TL;DR

-

Brief anchorage, quick repair:On October 11, 2025, USDe briefly fell to$0.65, but only for a few minutes.The overall breakout lasted about 90 minutes ($0.75-$0.98), with trading volume exceeding780 million pieces.price atBeijing time 06:45It has completely stabilized to around $0.99 before.

-

Local liquidity dislocation:Volatility is mainly concentrated on Binance.The price deviations between other major exchanges and DEX (Bybit, Curve, Uniswap) are all within 0.3%, shown asSingle point liquidity imbalancerather than a systemic problem.

-

Not the cause of the market crash:BTC, ETH, SOL atBeijing time 04:45Be the first to go down, triggering a chain reaction of liquidation.USDe’s price deviation is more likeSecondary liquidity release, rather than the triggering event that caused the decline.

-

The protocol robustness is verified:Ethena successfully processed over 24 hours$2 billion in redemptions, with no downtime or delays.The price of the Aave oracle remains in the $0.99–$1.00 range, and the system shows no signs of liquidation, default, or liquidity run.

-

Systemic risks are controllable:The three major exchanges (Binance, Bybit, OKX) collectively hold approximately$2 billionVenture funds, under similar market conditions, can theoretically carry approximately$200 billion liquidation impact, significantly reducing the risk of ADL (automatic deleveraging) triggering.

On October 11, 2025, USDe briefly decoupled to $0.65 on Binance, but only for a few minutes.The overall unanchoring lasted about 90 minutes ($0.75-$0.98), with a trading volume of over 780 million coins.During the same period, other major exchanges and on-chain market prices basically remained in the range of $0.99–$1.00, with limited fluctuations.Overall, this is a local liquidity dislocation rather than a mechanical risk event – the liquidation chain triggered by the sharp decline of BTC is amplified in trading venues with local depth and weakness.The Ethena protocol remains viable in a high-volatility environmentStable hedging structure, smooth redemption path and robust oracle system, successfully withstood the actual stress test and verified that its stabilization mechanism has goodImpact resistance and self-healing ability.

Ethena’s USDe stability mechanism has withstood the test of actual combat

USDe’s brief price dislocation on Binance

On October 11, 2025, USDe briefly became unanchored on Binance, with the lowest price touching $0.65 for about 90 minutes, during which the trading volume exceeded 780 million coins.

During the same period, Bybit, as the second largest exchange in the spot market, also experienced a slight deviation in its USDe/USDT trading pair, but the magnitude was limited and the trading volume was low, so the impact on the overall market was negligible.

Overall, the de-anchoring of USDE on Binance lasted about 45 minutes, with a maximum de-anchoring amplitude of about −35% (instantaneous). During the period, the total trading volume exceeded 780M USDE.The nature of the event is closer to a liquidity flash crash than to a protocol structural risk.

The de-anchoring and re-anchoring process of USDe on Binance Spot (USDE/USDT)

USDE/USDT price chart on Binance exchange

USDE/USDT price chart on Bybit exchange

USDe has no systematic deviation on the DEX side (Uniswap/Curve)

Compared with Binance’s deep de-anchoring, on-chain DEX (such as Curve, Uniswap) only experienced slight and delayed price fluctuations, with a minimum of approximately$0.995, the whole remains stable and almost unanchored.

Uniswap’s USDe/USDT price chart

Curve’s USDe/USDC price chart

USDe on Binance: Growth Trajectory and Post-Event Adjustments

Binance will be officially launched on September 22, 2025USDe Reward Program, providing users with the highest12% annualized return.The platform records the user’s minimum USDe position in spot, capital and margin accounts (including mortgage assets) through daily random snapshots, calculates the income on an annualized basis, and distributes it to the spot account every Monday.The activity cycle isSeptember 22 to October 22, 2025, users with a position of no less than 0.01 USDe and a holding period of more than 24 hours can participate.

Driven by this incentive plan, the USDe stock on the Binance platform once exceeded$5 billion.

Currently, USDe’s lending and contract mortgage functions on Binance are suspected to be temporarily closed, the front-end cannot be verified for the time being, and the relevant leverage and lending data have not been made public.

Based on subsequent announcements and parameter adjustments, it is speculated that Binance mayDirectly adopt the price index of USDeAs a core price feed reference, its lowest transaction price is approximately $0.66.

After the October 11 incident, in order to improve the robustness of the system, Binance immediately adjusted the risk control parameters of USDe, including incorporating the redemption price into the price index, setting minimum transaction price limits, and increasing the frequency of parameter reviews to respond to potential market fluctuations.

