Author: Stacy Muur, encryption analyst; Translation: xz@bitchainvision

There was a time when managing crypto assets meant juggling multiple wallets, navigating complex exchanges, incurring high exchange fees, and grappling with real-world consumption needs.

Today, a new generation of crypto-digital banks is reinventing this experience.Through a single application, users can not only hold interest-bearing stablecoins, but also directly spend them at merchants, and achieve global capital flows with almost zero friction.

Some platforms are like fintech banks equipped with encrypted channels, while others are built entirely on-chain – integrating stablecoins, DeFi protocols and self-hosted wallets into a unified ecosystem.

This article will provide an in-depth analysis of the current situation, operating mechanism, and service matrix of encrypted digital banks, and analyze the leaders in this field in terms of user experience, profitability, and market penetration.

1. Plasma One

Plasma One is a digital bank and encrypted debit card platform with stablecoins as its core, integrating the savings, consumption, transfer and value-added functions of digital dollars into a single application.

The platform is built on the Plasma Layer1 blockchain and is billed as the world’s first digital bank designed entirely around stablecoins. It mainly serves global users (especially emerging markets) who rely on U.S. dollar stablecoins for daily financial management.The project has strong funds and is supported by well-known investors such as Peter Thiel’s fund and Tether CEO. It has completed US$24 million in financing, and its native token XPL has been oversubscribed by US$3.73 billion.

Core functions:

Non-custodial stablecoin wallet: users hold their own private keys, no mnemonic required;

High-yield savings: The annualized income of USDT exceeds 10%, and the income is accumulated in real time until the moment of consumption;

Visa debit card (virtual + physical): directly use stable currency consumption at more than 150 million merchants in more than 150 countries;

4% cash back on consumption: Rewards are paid in XPL, and active users and partners can enjoy higher levels;

Instant stablecoin payment: USDT transfer on the global fee-free chain (ideal solution for cross-border teams);

Seamless DeFi integration: Revenue sources are connected to liquidity staking strategies such as EtherFi.

fee structure:

There are zero handling fees for stablecoin transfers and consumption;

No monthly fees and account management fees;

No recharge requirements: directly use the interest-earning balance for consumption;

Currency exchange is settled according to Visa network standard exchange rate;

Only third-party partners may charge withdrawal fees.

Other information:

Services cover more than 150 countries (Visa network reachable areas);

It initially supports USDT (Tether) and will gradually expand to more stable coins;

Received investment support from Peter Thiel’s Founders Fund and Tether executives;

The card is issued by Signify Holdings (Visa partner card issuer);

Security measures: Hardware-level key protection, encrypted storage, continuous auditing, real-time fraud monitoring.

2. EtherFi Cash

EtherFi Cash is a non-custodial encrypted digital bank and Visa card service that allows users to consume, borrow and add value through ETH, BTC and stablecoins while fully controlling their assets.

The platform is specially designed for crypto-native users and institutions, integrating DeFi income strategies with real-world financial functions, allowing users to participate in staking, re-pledge and credit guarantee liquidity acquisition without selling tokens.

The EtherFi Cash ecological indicators as of October 20 (data source: Dune Analytics, DeFiLlama) are as follows:

Since its launch in mid-2025, EtherFi Cash has become one of the most active crypto card products on the market.

The platform manages over US$200 million in deposits, has an average of over 2,300 daily active users, and has an average monthly card transaction volume of 12,500.

The product has a huge untapped potential market and abstraction layer design, which can attract both mature investors and ordinary users. These users are likely to gradually convert to other products in the EtherFi ecosystem.

