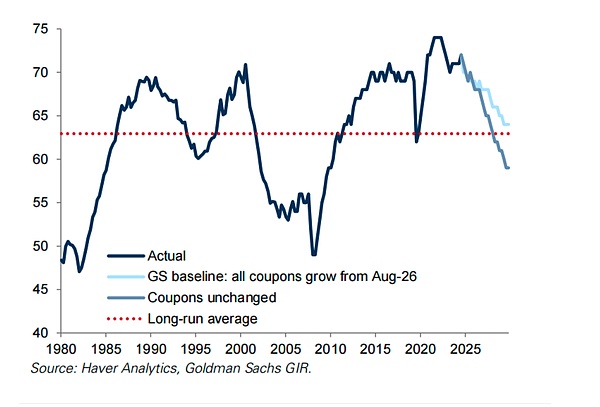

This will reduce the weighted average maturity of all outstanding U.S. debts

Average maturity date for outstanding tradable debts,

Making issuance decisions based on stablecoin-driven demand for secure assets has also strengthened the link between the public department’s borrowing costs and the private department’s demand for stablecoin liquidity.

This is different from the fiat currency system or the central bank digital currency, where central banks can smooth out liquidity demand in the private sector by adjusting liability costs without adjusting the asset side of the balance sheet.

If stablecoin demand is highly volatile, this link may be undesirable, potentially complicating Treasury debt management and leading to higher maturity premiums over time.

In summary, we expect the Treasury will allow the share of notes to rise in the coming years, but given the dangers and uncertainties surrounding the demand for ultimate stablecoin, we still think it is wise to take a controlled approach to this adjustment.

Stablecoin: Overview

What is a stablecoin?

Stablecoins are digital token currencies using blockchain technology, designed to maintain stable value, usually one-to-one pegs to traditional fiat currencies, most often the US dollar.This distinguishes stablecoins from Bitcoin and other cryptocurrencies, whose value is determined by the supply and demand of the currency.Their main purpose is to act as an intermediary for digital assets or payment settlements.

•Stablecoins maintain their fiat currency peg through market mechanism adjustments (algorithmic stablecoins) or issuers’ clear asset support.The latter is much larger in market value and is more integrated with the existing financial system because the issuer holds financial assets.

Issuers usually hold secure cash equivalents such as bank deposits, U.S. Treasury bonds, repurchase agreements and commercial paper, although some issuers also hold precious metals and cryptocurrencies.The GENIUS Act requires stablecoins to be fully supported after grace periods by “permitted reserves” (mainly secure assets such as USD and short-term Treasury bonds).

•The overall size of the stablecoin market is approximately US$268 billion, of which USDT (circulated about US$166 billion, issued by Tether) and USDC (circulated about US$68 billion, issued by Circle) occupy the vast majority of the market share.The remaining uncirculated stablecoins are scattered among many smaller issuers.

How to use stablecoins?

•Currently, stablecoins are mainly used in the cryptocurrency ecosystem for trading, providing a stable asset to enter and exit positions without the need to be converted to fiat currency.

• Another major purpose is to provide USD access outside the USD, especially in areas that are prone to depreciation, as well as for cross-border payments and remittances.

• Stablecoins can also be used for consumer payments, but as of now, this use is still limited because consumers still rely on traditional payment systems.

•Inter-business payment (B2B) may be another application scenario for stablecoins, although inter-business payments have historically been very slow to adopt new payment channels.

How do stablecoins work?

1. The customer deposits the underlying assets to the stablecoin issuer, usually in US dollars. In return, the issuer mints an equivalent stablecoin on the blockchain and delivers it to the customer.The dollar cash received by the issuer is deposited in so-called reserve funds, which are usually high-quality liquid assets, such as U.S. Treasury bonds.Stablecoins can also be traded in the Ⅴ-level market, and their prices will fluctuate with the supply and demand relationship.

2. Stablecoins are usually stored in cryptocurrency wallets.These wallets hold stablecoins as digital assets on the blockchain—the blockchain records who owns the coin and any transactions they make, allowing users to send, receive and manage their stablecoins.

