Author: Tanay Ved, CoinMetrics analyst; Compiler: Shaw Bitcoin Vision

Key takeaways

-

Ethena’s USDe has quickly grown to become the third largest stablecoin, characterized as a yield-generating synthetic dollar backed by crypto collateral and delta-neutral hedging futures contracts (rather than fiat reserves).

-

Staking USDe (sUSDe) earns revenue from perpetual funding rates, Ethereum staking rewards, and liquid stablecoins, with returns tied to exchange funding dynamics and on-chain earnings.

-

USDe is primarily used as a savings and income instrument.Its integration with DeFi protocols like Aave and Pendle improves funding efficiency and composability while tying stability to on-chain leverage.

-

Market stress events such as the Bybit hack and the October Flash Crash tested Ethena’s design and risk management, highlighting how funding, exchange, pricing and liquidity dynamics affect the stability of synthetic dollars such as USDe.

The Rise of Ethena’s Synthetic Dollar USDe

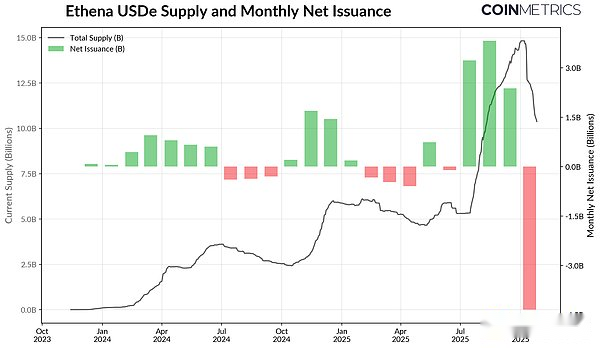

Ethena’s USDe was born in 2024 and quickly jumped to the third largest stablecoin in market value.At present, the market value of USDe has exceeded 10.5 billion US dollars, and it has become a strong competitor and differentiated choice that poses a threat to the long-term dominance of USDT and USDC.USDe’s appeal stems from its unique design: a yield-generating “synthetic dollar” that is not backed by cash or Treasury bonds, but by delta-neutral hedging strategies in cryptoassets and perpetual contract markets.

Source: Coin Metrics Network Data Pro

However, these characteristics also make it the focus of discussions about cryptocurrency systemic risk, with people often comparing it to Terra’s UST’s death spiral.Although fundamentally different from UST’s algorithmic design, the Bybit hack in early 2025 and the market flash crash on October 11 highlighted the vulnerability that synthetic dollars such as USDe can face during times of market stress.

This rapid rise, coupled with recent market volatility, provides an opportunity to examine how the Ethena synthetic dollar system works in practice.In this issue of the CoinMetrics Network State Report, we will analyze in detail:

-

How USDe and its staking yield version sUSDe work

-

Ethena’s support mechanism and revenue generation principle

-

USDe and sUSDe usage in exchanges and decentralized finance (DeFi)

-

Risks of synthetic stablecoins revealed by recent volatility

Support, Stability and Revenue Sources

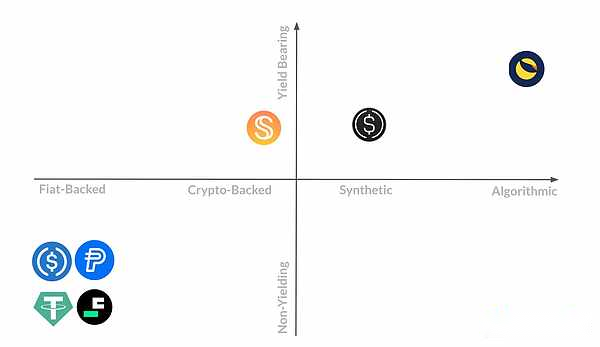

Positioning Ethena USDe on the stablecoin support and earnings spectrum

Unlike stablecoins such as USDT or USDC, which are collateralized by cash and short-term U.S. Treasury bonds, USDe is not based on traditional reserves but is backed by hedging strategies in cryptoassets and futures markets.Ethena tokenizes this approach, known as “spot arbitrage trading” or “delta neutral strategies,” to maintain a synthetic USD peg.In fact, every dollar of USDe minted is based on two opposite contract positions held by the protocol:

-

Long contracts of spot crypto assets are held at over-the-counter custodians as collateral (mainly BTC, ETH or pledged ETH).

-

Hold equal and opposite short contracts in the perpetual futures market on exchanges like Binance, Bybit, and OKX.