Core functions:

Visa credit card based on crypto-asset collateral;

Enjoy 3% instant cash back on all channel purchases (up to 20% during promotion period);

Spend directly from the DeFi income vault (earn while doing it);

High-yield DeFi vault (annualized stablecoin is about 10%, ETH is about 7%);

Completely unmanaged mode;

Supports automatic repayment using pledge/re-pledge proceeds;

Virtual cards and physical cards are compatible with Apple Pay/Google Pay;

Provide a corporate card system with fund management and control for DAO and encryption teams.

fee structure:

Free of card production fees and account management fees;

Overseas transaction fee: 1%;

ATM cash withdrawal fee: 2%;

0 interest rate for the credit line during the promotion period (subsequent interest rates are anchored in the DeFi market);

No hidden fees or dormant account fees.

Other information:

Services cover most countries (excluding US restricted states and OFAC sanctioned areas);

Run based on Scroll chain;

Cashback is paid in cryptocurrency (SCR or ETHFI) and is automatically credited to your account for every purchase;

All treasury and logic contracts are available on the chain and audited and verified;

Cards are issued under the Visa network by licensed U.S. bank partners;

Nexus Mutual’s DeFi insurance service is optional.

3. Mantle UR

Mantle UR (pronounced the same as “You Are”) launched by Mantle is the world’s first digital bank entirely based on blockchain, aiming to unify fiat currencies and crypto assets into a single account.

UR connects traditional finance and decentralized finance through borderless smart currency applications to achieve seamless consumption, savings and legal currency exchange.The platform provides fully compliant Swiss regulated accounts, allowing users to earn on-chain earnings, use fiat currency deposits and withdrawals, and spend cryptocurrencies globally.

Since its launch in mid-2025, UR has shown strong early growth momentum, with a total of nearly 10,000 accounts opened, and ecosystem activity continues to increase.The number of daily transactions is stable between 250 and 300, and the average daily card transaction volume of mainstream assets exceeds US$40,000.

Relying on the support of Mantle’s more than US$2.3 billion treasury and strategic partners such as Bybit, UR makes full use of Mantle’s infrastructure to integrate stablecoin income, compliant bank channels and global payment services, becoming a “liquidity chain” connecting institutions and retail users.

Core functions:

Multi-currency Swiss IBAN account (supports US dollars, euros, Swiss francs, RMB, etc.);

A self-hosted smart wallet integrating legal currency functions;

USDe’s native income is annualized at 5% (integrated with Ethena protocol);

Access the DeFi income vault (mETH, Mantle Index Fund MI4, etc.);

MasterCard debit card (virtual + physical) covers usage scenarios in more than 40 countries;

Crypto asset mortgage credit line (supports mETH, FBTC);

On-chain identity authentication (NFT KYC pass) and wallet verification;

Compatible with Apple Pay, Google Pay, Alipay, and WeChat Pay;

Access the Mantle Reward Station to get MNT token incentives.

fee structure:

Basic version: 0.5% handling fee for legal currency withdrawals; Professional version: 0% handling fee (specific rates are not disclosed);

USDe is exchanged for fiat currency without withdrawal fees;

Zero fees for stablecoin deposits and internal transfers;

Competitive foreign exchange spreads, no hidden cross-border transaction markups;

MasterCard ATM cash withdrawal: Third-party standard handling fees may be incurred.

Other information:

The service covers 45+ countries in Europe, Asia, Latin America, etc., and is currently not open to US users;

Legal currency funds are reserved at a ratio of 1:1 and are regulated and protected by a Swiss financial technology license;

Regulated by FINMA through SR Saphirstein AG (Switzerland);

Backed by Mantle DAO (formerly BitDAO), its treasury reaches billions of dollars.

4. Gnosis Pay

Launched in 2023, Gnosis Pay is a self-hosted payment network built on the Gnosis chain, aiming to connect traditional finance and decentralized finance.

It provides a Visa debit card directly linked to the Gnosis Safe smart account, allowing users to spend stablecoins like cash at more than 80 million merchants around the world.As a digital banking infrastructure, it focuses on providing B2B solutions for wallets, exchanges and financial technology companies to help them launch branded stablecoin card projects, while consumers use the service through cooperative applications such as Zeal Wallet and Rebind.