3. Customers can trade in stablecoins in various ways.When a customer initiates a transaction, they send a request to the blockchain network that includes the recipient’s wallet address and the number of stablecoins to be transferred.Transactions are verified and recorded on the blockchain.The transaction is then reflected in the recipient’s wallet balance.

4. When users want to exchange stablecoins for underlying assets, they will return the stablecoins to the issuer.The issuer then destroys the stablecoin, removes it from circulation, and returns the reserve assets of equivalent value to the customer.

Stable currency market size

The current stablecoin market size is approximately US$270 billion, mainly dominated by two major issuers, Tether and Circle.

The US dollar stablecoins in circulation are divided by market value, unit: US$100 million

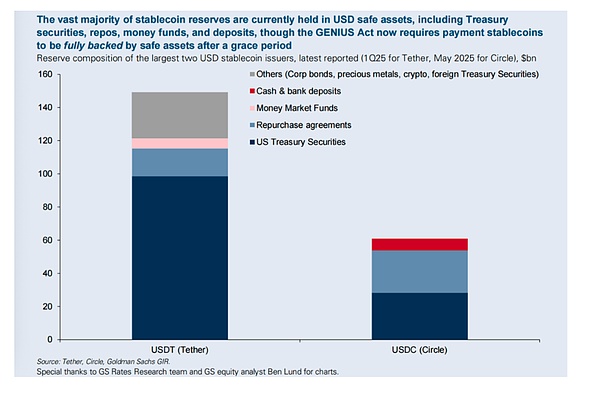

Currently the vast majority of stablecoins reserves are held in safe dollar assets, including Treasury bonds, repurchases, money funds and deposits, although the GENIUS Act now requires that payment of stablecoins must be fully supported by secure assets after the grace period.

The reserve composition of the largest two US dollar stablecoin issuers, latest report (Tether is the first quarter of 2025, Circle is the May 2025), $bn

Stablecoin: Business Opportunities

James Yaro discussed the business model and opportunities of stablecoin issuers.

As stablecoins adoption rates rise and regulatory environment improves, interest in stablecoins has surged, which raises questions about business opportunities for stablecoins issuers.

Although business models vary, fiat-backed stablecoin issuers have value pegged to fiat currency, usually in the US dollar, generating income mainly by earning interest on their reserve assets.

We believe that as real-world assets are tokenized, business opportunities for stablecoin issuers may increase.

Business Model: Guide

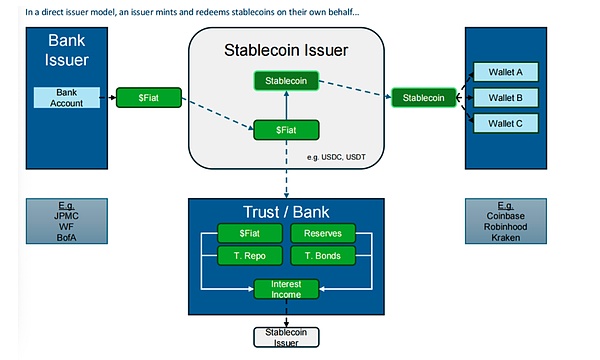

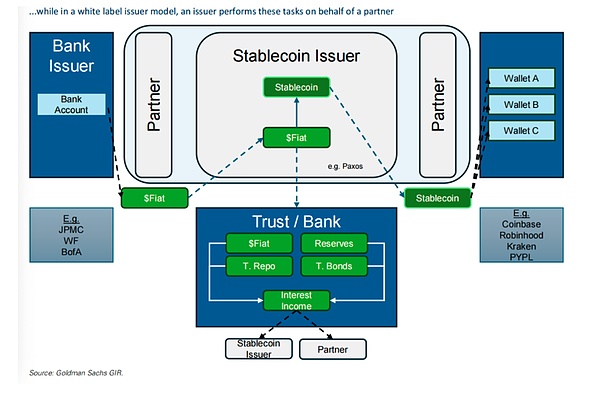

Stablecoin issuers adopt two main business models: (1) direct issuance and creation of stablecoins, and (2) “white-label” stablecoins.

In the direct issuance mode, the issuer “mints” its own stablecoins.