In addition, according to Binance’s latest announcement, the platform has launched for users affected by this incident (including USDe, BNSOL and WBETH unanchoring related assets)Compensation plan of approximately $283 million.

Binance’s USDE Index Price

The USDe lending market on Aave remains stable without serial liquidations

When analyzing Aave’s related markets, the main focus isUSDe lending poolJust use sUSDe.Although other USDe-related assets (such as pt-sUSDe, etc.) exist on Aave, because the price and USDe itself are highly correlated, the USDe principal of the Pendle protocol is limited.

at present,USDe’s lending pool is mainly distributed on two chains: Ethereum (approximately $1.1 billion) and Plasma (approximately $750 million).Meanwhile, sUSDe has approximately $1 billion in deposits on Ethereum.

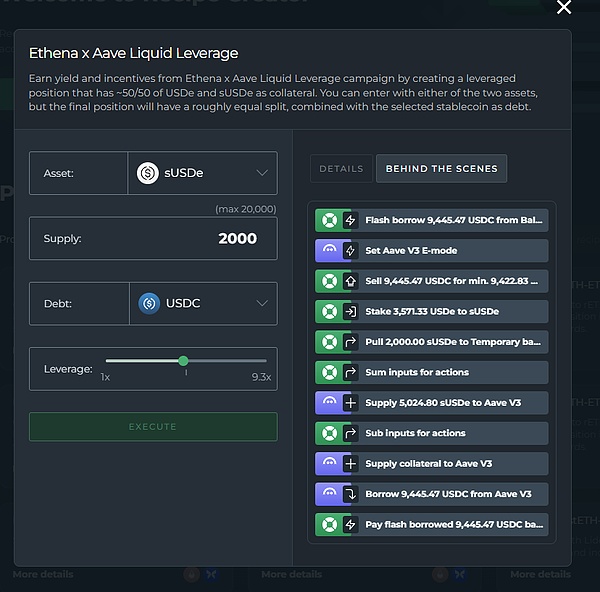

Because there is on the chainrevolving loanmodel, some users will use USDe and sUSDe as collateral to lend other stablecoins, and then re-convert and mortgage the resulting funds into USDe and sUSDe to achieveLeveraged USDe return amplification strategy.

Aave’s USDe and sUSDe revolving loan process

Judging from Aave’s price feed data, USDe’s oracle price within the platform has always remained near $1, or even slightly above $1.The price feed of sUSDe remains at around 1.2, which means that USDe and sUSDe lending users on Aave have not been actually affected by the unanchoring of Binance USDe spot.

Note: This analysis focuses onLending cycle and stability performance related to USDe and sUSDe, other liquidation behaviors using mainstream assets such as BTC and ETH as collateral are not within the scope of discussion.

Aave Ethereum’s USDe price feed

Aave Plasma’s USDe price feed

Aave Ethereum’s sUSDe price feed

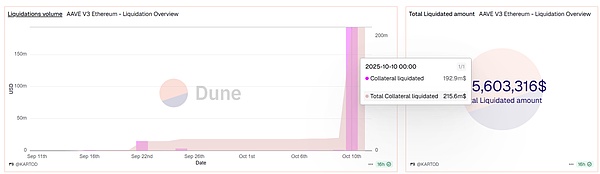

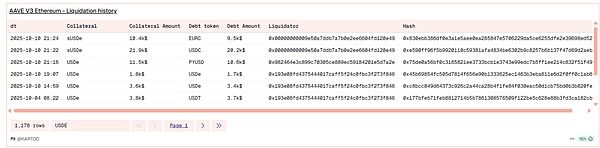

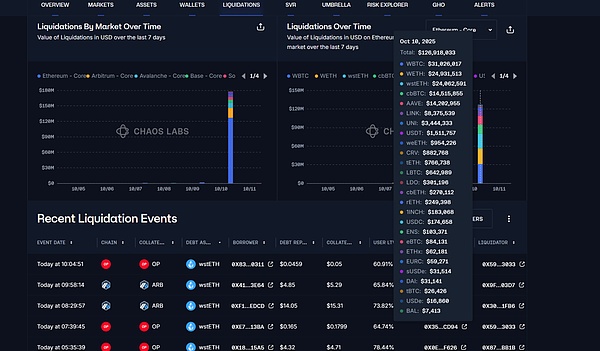

We also tracked Aave’s liquidation through a third-party data analysis platform.Data shows that despite the market rout (October 10-11, 2025)Aave’s overall liquidation volume is as high as $192 million, but the liquidation events related to USDe and sUSDe are very few and almost negligible.