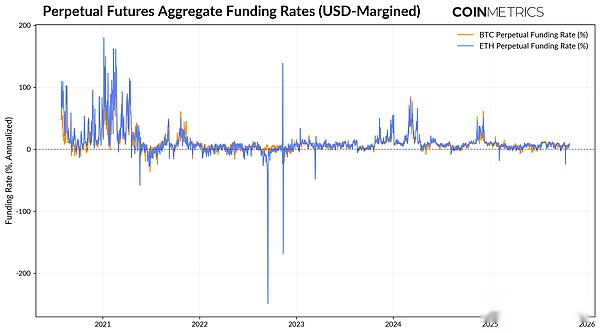

This combination allows Ethena’s exposure to remain market neutral while still generating revenue from perpetual futures funding rates.Simply put, perpetual futures are derivatives that allow hedging or speculation on cryptoassets, similar to traditional futures contracts, but without an expiry date.In order to keep the price close to the spot price of the underlying asset, the exchange implements funding fee payments, which are fees for regular trades between long and short traders.When the funding rate is positive, short contracts will earn a profit, allowing Ethena to pass this profit on to sUSDe holders.

Source: Coin Metrics Market Data Pro

As shown in the chart above, the futures funding rates for BTC and ETH have been positive during the bull market, with annualized rates averaging around 11% in 2024 and around 5% in 2025.Consistently high rates suggest the market is paying to be long, allowing Ethena to capture this spread with its delta neutral strategy.However, during periods of market stress, such as the Luna and 3AC incidents, the FTX crash in November 2022, and the flash crash in October 2025, funding rates have turned negative, which has posed a severe test to the stability and revenue generation capabilities of the protocol.

Where does the revenue come from?

While the perpetual contract’s funding rate is Ethena’s primary source of revenue, the protocol also supplements this revenue with two additional revenue streams:

-

Perpetual futures funding rate: The income generated by the price difference between long spot and short futures.

-

Pledge income: ETH staking income obtained from the Ethereum consensus layer and execution layer.

-

Interest on Liquid Stablecoins: Coinbase’s USDC fixed rate, or income from short-term U.S. Treasury investment through BlackRock’s BUIDL fund.

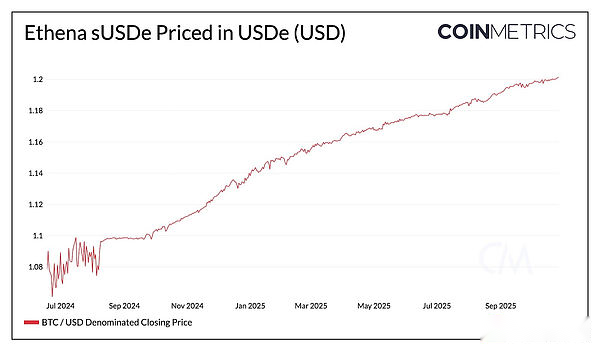

Revenue generated from these sources will be distributed to holders of staked USDe (sUSDe).sUSDe automatically accumulates earnings through the ERC-4626 vault standard, and its value will exceed USDe.The growth in Ethena’s synthetic dollar supply and earnings is therefore driven by the interplay of these earnings sources, enhancing its appeal in a bull market.

Source: Coin Metrics Network Data Pro

Ethena Reserve Fund

To manage risk in adverse circumstances, Ethena has established a reserve fund that serves as an insurance buffer against negative funding rates or unexpected losses.When the funding rate is high, the protocol prefers a delta-neutral strategy; when the funding rate is low, it turns to holding stablecoins to maintain support and provide benchmark treasury bond interest rates.

The assets in the reserve fund are held by this contract and consist of liquid stablecoins (currently $41.8 million in USDtb, an Ethena stablecoin backed by BlackRock’s BUIDL tokenized Treasury bonds).

Ethena’s USDe and sUSDe usage

After understanding the underlying operating mechanism of Ethena, understanding the usage scenarios and methods of its assets (USDe and sUSDe) will help understand its unique uses and risk profile.Unlike stablecoins such as USDT or USDC, which are used for transactions and more frequently for payments or settlements, USDe is a savings and income instrument rather than a medium of exchange.