Minting is the process of creating new coins.The customer delivers the US dollar to the issuer, who then creates a stablecoin of equal value and delivers it to the customer.

The minting proceeds are invested in high-quality liquid assets, which for certain stablecoins have no credit, market or interest rate risks.

These assets, or reserves, are usually composed of a mixture of U.S. Treasury bonds, U.S. Treasury bond repurchases and bank deposits, which are usually important banks in the global system.

The high quality of these reserves means stablecoin issuers can easily cash them in order to provide US dollars to customers who want to sell their stablecoins, a process known as “redemption.”

Tether (issuance of USDT) and Circle are two direct stablecoins issuers, with market capitalizations of approximately $166 billion and approximately $68 billion respectively, accounting for the vast majority of the total market capitalization of USD stablecoins approximately $268 billion.

In the white-label stablecoin issuance model, the issuer mints and redeems stablecoins on behalf of the partner, and the partner delivers its client’s USD to the issuer for minting and delivers the newly minted stablecoins to the client.

The reserve structure and composition under this issuance model are similar to the direct issuance model.

The largest market player in the ume-label stablecoins is Paxos, whose usage has recently risen due to its global dollar stablecoin (USDG) expansion in several partners including Robinhood and Kraken, which issues PayPalCoin (PYUSD) and USDG on behalf of the global dollar network.

Make Money: Everything About Interest

One of the main ways stablecoin issuers make money is to get more returns through their assets than they pay to their business partners.The issuer collects interest reserve fund income (“reserve fund income”).

The recently entered into force GENIUS Act does not allow issuers to pay interest directly to token holders, because the purpose of stablecoins is to be used for payment.

However, stablecoin issuers can and often pay part of the reserve fund income to partners as distribution fees, which can then choose to allocate rewards to customers, which have similarities to interest.Circle pays allocation fees through its commercial contract Coinbase, which offers rewards to USDC holders on its platform.

Different stablecoins have different models, i.e. how much reserve money they pay to partners to incentivize usage or pay rewards.Some, such as Paxos’ USDG, pay almost all reserve income to partners, deducting a small part of the management fee retained by Paxos.

Others, such as USDT, retain all reserve income.Circle’s USDC is somewhere in between, with approximately 60% of reserve fund income allocated to partners in 2024.

Use case: Tokenization opportunity

Currently, stablecoins are mainly used as a means to allow people to obtain US dollars for trading outside the United States and within the crypto ecosystem.

Tokenization based on real-world assets, that is, physical or digital assets whose rights are converted into digital tokens on the blockchain, are currently small in market size, with a total market value of approximately US$295 billion and US$27 billion after excluding stablecoins, making it the largest tokenized asset at present.

However, more real-world assets can be tokenized, which will enhance the application scenarios of stablecoins.

This tokenization is especially beneficial for assets that are difficult to track and involve cumbersome and expensive settlement processes, such as residential mortgages (the US market size is about $13 trillion), which involve time-consuming assessment processes, expensive property insurance, and ultimately require offline signing of closure documents. The latter two are particularly likely to achieve more efficient and low-cost processes on the blockchain.

This asset tokenization has begun.Robinhood and private cryptocurrency exchange Kraken recently began offering tokenized stocks with the goal of opening up new markets for the product (i.e., trading in US stocks to European investors), trading around the clock (not possible under traditional stock trading rules), and providing access in areas with a lack of a sound brokerage market (in theory anyone with a smartphone can buy digital assets).Moreover, the more tokenized assets, the more useful the stablecoins are, because they are the natural way to pay real-world assets on the blockchain.

In the direct issuer model, issuers mint and redeem stablecoins on their own…

In the white-mark issuer model, the issuer performs these tasks on behalf of the partners

Q&A: The impact of stablecoins on payments

Nance Will answers key questions about the disruptive potential of stablecoins to traditional payment channels.

As the passage of the GENIUS bill opened up a more popular path for stablecoins, a debate over the possibility of this disruptiveness emerged.

We explored the key issues and concluded that even if stablecoins are adopted more generally, traditional payment companies may still play an important role in distribution, fraud prevention, and regulatory compliance.