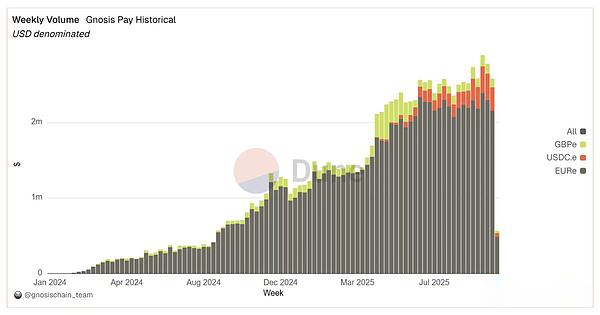

Since its launch, Gnosis Pay has processed more than 1.7 million payments, with total transaction volume exceeding US$107 million. Both transaction volume and the number of active users have grown steadily.

Currently, the platform supports more than 21,000 active fund addresses, with a weekly settlement volume of approximately US$2.5 million, mainly driven by European users’ consumption of EURe stablecoins.

Core functions:

Supports Visa debit cards (virtual + physical) in 130 countries and over 80 million merchants;

Self-hosting through Gnosis Safe: the private key is sovereignty;

Directly use EURe/GBPe/USDCe (Gnosis chain) for consumption;

Up to 5% GNO cashback (graded according to GNO holdings; OG NFT holders +1%);

Obtain a personal IBAN (SEPA) account through Monerium, supporting legal currency deposits and withdrawals;

Supports Apple Pay/Google Pay and global ATM cash withdrawals;

Instant legal currency exchange channel; users do not feel gas fees when using cards;

Programmable spending controls (single-day limits, licensed tokens, whitelisted payees);

Compatible with DeFi wallet function (free access to external income/DEX/lending protocols).

fee structure:

No annual/monthly fees;

The one-time production fee for the physical card is 30.23 euros;

Free of foreign exchange points and transaction fees;

5 free ATM cash withdrawals per month (2% handling fee will be charged for any excess);

Gas fees incurred when using the card will be borne by Gnosis Pay.

Other information:

There is no built-in annualized return on the idle balance; users can allocate funds to DeFi strategies through Safe (obtain external returns);

Already covered in the EU/EEA, UK and Brazil (through local partners), Latin America and Asia Pacific expansion plans have been announced; other regions can apply for a waiting list;

Not available in sanctioned and high-risk areas;

The delay module provides a cancellation buffer period of approximately 3 minutes for suspicious transactions;

Runs on the Gnosis chain.

5. KAST

Launched by a Singaporean financial technology company in 2025, KAST is a Visa-based stablecoin encryption card and digital banking platform that integrates traditional U.S. dollar banking services with cryptocurrency consumption and staking functions.

Users can hold global USD accounts through this platform, use debit cards to consume stablecoins at over 150 million merchants and ATMs, and obtain high SOL staking returns.Relying on the compliance regulatory endorsements of Singapore and the United Arab Emirates, KAST positions itself as a “stablecoin super application” that takes into account asset security and global accessibility.

Core functions:

Global Visa debit cards support more than 160 countries and over 150 million consumption points;

Hold and consume USDT, USDC, PYUSD, USDe and KAST Dollar across chains;

3–10% cashback on consumption (issued as KAST points, which can be redeemed for rewards or token rights);

The “Grow” savings account will be launched soon, providing an annualized return of approximately 4.5% on stablecoins;

Integrated legal currency channels (ACH, SEPA, PIX, SWIFT) support bank deposits and withdrawals;

Solana staking integration, the comprehensive annual income is up to 21% (including SOL and KAST rewards);

Support Apple Pay and Google Pay (one-click quick payment for stable currency);

Real-time transaction reminders and instant card control within the APP;

Virtual card and metal card options (including gold version and LED lighting level).

