On November 5, 2025, the U.S. federal government shutdown entered its 35th day, tying the longest record in history.The impasse stems from differences between congressional Republicans and Democrats on the budget bill. The Democrats demanded an extension of Affordable Care Act subsidies, while the Republicans refused to give in. This led to the Senate rejecting temporary appropriations bills passed by the House of Representatives 14 times.During the shutdown, taxes were collected as usual, but federal spending was significantly frozen, about 700,000 employees were on unpaid leave, airport security delays affected a total of 3.2 million passengers, the Food Assistance Program (SNAP) only paid 50% of benefits, and the Head Start children’s program was partially closed.The economic impact is already being felt: The Congressional Budget Office estimates that GDP losses are about $1.4 billion per week.If the shutdown continues, the liquidity crisis will become the biggest hidden danger.

The “pipeline” of the financial system has shown signs of tension

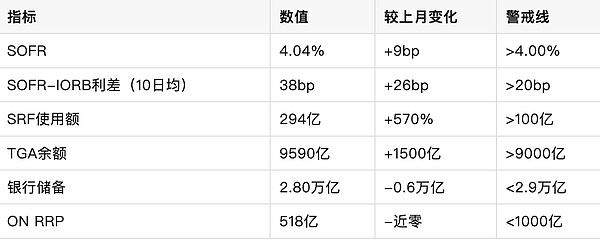

The U.S. financial system’s short-term funding markets rely on approximately $3 trillion in overnight repurchase (repo) transactions.These transactions are collateralized by Treasury bonds, with banks, money market funds (MMFs) and primary dealers lending dollars to each other on a daily basis to ensure smooth payment settlement.The core indicator isSecured Overnight Financing Rate (SOFR), which reflects the actual cost of borrowing.On November 3, 2025, SOFR reported 4.04%, which is 4 basis points higher than the Federal Reserve’s interest on reserve balances (IORB, upper limit of 4.00%). It has exceeded the upper limit for six consecutive days, and the 10-day moving average spread reached 38 basis points.

The Fed does not set a single interest rate, but sets a corridor: the lower limit is the ON RRP interest rate (4.00%), and the upper limit is the IORB and Standing Repurchase Facility (SRF) interest rate (4.25%).Under normal circumstances, SOFR should fluctuate below the upper limit.However, since September 2025, SOFR has repeatedly exceeded the upper limit. On October 31, the single-day SRF usage hit a record of 50.35 billion U.S. dollars, and on November 3, it reached another 29.4 billion U.S. dollars. This shows that the private market is unwilling to lend, and institutions are forced to seek assistance from the Federal Reserve.

The unsecured end is also under pressure.The federal funds rate (EFFR) trades at an average daily price of $8-9 billion, with the October moving average 12 basis points higher than the ON RRP.Logan, president of the Dallas branch of the Federal Reserve, warned on October 31: “If the recent increase in the repo rate is not temporary, the Federal Reserve needs to initiate asset purchases (QE).” Chairman Powell also named “tight pipelines” in his speech in November.

The Treasury General Account (TGA) has become a liquidity “black hole”

TGA is the Treasury’s “checking account” with the Federal Reserve.In a normal year, the TGA’s target balance is US$850 billion, and tax revenues are quickly disbursed after inflows, forming a supplement to bank reserves.Before the shutdown in 2025, the Finance Minister has filled the TGA from 300 billion to 850 billion, exhausting the ON RRP buffer (only 15 billion is left).After the shutdown, tens of billions of tax revenue continued to flow in on an average daily basis, but expenditures almost fell to zero, causing TGA to soar to US$959 billion (weekly average on October 29), a surge of 150 billion from before the shutdown.

For every $1 of TGA increase, $1 of reserves is taken away from the banking system.From July to October 2025, bank reserves dropped from 3.4 trillion to 2.8 trillion, accounting for 13% of M2. The last time it touched this level was when three large banks including Silicon Valley Bank collapsed in 2023.ON RRP is nearly exhausted (only 51.8 billion on November 3) and can no longer act as a “shock absorber”.

Triple Squeeze: QT + New Debt + Shut Down

-

Quantitative Tightening (QT)

The Federal Reserve is reducing its asset holdings by $95 billion every month, and reserves continue to be lost.On October 29, the FOMC announced the end of QT on December 1, but it was too late.

-

Huge debt issuance

The deficit in fiscal year 2025 is 2.1 trillion, and tens of billions of government bonds need to be issued every day. Buyers need to prepare US dollars in advance to further drain reserves.

-

closing amplifier

If TGA increases by another 50 billion per week, 200 billion in reserves will be removed in one month.Tax season (January-April) will be even worse.

The Fed’s net liquidity indicator (balance sheet – ON RRP – TGA, inverted) has risen sharply in two months, the DXY US dollar index has risen to 108 during the same period, and the 10-year U.S. Treasury yield is approaching 4.8%.Bitcoin and the S&P 500 fell 1.1% and 0.8% respectively this week, and the VIX rose to 21.

Crisis transmission path

Stage 1: Repurchase out of controlIf SOFR rises to 4.30% (SRF upper limit + 5bp), primary dealers will flock to SRF collectively, and the single-day usage may exceed 100 billion, exposing the reliance on the “lender of last resort”.

Stage 2: Reserve shortageIf the reserve/GDP ratio falls below 11%, banks will reduce on-balance sheet leverage and reduce government debt underwriting.Regional banks are the first to bear the brunt of the pressure – in 2025, three small and medium-sized banks will have non-performing loan ratios exceeding 5%.

Stage Three: Credit FreezeA wave of redemptions from money market funds → a suspension of private repurchases → a break in the payment chain.The probability of a recurrence of the SVB incident in March 2023 has increased to 30% (Goldman Sachs model).

Stage 4: Systemic shockThe Federal Reserve was forced to restart QE, buying 200 billion in bonds every month. The 10-year yield plummeted by 50bp, and the U.S. dollar index collapsed below 100, triggering a loss of inflation expectations.

The latest data at a glance (2025.11.4)

Federal Reserve Emergency Plan

-

Restart QE immediately

Purchase bonds worth RMB 150 billion per month until reserves return to RMB 3.2 trillion.

-

Downregulate IORB 25bp

Stimulates bank lending and lowers SOFR.

-

Expanding SRF counterparties

Incorporate more MMFs and foreign banks.

-

Suspension of new bond issuance

The Ministry of Finance has used special measures (part of which was already used in October).

The path to parliament’s defeat

The most optimistic: Senate bipartisan leaders Thune and Schumer reached a compromise on November 6, the House of Representatives will resume session on November 10, and temporary funding will be provided until January 2026.The most pessimistic: the shutdown is delayed until December, TGA exceeds 1.1 trillion, SOFR rushes to 4.50%, triggering a “flash crash”.

Investors respond

-

cash is king

Increase holdings of 3-month Treasury bills (yield 4.15%).

-

Hedging tail risk

Buy VIX call options and gold ETFs.

-

Pay attention to trigger points

SOFR breaks 4.10% in a row or SRF exceeds 50 billion in a single day, which means reducing positions in risky assets.

The government shutdown was originally a political farce, but it turned into a systemic threat in the context of depleted liquidity.The Federal Reserve has put on a red light: on November 3, SRF usage hit a new high since the epidemic.If Congress delays for another week, TGA will drain another 100 billion in reserves, and SOFR may lose control.History tells us that the 35-day shutdown in 2018 only caused a loss of 0.1% of GDP, but today’s reserves are only 70% of that year, and the ON RRP buffer is exhausted. Any disturbance may ignite the powder keg.Reopening the government is the only key to stopping the crisis.