Aave’s Reckoning Dune Panel

In the monitoring data of Chaos Labs, another risk analysis platform, Aave’s liquidation activities can also be seen, but there are no liquidation records directly related to USDe and sUSDe.

Aave liquidation data provided by Chaos Labs

Aave’s oracle pricing and price feed logic for USDe

Aave’s pricing of USDe is not fixed at $1, but uses a combined oracle mechanism:

USDe Price = Chainlink USDe/USD Price Feed × sUSDe/USDe Internal Exchange Rate × CAPO (Price Adapter) Adjustment Factor

This pricing logic is clearly stated in Aave’s official governance proposal “sUSDe and USDe Price Feed Update” and its risk analysis document.

Although there are currently some community proposals to “hard-code” the USDe price to $1 (that is, directly aligned with USDT), the relevant plan has not yet been adopted or deployed.

Therefore, Aave is still based onChainlink real-time price feed and sUSDe internal exchange rateCalculate the reference price in USDe.

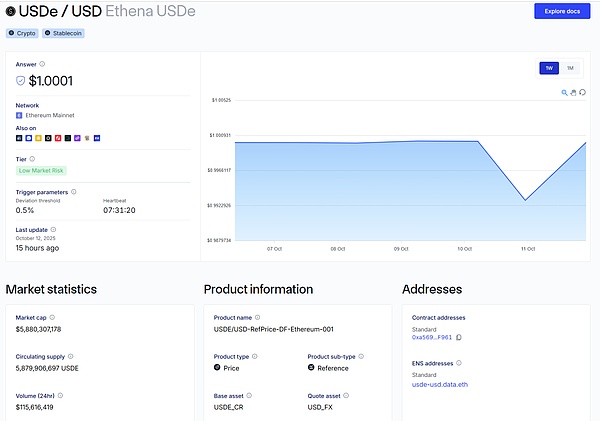

During the period of October 11-12, 2025, the USDe/USD price feed provided by Chainlink has always remained in the range of $0.992-$1.000, with minimal overall fluctuations and no significant de-anchoring.

Chainlink’s USDe price feed adoptedMulti-source aggregation and denoising weighting mechanism: It is not taken directly from a single exchange, but by integrating transaction data from multiple centralized and decentralized markets, and calculating a verified weighted average price (Reference Price) through node network aggregation and outlier filtering.

This price feed is usually updated in minutes and is widely used for mortgage and liquidation calculations in protocols such as Aave.

Thanks to this mechanism, USDe’s pricing on Aave can effectively reflect itsFull market fair value, thereby avoiding price deviations due to short-term fluctuations or liquidity imbalances on individual exchanges.

Chainlink’s USDe price feed

During the unanchoring period, there were no abnormal USDe fund flows on Binance.

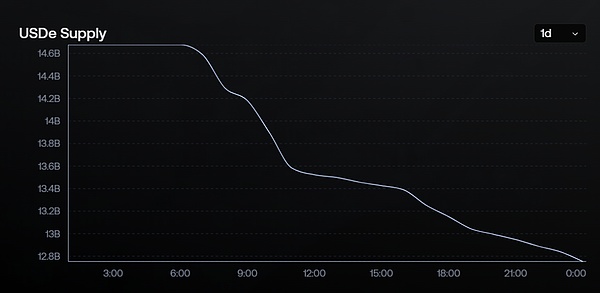

No obvious abnormal capital inflows were observed.Binance’s USDe stock is approximately US$4.7 billion. After the incident, it dropped significantly from the previous US$5.2 billion, a drop of approximately US$500 million.This change is related toTotal USDe supply drops from $14.6 billion to $12.8 billionThe overall trend is basically the same.

From the perspective of collateral structure,BTC positions decreased by approximately US$650 million, ETH by approximately US$130 million, and stablecoin assets by approximately US$400 million..Based on comprehensive judgment, the decline in USDe issuance this time is mainly due toLong positions liquidated and capital capacity shrinks in the derivatives market, rather than a stability attack or run on a single exchange level.

Arkm’s Binance asset profile

USDe supply changes

Changes in USDe’s underlying assets

Changes in USDe’s underlying assets

The relationship between the overall market decline and USDe de-anchoring

In fact, BTC began to fall at 4:45, and major assets such as ETH and SOL also experienced corrections during the same time period.The market pinned at 5:15, but at this timeUSDe has not yet clearly decoupled.

Therefore, it can be speculated that the de-anchoring of USDe was not directly triggered by the overall market decline, but was more likely to stem fromUsers holding revolving loan positions on Binance concentrated on selling USDe in response to margin pressure., thus triggering short-term liquidity runs and price de-anchoring.