fee structure:

Free account opening and virtual card issuance;

0 handling fees for base currency transactions;

A 2% currency conversion fee will be charged for non-USD purchases;

ATM cash withdrawal: fixed fee of US$3 + 2% of the cash withdrawal amount;

Optional paid packages (annual fee 1,000-10,000 US dollars) enjoy bonus bonuses and exclusive customer service;

Stablecoin recharge is free of deposit and transfer fees;

Other information:

Services cover more than 160 countries; will expand to the United States and Asia-Pacific markets in 2025;

Adopt a licensed partner custody model and a regulated reserve mechanism;

Implement 1:1 full reserve; KAST Dollar stablecoin will be launched soon to realize on-chain reserve transparency;

Access to the Visa global network, equipped with bank-level encryption and anti-fraud protection;

Supports blockchains: Solana, Ethereum, Tron, BNB Chain, Arbitrum, Polygon, XRPL;

It is supported by top financial technology investors such as Sequoia China, Peak XV, and Stripe’s Bridge Fund.

6. Payy wallet

Payy is a self-hosted Ethereum second layer network built for privacy-compliant, zero-gas stablecoin transactions.It is built based on the ZK validity proof architecture and UTXO state model, integrating cryptographic-level privacy protection and practical ease of use, allowing anyone to send and receive stablecoins such as USDC with no gas cost, complete privacy, and optional compliance.

Core functions:

Privacy-protecting wallet that supports stablecoins;

Visa debit card available for spending (virtual/physical card with illuminated logo);

Realize instant, zero-fee private transfers through payment links;

Access to legal currency exchange channels (banks, Apple/Google Pay, encrypted wallets);

Self-hosted application with built-in ZK proof, transactions cannot be traced;

The upcoming guardian mechanism will enhance the security level.

fee structure:

No transactions, recharges, gas and monthly fees;

No foreign exchange fees (non-USD transactions are calculated at Visa exchange rate);

Core services are clearly marked as completely free;

Points-earning rewards for consumption will be launched soon (currently there is no profit function);

Other information:

Supports deposits into bank accounts in the United States and Argentina, and can use cards at more than 80 million Visa merchants around the world; the service area continues to expand.

7. Coinbase One Card

Coinbase One Card is a crypto credit card and digital banking service launched by Coinbase, aiming to integrate traditional banking functions with the crypto ecosystem.The product combines a rewards credit card (issued on the American Express network) with the Coinbase subscription service (“Coinbase One”) to provide crypto users with an integrated financial solution.

Core functions:

Visa/American Express credit card, you can get up to 4% Bitcoin cash back for each purchase;

High-yield savings: USDC deposit annualized 4.25% (maximum USD 10,000);

ETH, SOL and other asset pledge reward bonuses (+5%);

Fee-free crypto trading ($500 monthly limit on basic Coinbase One);

Supports the direct use of cryptocurrency to repay credit card bills;

Dedicated customer service and American Express travel/shopping protection;

Contains Base network Gas fee deduction limit (for on-chain operations);

Deep integration with Coinbase exchange and wallet infrastructure.

fee structure:

No annual fee (but you need to subscribe to Coinbase One service: basic version $49.99/year);

No foreign exchange fees, no encryption consumption fees, no ATM cash withdrawal (credit card attributes);

Interest on repayments not made in full will be calculated at the standard annual interest rate (the specific interest rate is not disclosed);

Cryptocurrency repayments are charged at Coinbase’s regular exchange spreads;

Other information:

Custody model: All assets are managed by the listed company Coinbase;

U.S. dollar deposits are protected by FDIC insurance, but crypto assets are not applicable;

Only available to U.S. residents (covering 50 states, cards issued by American Express). It is not currently supported in overseas areas (territorial and non-U.S. users cannot use it);

Equipped with two-factor authentication, biometric login, address whitelist and card freezing control functions;

Cards are issued by Cardless through the American Express network;

Non-credit establishment orientation: Designed for crypto-active users with existing credit records.