Q: With the remittance company under the gun of stablecoin subversion, can stablecoins destroy existing cross-border payment channels?

A: We think the risk to the remittance company is exaggerated.We hardly see where the cost of stablecoin payment is essentially lower than traditional remittance payments, because the cost in the remittance area is mostly up/downhill costs, regulatory licensing, and account opening/KYC/compliance related costs, and stablecoins do not directly solve these problems.

To assess potential cost savings for stablecoins, investors should compare item by item on each individual channel (i.e. the specific path through which funds are transferred from one country to another) and include up/downhill costs, foreign exchange conversion fees, KYC and AML costs, as well as fraud and fraud prevention costs, which significantly increase the surface costs of blockchain transactions.

In situations where certain highest cost corridors are often associated with lower liquidity money markets and higher settlement costs, cost savings may occur if stablecoins can intervene and increase financial infrastructure and increase liquidity of these currencies.

But such galleries do not represent the main part of remittances, and government regulation may limit the size of stablecoin-based payments in these regions.

Without the general dollarization, or unless the global economy moves toward blockchain completely “on chain”, stablecoin-based remittances may incur similar transaction costs as traditional remittances, resulting in little or no savings from consumers.

However, we do see opportunities to use stablecoins for 24/7 settlements that can improve the working capital efficiency of remittance companies, thereby reducing the need for advance payments for weekend events.

Q: How do consumer payment companies deal with the risks/opportunities brought by stablecoins?

A: A often underestimated fact is that Visa and Mastercard already play an important role in facilitating payments and transactions.

For stablecoins, it will be based on its early partnership with Coinbase to facilitate payment settlements based on cryptocurrencies.

Visa expects to settle more than US$1 billion in stablecoin transaction volumes within the next 12-18 months.

As with any new payment method, stablecoins are unlikely to scale without a distribution network.For general acceptance, significant distribution barriers may limit consumption of stablecoin-based payments in emerging markets where card payments have not yet taken root in economic development.Given that the global card ecosystem is strengthened by significant network effects, we believe that existing consumers face limited risks.

Q: What aspects of the potential impact of stablecoins on traditional payments have investors underestimated?

A: We think the most common misunderstanding is the perception of the huge cost advantage compared to traditional cross-border payments.

In our view, stablecoins are an incomplete medium of cross-border payments and still require most of the onshore and offshore infrastructure.They are equally susceptible to fraud and still require permission and compliance with local government regulations.

We believe this is a more general misunderstanding in the payment field: the value of most payment companies is not in actual money flow, but in large-scale coordination of payments in a compliant manner, while minimizing fraud costs and achieving efficient, user-friendly distribution.

Although stablecoins are a payment channel, we believe they operate at the payment infrastructure level, side by side with the domestic ACH system.

Central bank channels (i.e. SWIFT/agent banking) operate in cross-border businesses, while most payment companies operate at the service level, where transaction monetization is associated with value-added services on the underlying transaction.

Q: What does it seem to be the most unreasonable in the payment field? Who is in the best/worst position in a world where stablecoins are more popular?

A: We believe that digital priority remittance providers that are less involved in the mysterious channels of instability and/or non-liquid currencies are the most advantageous companies in this field.Service providers capable of integrating stablecoins into their networks are also relatively in a favorable position.

The most disadvantaged companies are traditional remittance service providers, which have significant exposure to cash-intensive channels.However, the popularity of stablecoins may provide an opportunity if the adoption of stablecoins in these channels can reduce transaction costs and working capital needs.

Q: Will stablecoins reduce bank deposits?

A: If a customer transfers deposits to a stablecoin, the increase in the stablecoin may have a significant impact on the bank’s deposit base.

However, we believe that any major transfer requires stablecoins to provide better economics than traditional deposits or lower payment frictions for goods and services, both of which may be difficult to achieve in the short and medium term.

Furthermore, we believe that banks plan and have begun integrating stablecoins and other blockchain products into their infrastructure, which may increase efficiency over time.