It remains unclear whether any market makers will use USDe as collateral to participate in market liquidity provision.Based on actual testing, Binance currently only allows USDe to be deposited into margin accounts and has not yet opened the function as contract collateral, so its market making use may be limited.

BTC price drop icon

ENA Systemic Risk and USDe Stability Analysis

ENA system anti-risk structure

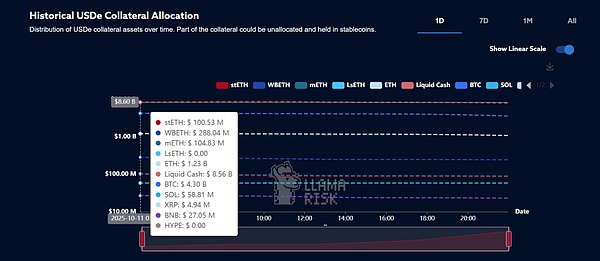

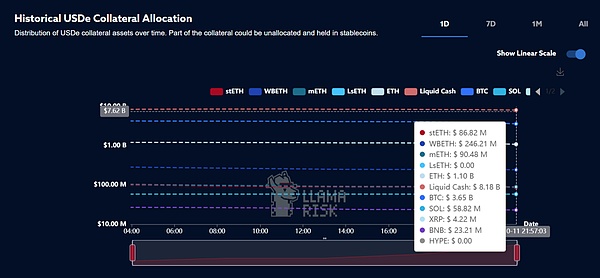

Under the current ENA ecosystemThe total issuance of USDe is calculated based on US$14 billion..

in:

-

About 60% (≈$8.4 billion)It is the “liquid stablecoin” part, mainly used for internal deployment and circular mortgage of the protocol;

-

About 40% (≈$5.6 billion)Stablecoin liabilities formed for hedging structures,in:

-

BTC spot + short orderAccounting for approximately 28% (corresponding to the issuance of approximately 3.9 billion USDe);

-

ETH spot + short orderAccounting for approximately 11% (corresponding to the issuance of approximately 1.54 billion USDe).

This means that the stability of the BTC and ETH hedging positions directly determines the risk resistance of the entire system.

core systemic risk

USDe’s main systemic risk lies in itsEffectiveness and sustainability of short hedging orders:

-

If the short order of BTC/ETH is affected by sharp market fluctuations orADL (automatic deleveraging)If the position is triggered and forced to be liquidated, the ENA protocol will lose the corresponding neutral hedging structure.

-

At this time, what the agreement holds will no longer be a hedging portfolio, but will become a contract portfolio.$3.9 billion in BTC long exposure.

-

If the market falls further 10%–20%, USDe’s asset side will experience actual losses, and the stablecoin will faceTrue anchor breaking pressure.

also,Funding rate contraction and position closing delays under extreme market conditionsIt may also lead to an expansion of losses on the asset side, which can be confirmed by the data on the decline in the proportion of BTC in this incident.

The possibility of breaking anchor again and monitoring points

The market anchoring of USDe is mainly composed ofExchange order bookTherefore, if a large amount of selling occurs (such as concentrated selling by whales), even if the asset side is still healthy, it may cause a short-term destabilization.

The following indicators need to be continuously monitored:

Potential impact on overall liquidity

If USDe materially unanchors, the market impact could be close to a local liquidity crisis:

-

BTC hedging positions at the protocol level expire →Asset-side risk exposure exposure;

-

LPs and lenders of the stablecoin pool will give priority to divestment →Liquid stablecoin outflows accelerate;

-

If a feedback chain is formed,The magnitude of de-anchoring is positively correlated with the magnitude of BTC’s decline

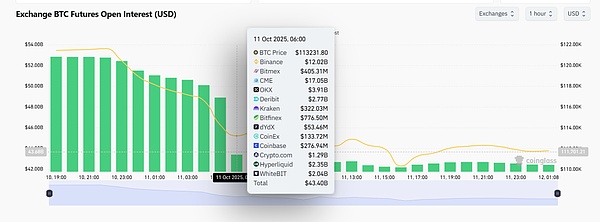

BTC contract OI data

Ethena’s response mechanism to ADL and exchange risks

The Ethena team has already made plans for potential ADL (automatic position reduction) and exchange system risks, and has clearly stated this in official documents.

This part mainly targets two types of scenarios:

-

Auto Deleveraging risk;

-

Exchange Failure Risk (exchange failure or bankruptcy risk).