8. MetaMask Card

MetaMask Card is a self-hosted crypto debit card developed by Consensys in partnership with Mastercard and Baanx (Crypto Life).Users can spend directly with cryptocurrencies in the MetaMask wallet at merchants around the world that accept Mastercard, and enjoy real-time on-chain exchanges, interest-bearing stablecoin balances, and crypto cashback rewards.Designed specifically for DeFi native users, the product combines bank-like functionality with complete wallet autonomy.

Core functions:

Global MasterCard debit card (virtual/physical) linked to MetaMask wallet;

Directly use ETH, USDC, USDT, aUSDC, EURe, and GBPe on the Linea network for consumption;

Self-custody mode: funds are always deposited in the user’s wallet before payment is executed;

Real-time on-chain exchange for fiat currency at the point of sale (no pre-recharge required);

Integrate Apple Pay and Google Pay to support Quick Pass function;

Receive 1–3% USDC cashback (up to 13% for on-chain reward partners);

Supports interest-bearing aUSDC and Aave Boosts (potential annualized return 4–8%);

Built-in DeFi revenue aggregation (Aave, Linea) and Coinmunity token rewards;

Real-time consumption limit, instant freezing/unblocking and in-APP management functions.

fee structure:

Standard cards are free of monthly fees and card creation fees;

Each transaction generates Gas fees (approximately $0.01–0.02) on the Linea chain;

Cryptocurrency exchange fee 0.5–0.875% (fluctuates depending on asset type);

Foreign exchange handling fee is 1% (can be waived for metal card tiers);

ATM cash withdrawal fee is 2% (free for metal cards within US$1,200 per month);

The annual fee for the metal card is US$199 (enjoy 3% cash back, zero foreign exchange fees and higher limits);

No pre-top, escrow or transfer fees.

Other information:

Service area: Argentina, Brazil, Canada, Colombia, Mexico, EU/EEA, United Kingdom, United States and Switzerland under pilot;

Custody mode: 100% self-custody (controlled independently by the wallet);

Security mechanism: Mastercard-level anti-fraud protection, on-chain consumption limits, complete wallet control;

Supported chain: initially based on Linea, with plans to expand to Ethereum, Arbitrum and Polygon;

Card issuer: Baanx (Crypto Life), an electronic money institution regulated by the British FCA;

User qualifications: KYC required, open to global individual users (continuous expansion in 2025).

9. Gemini Credit Card

The Gemini Credit Card is a crypto rewards credit card launched by the regulated cryptocurrency exchange Gemini in partnership with WebBank, focusing on the US market.The product provides convenient financial solutions for daily needs, including themed versions that allow you to spend fiat currency while earning crypto rewards with value-added or staking potential.

Core functions:

Personal credit card for US residents, supporting global consumption;

High category crypto rewards (up to 4% cash back on gas/transportation, 3% on dining, 2% on groceries, 1% on others);

Mastercard credit card (physical/virtual card, providing Bitcoin/XRP/Solana and other themes) for consumption;

Rewards are deposited into Gemini accounts in real time for trading or holding;

The Solana theme version automatically stakes SOL rewards.

fee structure:

No annual fees and overseas transaction fees;

Late payment fee: up to $8;

Chargeback fee: up to $35;

The floating annual interest rate is higher: 19.24%-35.24% (full repayment can be avoided; there are no fees for bonus benefits).

Other information:

Service area: Credit cards are only available to US residents (50 states); exchange services cover more than 60 countries around the world;

Custody mechanism: Gemini uses offline cold storage to store assets and provides hot wallet insurance;

Security certification: Passed SOC 2 audit, supports double verification, address whitelist function, and US dollar assets enjoy FDIC penetrating insurance protection.