Four prerequisites for deposit transfer:

1. The interest (or equivalent) paid by the stablecoin must be significantly higher than the bank deposit rate.

2. Stablecoins must provide a more efficient payment mechanism.

3. Stablecoins must provide customers with similar guarantees as bank deposits.

4. Regulators and policy makers must believe that the transfer of bank deposits to stablecoins will lead to more diversification and competition in non-bank lending options.

This may be difficult to achieve.

We see challenges in achieving these prerequisites.

Under the GENIUS Act, stablecoin issuers do not allow interest payments on stablecoins.

While issuers can earn revenue from Circle through partners (e.g., Coinbase (COIN), and in turn provide rewards for USDC customers), interest bans limit their ability to compete with banks, which have greater flexibility in interest rates paid to depositors and can remain competitive by increasing interest rates.

While this is not good for profit margins, it reduces customers’ motivation to move deposits out of the banking system.

Therefore, both market practices and laws need to undergo significant changes in order for stablecoins to provide better economics relative to bank deposits.

Stablecoins may also need to obtain greater utility than current use cases (i.e., in the cryptocurrency space and providing US dollar funds to non-U.S. customers) so that depositors can give up deposit interest (at least for interest-bearing deposits, which accounts for approximately 80% of all deposits).

The fact that banks provide FDIC deposit insurance protection while stablecoins are not insured may also set a high threshold for insured deposits to move from the banking system to stablecoins.

If banks lose large amounts of operating deposits (which are often lower in cost), consumers’ borrowing costs may rise as banks try to cover higher funding costs by raising loan rates, which may cause negative views from policy makers.

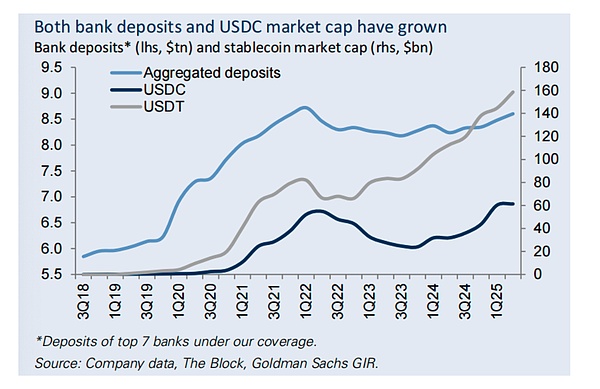

Bank deposits and USDC market value both increased

Bank deposits* (left, trillion US dollars) and stablecoin market capitalization (right, trillion US dollars)

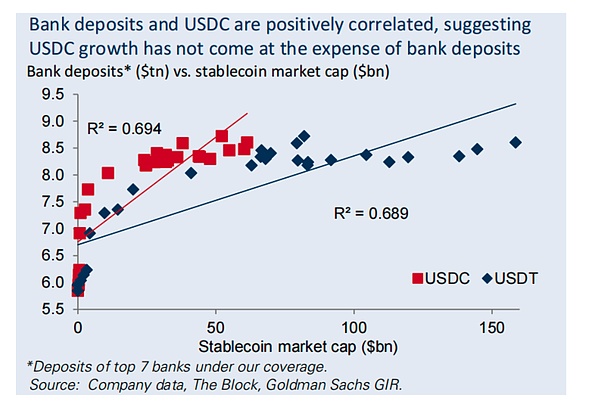

Bank deposits and USDC are positively correlated, indicating that USDC increases are not at the cost of bank deposits.

Bank deposits* (trillion dollars) vs. stablecoin market value (gigabit dollars)

Tokenization may change the landscape

We believe that the most obvious case of stablecoins replacing banks will be the pan-tokenization of the US economy.In a tokenized economy, goods and services will all be interchangeable on the blockchain, and a tokenized asset (for example, tokenized stocks, bonds or houses) can be exchanged for tokenized US dollars (i.e. stablecoins).

In such a world, stablecoins will become an important means of payment, leading to a significant shift from bank deposits to stablecoins.However, tokenized assets have been very few so far, and other digital payment methods may appear (for example, tokenized money market funds recently launched by some financial institutions, and their own digital currencies provided by banks) to compete with stablecoins, thereby limiting the impact on bank deposits.

