Author: Zhang Feng

The historic closed-door meeting of the Federal Reserve quietly changed the position of cryptocurrencies in the global financial system.On October 21, Federal Reserve Governor Christopher Waller made it clear at the first “Payment Innovation Conference” held at the Federal Reserve Headquarters that “the DeFi industry will no longer be regarded as suspicious or ridiculed, and the Federal Reserve will actively embrace payment innovation.” This so-called “historic” conference is unusual – it no longer treats cryptocurrency as a marginal threat to the financial system, but discusses it as a key component of the future payment system.

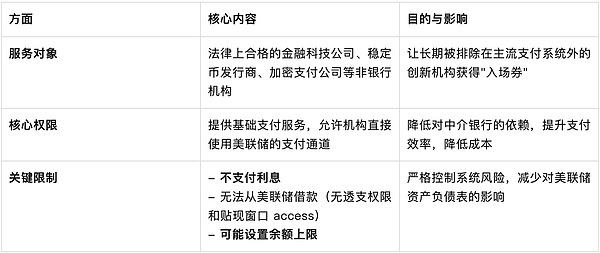

What is even more striking is that the Federal Reserve has proposed a specific concept of “streamlined moderator accounts” to provide basic payment services to non-bank payment companies, which meansStablecoin issuers and crypto payment companies are expected to have direct access to the Federal Reserve’s payment system, eliminating their reliance on traditional banks.

1. From suspicion to embrace, the Fed’s attitude has changed dramatically

Global payment innovation has entered a period of acceleration, with cross-border applications of stablecoins, tokenization of traditional assets and AI-driven payment security technology becoming the focus of the industry.In this context, the Fed’s choice is not to resist, but to actively participate and guide the direction of innovation.This meeting marked the beginning of the U.S.There has been a fundamental change in the attitude of regulators towards crypto-assets and AI payments.The Fed’s stance has changed from vigilance and suspicion in the past to openness and acceptance now, demonstrating its recognition of the trend of financial innovation.

In his speech, Governor Waller elaborated on the Federal Reserve’s dual role in payment innovation: one is to act as a convener to solve coordination problems, and the other is to operate core payment and settlement infrastructure.He emphasized that the Fed is “looking ahead to conduct real-world research on tokenization, smart contracts, and the intersection of artificial intelligence and payments.”Behind this change in attitude is the Federal Reserve’s clear understanding of the current payment revolution situation.

2. The new financial era of AI and asset tokenization

This meeting will focus onIntegration of traditional finance and digital assets, stable currency business model,AIApplications in payment, tokenized productsFour core topics were discussed to outline a clear outline of the future payment ecosystem.

In terms of AI applications, Cathie Wood, CEO of ARK Invest, proposed,AIThe driven “agent payment system” will open the era of “Agent commerce”.She believes that AI can not only “know” but also “execute” and make financial decisions independently on behalf of users.Wood predicts that the huge productivity unleashed by AI and blockchain is expected to drive U.S. real GDP growth to 7% in the next five years.

Richard Widmann, head of Web3 strategy at Google Cloud, pointed out the natural fit between AI and stablecoins, “AI agents cannot open traditional bank accounts like humans, but they can have encrypted wallets. The programmability of stablecoins makes them a perfect fit for AI-driven automated micro-transactions and machine-to-machine settlement scenarios.”

Asset Tokenizationis another major focus.Traditional financial institutions are accelerating their deployment in this field.As of 2025, the global tokenized asset market will be approximately US$28 billion. Despite rapid growth, it is still far lower than the total volume of the US ETF industry.

3. “Simplified moderator account” to get through the last mile

The most noteworthy policy innovation of this meeting isThe concept of “streamlined moderator accounts” proposed by the Federal Reserve.This move is expected to pave the way for non-bank payment companies to directly access the Federal Reserve payment system, fundamentally reducing operating costs and improving efficiency.