10.THORWallet

Thorwallet is a self-hosted, multi-chain wallet that integrates a Swiss-regulated IBAN account (via Fiat24) and a virtual Mastercard compatible with Apple Pay, Google Pay and Samsung Pay.

Users can exchange cryptocurrencies for euros, Swiss francs, US dollars and RMB balances, spend them globally, and always maintain full self-custodial control of digital assets until a transaction occurs.

Core functions:

Self-hosted wallet (supports multiple chains);

Card used: Virtual MasterCard (no physical card yet); supports Apple/Google/Samsung Pay; deducts money from fiat currency sub-accounts in real time; no need to pre-charge segregated accounts;

THORChain savings pool (supports single assets such as BTC/ETH, etc.) → generates floating “real income” through exchange fees (settled with the same asset);

Stable currency treasury (USDC/USDT on the EVM chain) → floating annualized income driven by handling fees.

fee structure:

Account/Card: 0 monthly fee, 0 annual fee, no dormant account fee;

Cryptocurrency → Fiat currency deposit/foreign exchange rate:

Standard version (free): 1.0%;

Gold version: 0.5% (one-time upgrade fee is about 1.54 ETH);

Platinum version: 0.25% (one-time upgrade fee is about 15 ETH).

Other information:

Service area: Covering more than 60 countries including the EU/EEA/UK/Asia-Pacific/Canada, the United States is not supported.Bank/card services require KYC; wallet/DeFi functions remain without permission;

Limit (standard version): monthly bank transfer is about 100,000 US dollars; monthly card consumption is 20,000 US dollars (the maximum in a single day is about 10,000 US dollars).Paid tiers enjoy higher limits;

Transfer: SEPA/IBAN transfers on ThorWallet are free;

Network cost: Charged normally according to each chain’s Gas fee/THORChain handling fee (application automatically optimized; some support “zero Gas” path);

ATM: Not supported (virtual card only);

Protocol pledge (TITN) → Obtain stable currency revenue share; the pledge weight can increase the revenue multiple.

11. Bybit Card

Bybit Card is a Mastercard crypto debit card launched by the global cryptocurrency exchange Bybit. Users can directly use cryptocurrency for consumption at more than 90 million merchants around the world.The card supports real-time cryptocurrency-to-fiat conversion, high cashback rewards and passive income, and is designed to meet the needs of crypto-native users who pursue convenience and performance.

Core functions:

Virtual and physical Mastercard debit cards (supports chip, contactless payment and ATM cash withdrawals);

Real-time cryptocurrency to fiat conversion at the point of sale;

Supports BTC, ETH, USDT, USDC, XRP, and TON (more assets will be launched soon);

Cash back up to 10% (depending on Bybit VIP level);

Idle cryptocurrency can enjoy up to 8% annualized income through automatic savings;

Compatible with Apple Pay, Google Pay, Samsung Pay;

3D security verification, instant card freezing/unfreezing, transaction reminder;

Supports ATM cash withdrawal, subscription cashback (Netflix, Spotify) and loyalty points.

fee structure:

No annual, monthly or account dormancy fees;

Cryptocurrency exchange fee: approximately 0.9% per transaction;

Foreign currency transaction fee (non-Euro settlement): about 0.5%;

ATM cash withdrawal: the first 100 euros per month is free, and 2% is charged for the excess;

Virtual card: free | Physical card: about 5 euros (free for VIP users);

Cashback rewards are issued in Bybit points (can be exchanged for cryptocurrency or privileges).

Other information:

Service area: covering most of Europe, Australia, Latin America, some Asia-Pacific countries and the Astana International Financial Center (the United States is not supported);

Open to non-U.S. users who have completed full KYC (identity proof + address verification);

Funds are deposited in Bybit custodial exchange accounts;

Achieve income, reward and consumption functions through a unified encrypted asset panel;

Relying on Bybit exchange custody, reserve certificates and multi-regional compliance regulatory endorsements;

It is most suitable for active traders, advanced DeFi users and groups who pursue high cash rebates and are unwilling to sacrifice liquidity.