Auto Deleveraging (ADL)It is the “last line of defense” used by major derivatives exchanges to prevent systemic risks under extreme circumstances.When the insurance fund is exhausted and cannot cover liquidation losses, the exchange will forcefully close the positions of the profitable parties to eliminate risk exposure.

Ethena pointed out in the document that although ADL may theoretically lead to the passive closing of some hedging positions, in current mainstream exchanges (Binance, Bybit, OKX, etc.), the probability of its triggering is extremely low because:

The insurance fund size is sufficient;

The clearing system has multi-layer risk buffering and self-healing mechanisms;

When the market fluctuates, the exchange will prioritize risk mitigation through internal matching and position-by-position allocation.

Even if individual locations trigger ADL, Ethena can passInstantly rebuild hedging positions and proactively realize unrealized profits and losses(realize PnL) to quickly return to market neutrality.

Overall, ADL’s impact on Ethena is limited toThe risk of short-term position interruption will not pose a systemic threat to USDe’s price anchoring or asset security.

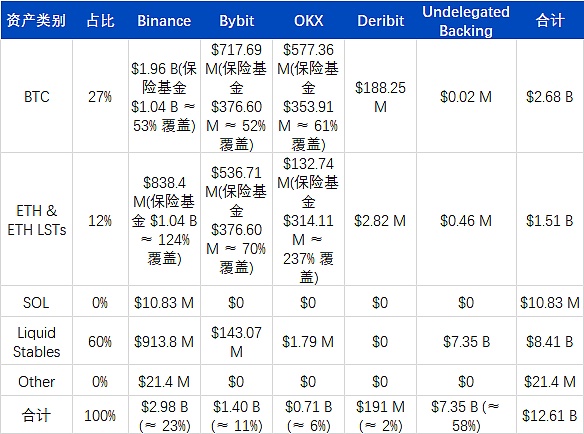

Multi-exchange risk fund carrying capacity assessment

Based on the distribution of Ethena’s hedging positions and the risk reserve scale of each major exchange, the following calculations can be made:

As ofOctober 11, 2025, the total market-wide single-day clearing total is approximately$20 billion.

Among them, the risk fund balance officially disclosed by Binance fell by approximately$200 million, it is estimated that its performance under extreme market conditionsRisk absorption rate is about 10%.

If the current size of Binance’s risk fund is approximately$1 billionCalculate, then its performance under similar market conditionsTheoretical maximum liquidation carrying capacityApproximately:

≈ USD 100 billion in single-day liquidation volume (corresponding to 10% risk absorption rate)

Ethena’s hedging positions are distributed across multiple mainstream exchanges (Binance, Bybit, OKX, etc.), which has a significant risk diversification effect.

Estimated based on public data:

-

Binance: ~$1.04 billion

-

Bybit: approximately US$380 million

-

OKX: ~$320 million

Approximately US$2 billion in total

Under the same assumption (about 10% risk absorption rate), the total risk fund size of the three major platformsTheoretically capable of carrying a single-day liquidation shock of approximately $200 billion, without triggering systemic risks.

This result shows that Ethena’s multi-exchange hedging strategy has good risk distributionSufficient flexibility and defensive depth, even in extreme fluctuations, the risk of systemic position reduction (ADL) is still within control.

Reference link

https://app.ethena.fi/dashboards/transparency

https://www.binance.com/en/trade/USDE_USDT?type=spot

https://www.bybit.com/en/trade/spot/USDE/USDT

https://aavescan.com/ethereum-v3/usde

https://dune.com/KARTOD/AAVE-Liquidations

https://community.chaoslabs.xyz/aave/risk/liquidations

https://intel.arkm.com/explorer/entity/binance

https://portal.llamarisk.com/ethena/overview

https://www.binance.com/en/futures/funding-history/perpetual/insurance-fund-history

https://www.bybit.com/en/announcement-info/insurance-fund/

https://www.okx.com/zh-hans/trade-market/risk/swap

https://help.defisaver.com/protocols/aave/ethena-liquid-leveraging-on-aave-in-one-transaction

https://governance.aave.com/t/arfc-susde-and-usde-price-feed-update/20495

https://data.chain.link/feeds/ethereum/mainnet/usde-usd

https://www.binance.com/zh-CN/support/announcement/detail/9eb104f497044e259ad9bd8f259f265c?utm_source=chatgpt.com

https://www.binance.com/zh-CN/support/announcement/detail/f3d5d97ed12c4f639019419bd891705e?utm_source=chatgpt.com

https://www.binance.com/zh-CN/support/announcement/detail/0989d6c7f32545bfb019e3249eaabc3f

https://www.binance.com/en/margin/interest-history

https://www.coinglass.com/BitcoinOpenInterest