The proposal of “lite account” marks a fundamental change in the Federal Reserve’s attitude towards financial technology, especially crypto-assets – from suspicion and scrutiny in the past to positive acceptance and integration.As Fed Governor Waller made it clear that the DeFi industry will no longer be doubted or ridiculed, and the Fed will “embrace disruption rather than avoid disruption.”This move is expected to solve the dilemma that companies like Custodia Bank and Kraken have been seeking master accounts for years, and speed up the approval process for companies such as Ripple that have submitted applications.In the long run, this is not only technology access, but also an evolution of the financial system structure.It heralds that the “pipeline” privileges of traditional banks in the payment field will be weakened, and financial technology companies will gain access to direct dialogue with the central bank, which is expected to greatly promote innovation and competition in the payment field.

For the crypto industry, this move is far-reaching.Crypto journalist Eleanor Terrett pointed out that the move is of great significance to companies such as Custodia Bank and Kraken, which have been trying to obtain the Fed’s master account for years, and Custodia even took the Fed to court.Companies such as Ripple and Anchorage that applied this year may also accelerate their access.

4. Opportunities and challenges between Hong Kong and the Mainland

Participating institutions included banks, asset managers, retail payment companies, technology companies, and crypto-native fintech companies, reflecting that distributed ledgers and crypto-assets are no longer marginal but increasingly integrated into the architecture of payment and financial systems.This series of actions by the Federal Reserve provides strong endorsement for the further integration of traditional finance and crypto assets.

Overall, the Federal Reserve Payment Innovation Conference pointed out the general direction of financial digitalization for Hong Kong and the mainland.The key for Hong Kong is how to balance risks in opening up, while the focus for the Mainland is on how to carry out innovative applications based on its own actual conditions.In the context of the integration of AI and blockchain to create new financial infrastructure, the two places should give full play to their respective advantages and will be better able to participate in shaping the future global financial landscape.

For Hong Kong, on the one hand, Hong Kong can consolidate its position as a financial hub.Hong Kong already has a practical foundation in the field of asset tokenization. For example, HSBC Holdings has completed a cross-border U.S. dollar tokenized deposit transaction.The Federal Reserve’s actions will further promote the process of global financial digitization.Hong Kong can take this opportunity to actively develop the tokenization market and explore cooperation withAICombined with advanced payment innovation, it attracts more international capital and projects and consolidates its status as an international financial center.

On the other hand, Hong Kong faces competition and regulatory pressures.As an international free port, while Hong Kong is actively introducing innovative businesses, it also faces the challenge of how to strike a balance between encouraging innovation and preventing and controlling financial risks.The Federal Reserve’s discussion of the regulatory framework for stablecoins means that Hong Kong also needs to establish a corresponding regulatory system to deal with possible cross-border risk transmission.

For the mainland, on the one hand, it can take advantage of the situation to develop its own technology.The mainland has established technical specifications in the areas of financial authentication and payment security.This can be the basis forAccelerate blockchain andAIIn-depth integration of technology in payment, identity authentication, supply chain finance and other scenarios.at the same time,The Federal Reserve’s exploration has also provided the mainland with valuable experience in promoting technology application under the premise of controllable risks.

On the other hand, the mainland needs to deal with technological competition and gaps.The Fed’s move could accelerate the digital race for global financial infrastructure.If Hong Kong and the mainland cannot keep up, they may face the risk of falling behind in areas such as cross-border payments and digital asset pricing power.In addition, differences in technical routes may also lead to challenges in the interconnection of different digital financial ecosystems in the future.

This Fed meeting is just the beginning.As “lite moderator accounts” move from concept to reality, stablecoin issuers and crypto payment companies will have direct access to the Federal Reserve payment system, the financial fortress dominated by traditional banks is showing structural cracks.andAIIntegration with blockchain may push this change deeper.Richard Widmann, director of Web3 strategy at Google Cloud, pointed out that AI agents cannot open traditional bank accounts like humans, but can have crypto wallets.Financial transactions in the future may no longer be led by humans, but completed automatically through crypto wallets between AI agents.

Standing at a turning point in history, regulatory agencies in various countries have to make a choice – whether to build a higher wall or embrace an irreversible trend.The Fed has made its choice.