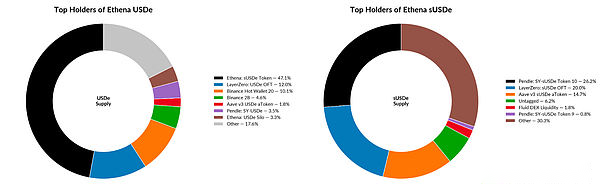

Source: Coin Metrics ATLAS

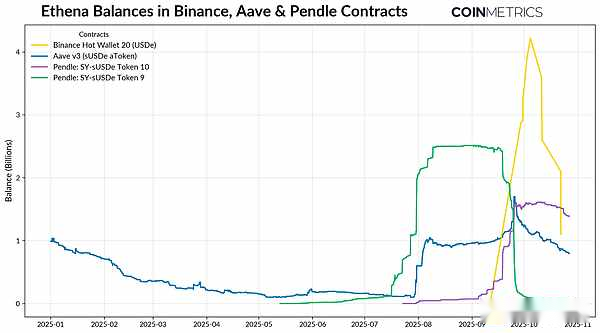

Looking at the snapshot of the account balances of each major holder in the table above (as of October 2025), we find that approximately half ($5.1 billion) of the USDe supply is pledged to obtain yield-generating sUSDe.About 13% ($1.3 billion) of USDe is located in LayerZero’s OFT bridge, used to facilitate cross-chain liquidity; while two Binance wallets hold about 14% of the USDe supply.Since Binance integrated USDe as a margin-collateralized asset for futures trading and Binance Earn in September, more than $4 billion in USDe has rapidly flowed into Binance.But soon, as USDe became unanchored on Binance, the price fell to $0.67, resulting in an outflow of $2.9 billion.

Source: Coin Metrics ATLAS

On the other hand, the majority of sUSDe’s supply exists within DeFi protocols.Aave (lending) and Pendle (yield tokenization) combined account for more than a third of all circulating sUSDe, as users use the token for collateralized lending and on-chain yield strategies.This creates a “yield amplification” cycle where users stake USDe to mint sUSDe, which is deposited into Pendle and tokenized, and then reused as collateral for Aave, increasing capital efficiency and composability while also creating a deeper connection to on-chain leverage and liquidity dynamics.

Risks and Reflexivity of Synthetic Dollars

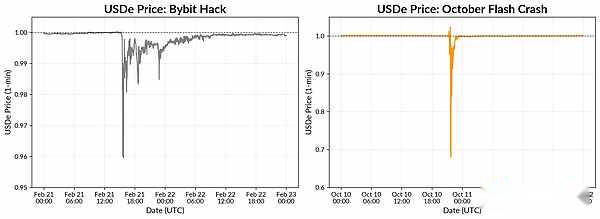

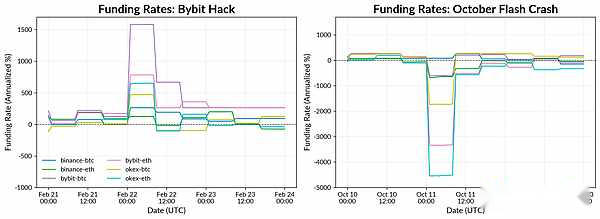

The market stress event in 2025 allows us to observe the performance of the Ethena synthetic dollar system under market fluctuations from a realistic perspective.We can observe this through the Bybit hack in February and the flash crash on October 11, both of which occurred over the weekend when traditional markets were suspended from trading.

Source: Coin Metrics Reference Rates

Despite the disruption, funding rates across major trading platforms have remained positive, allowing Ethena’s short futures positions to continue to generate revenue and provide a buffer for the protocol along with its reserve fund.The incident highlights exchange and custody risks: While Ethena’s collateral in custody over-the-counter remains safe, protecting it from the possible bankruptcy of Bybit, the incident also highlights the importance of diversifying trading and custody platforms and reducing single points of failure.

Source: Coin Metrics Market Data Pro

The October 11 flash crash brought about a more dramatic but shorter-lasting decoupling.On Binance, USDe fell to about $0.65 as liquidity depletion, serial liquidations, and the automatic deleveraging mechanism (ADL) exacerbated the price decline.Funding rates across trading platforms have turned sharply negative, but this decoupling remains localized due to sparse order books and pricing differences between centralized exchanges and DeFi platforms.The incident highlights the sensitivity of the USDe peg to platform-specific liquidity conditions, as well as the challenges of maintaining price consistency in interconnected markets.

While Ethena remains resilient and continues to operate, these events shed light on the dynamics and risks of synthetic dollars such as USDe.Negative funding rates could put pressure on protocol revenue and test reserves, while exchange outages highlight the importance of diversity in trading venues and liquidity conditions.OTC custody protects collateral, but pricing and arbitrage still rely on functioning markets.As Ethena’s assets become increasingly integrated within the DeFi space, its stability increasingly reflects broader leverage and liquidity cycles, tightly tying its growth and resilience to the health of centralized and on-chain markets.