12. Crypto.com Card

Crypto.com offers prepaid Visa cards and integrated digital banking features (cash account with bonuses).The card supports the use of cryptocurrency (through fiat currency exchange channels) or fiat currency consumption at Visa acceptance points around the world, and provides $CRO token tiered rewards based on level.The bank provides insured US dollar accounts (insured by Green Dot Bank in the United States), supports IBAN/ACH transfers, and has an annualized return of up to 5% on the balance.The two together form an encryption-friendly card banking service system covering users in many countries.

Core functions:

Covering users in more than 40 countries and supporting global Visa network consumption;

Tiered cash back on consumption (black gold level can get up to 8% $CRO reward);

Prepaid Visa cards (all levels have metal card faces), support consumption and ATM cash withdrawal;

A one-stop application integrating trading, wallet, NFT market and lending functions;

Provide income for locked assets through “crypto interest”;

Premium privileges such as Spotify/Netflix reimbursement, airport lounge access and exclusive events;

A custodial ecosystem that supports legal currency deposits and salary distribution services.

fee structure:

No annual fees, monthly fees and foreign exchange fees;

The monthly free ATM cash withdrawal limit depends on the level (200-1,000 US dollars), and a 2% handling fee will be charged for the excess;

In-app transaction rates are as low as 0.075%; recharge fees and core transaction fees are waived;

High levels require a pledge of CRO (for example, the black gold level requires a pledge of US$400,000);

Other information:

Services cover more than 100 countries (the United States supports 49 states, except New York State);

USD funds are held in custody by cooperative banks and are insured by FDIC (up to US$5 million, US users only);

The default custodial wallet; an independent DeFi wallet is also provided to support non-custodial use;

Reward levels require holding CRO tokens; high levels require staking/locking CRO;

CRO rewards are distributed to encrypted wallets in real time and can be traded/liquidated at any time;

Comprehensive KYC compliance; regulated by the United States, European Union, Singapore, and the United Kingdom.

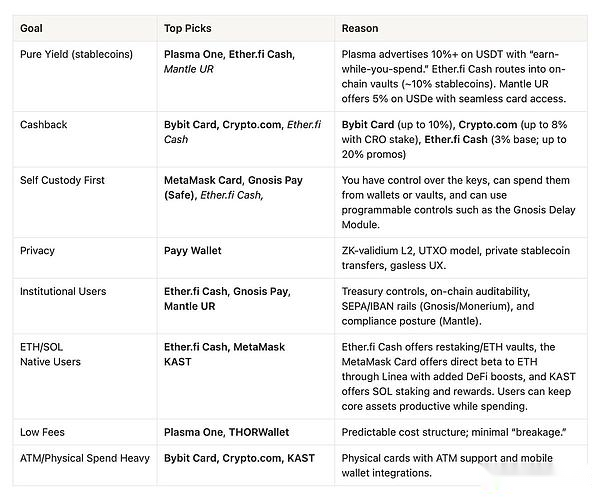

How to choose a suitable encryption card?

Finally, we present the advantages of each encryption card through an objective decision matrix.The evaluation criteria focus on the core concerns of real users: actual revenue, stable reward mechanism, hosting model, fee structure, and the current range of products available.

Each model reflects a different prediction of the future direction of DeFi – whether it focuses on income, reward mechanisms, compliance or privacy protection; but the common development trajectory is clearly visible: encrypted native currencies are accelerating the integration with the usability standards of modern financial technology.

The winning products will be those that balance regulatory clarity, user control and global accessibility without sacrificing security or transparency.

As the digital banking ecosystem matures, they will become the operational layer of the digital economy.Its success does not depend on brand marketing or token incentives, but on its ability to continue to provide reliable and flexible services and create real value for global users.

Have you entered the new era of digital banking?