Finally, banks are focusing on accelerating the integration of stablecoins and blockchain technologies into their infrastructure, which can improve efficiency, provide a better customer experience through faster settlements, and potentially reduce costs.

Banks have begun to integrate payment and blockchain technology.For example, JPMorgan Chase recently announced that it will offer tokenized deposit tokens to institutional clients, which will become an alternative to holding stablecoins over time.

JPMorgan and COIN also announced a partnership to connect JPMorgan’s deposit account with COIN wallet, transfer JPMorgan’s credit card points to COIN, and allow the use of JPMorgan’s credit card on COIN.We expect the banking industry to announce more collaborations and blockchain products over time.

Stablecoins and central bank digital currency

Bill Zhu discussed the considerations of payment stablecoins and central bank digital currencies in financial system design and stability.

The recent US law has opened up the largest adoption of stablecoins, but at the same time, at least currently shutting down the central bank digital currency (CBDC).But many other countries are still exploring CBDC as the world increasingly turns to digital currencies.Below, we discuss the considerations of payment stablecoins and CBDCs in financial system design and financial stability.

Private and Public

Stablecoins and central bank digital currencies are both digital token forms that utilize blockchain technology.They share many things in common, including faster and cheaper transactions, potential replacement of physical currencies, and implicit support provided by secure assets.However, stablecoins are issued by private institutions and operate on decentralized systems, while central bank digital currencies are issued and controlled by a single entity, central bank.

Transfer of seigniorage

Since stablecoins are issued by private institutions rather than central banks, this means private issuers are able to capture the seigniorage tax, i.e. the difference between the currency’s parity value and its production cost, which has historically been a source of revenue for central banks.

Stablecoin issuers may share seigniorage with merchants through operational efficiency and share with end users through rewards paid to end users by business partners.By contrast, central bank digital currencies will keep seigniorage at the central bank.

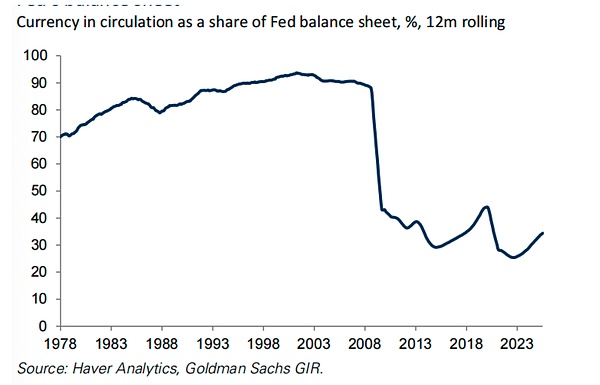

In the past year, the proportion of circulating currencies in the Federal Reserve’s balance sheet has declined.

The proportion of circulating currencies to the Federal Reserve’s balance sheet (%), 12 rolling

If stablecoins weaken the demand for physical currencies, the transfer of seigniorship to the private sector means that a larger proportion of central bank liabilities will become interest-bearing liabilities, which will increase the total interest expenditure of the public sector relative to the central bank’s digital currency framework.

The shift from physical currencies to stablecoins may allow central banks to run smaller balance sheets over time while maintaining their ideal reserves level.

The singleness of currency

A major advantage of traditional currencies as mediums of exchange is that they can solve the problem of “double coincidence”

Though unlike physical cash, central bank digital currency maintains this characteristic to a large extent because it is issued by a single entity, central bank.

Some believe that stablecoins involving multiple issuers and currencies may weaken the currency’s singularity (Part 6-7) and slow down the adoption process.

If there is uncertainty about the issuer’s financial situation, having multiple private currency issuers can also bring financial stability risks.But others are comforted by the fact that all stablecoins will receive full support from the same risk-free assets.

Safe Asset Volatility

Stablecoin issuers buy reserve assets when creating tokens, and sell reserve assets when redeeming them.

This process has the potential to amplify price fluctuations in reserve assets, especially during periods of low liquidity or unbalanced supply and demand.Empirical research shows that the flow of stablecoins can create price pressure in the treasury bill market, where the impact of redemption is greater than creation.

By contrast, the creation and redemption of central bank digital currencies will only change the composition of central bank liabilities (e.g., from digital currencies to currency or reserves) without affecting central bank asset holdings, so it is unlikely to amplify price fluctuations in secure assets.

Financial stability considerations

Bank deposits rely on fewer safe assets than stablecoins.If the attractiveness of stablecoins to deposits is large enough at the system level, this may reshape the asset and fund structure of the banking department, thereby affecting credit provision and financial stability.

If stablecoins are to compete with low-cost deposits, it could put pressure on banks, forcing them to compete on prices or increase their reliance on more expensive, non-deposit sources of funds.Over time, this may increase the overall cost of credit intermediaries across the economy.

Interbank heterogeneity is also an important consideration.If the liquidity distribution between banks is uneven and deposits are outflowing in large quantities from banks with strict liquidity constraints, it may lead to intensifying internal redistribution frictions within the banking system, similar to the risk of bank runs from banks to money market funds.

These risks are greater for banks with a concentrated or prone to churn (e.g., banks with higher corporate deposits than retail deposits), and when people think that deposits have small returns relative to stablecoins.

While it is not clear whether the existence of stablecoins will amplify this risk more significantly than money market funds, it remains another source of friction and disturbances to overall banking activity.

While these considerations are equally applicable under the Central Bank Digital Currency (CBDC) framework, policy makers can reduce these risks by designing CBDCs, for example, the goal is to replace cash demand rather than deposit demand (as in China).The central bank also has the ability to make up for lost deposit funds by lending directly to banks, although this may mean that the central bank will have to bear some credit risks.

The Genius Act: Overview

what is it?

The GENIUS Act is a US stablecoin law proposed by Senators Hagerty (R-TN), Scott (R-SC), Gillibrand (D-NY) and Rums (RWY).

The bill provides a regulatory framework for payment of stablecoins, defining it as a digital asset designed to be used as a payment or settlement method.

The bill was signed into law by President Trump on July 18, and was previously passed in the Senate with a vote of 68 and 30 against it on June 17, and in the House of Representatives with a vote of 308 and 122 against it on July 17.

Two other cryptocurrency bills passed in the House together with the bill: the Digital Assets Market Clear Act (also known as the CLARITY Act), which will provide a regulatory framework for a wider digital asset, and the anti-Central Bank Digital Currency Monitoring National Act, aiming to prevent the Fed from issuing Central Bank Digital Currency (CBDC) directly to individuals without explicit authorization from Congress.The two bills are now under consideration in the Senate.

What is the role of the Genius Act?

Define stablecoin issuers.Stable coins can be issued by insured depository subsidiaries, or by federally licensed non-bank entities specially licensed by the Comptroller of Currency 5 (OCC), and state licensed issuers, subject to the issuance of their volumes to less than $10 billion.

As a result, banks will be allowed to issue their own stablecoins, while non-financial companies will be restricted unless they meet certain standards (those standards have not yet been established).

Establish a framework for regulatory reserves.Issuers must maintain stablecoins support reserves at least 1:1.Reserves must consist of US dollars, current deposits held by depositors, treasury bills, notes or bonds with a term of 93 days or less, repurchase or reverse repurchase agreements with a term of 7 days or less, money market funds or central bank reserve deposits.

Develop a reserve audit framework.Stablecoin issuers must disclose their reserve composition on their website every week, while issuers who issue outstanding stablecoins over $50 billion must publicly disclose annual financial statements, which must be audited by a certified public accounting firm.

Payment of interest is prohibited.Stablecoin issuers prohibit paying interest to token holders.However, the bill does not mention whether a third party or affiliate can pay interest, and the issuer can distribute reserve revenue to the affiliates, and the affiliates can provide rewards to stablecoin holders on their platform.(Example: Circle can pay reserve revenue to Coinbase, which can offer rewards to USDC holders on its platform).

Establish compliance requirements.Issuers must comply with bank confidentiality laws, anti-money laundering compliance requirements and sanctions requirements.They also have to conduct transaction monitoring, recordkeeping and suspicious activity reporting.

Access to the Fed’s main account remains in progress.The bill does not change the current elections for those who are legally eligible for Federal Reserve services or deposit access.