1. Introduction

Jersey has a tax system that is independent from the United Kingdom. It has long been known for its “low tax burden, clear system, and simple structure” and is one of the most attractive offshore financial centers in the world.The island’s tax system adheres to local governance and takes into account international compliance standards, providing a flexible and stable tax environment for traditional financial services, wealth management institutions and the emerging crypto economy.

Unlike other countries, Jersey’s institutional response to crypto-assets is not radically innovative, but rather represents a cautious, layered, compatibility-oriented path choice.In terms of taxation, it continues the traditional design of tax exemption on capital gains and low corporate tax burden, but retains the flexibility of “commercial” and “purposeful” judgments in the identification of behavior; in terms of supervision, it expands the existing legal boundaries and incorporates virtual assets into conventional frameworks such as anti-money laundering, transaction information disclosure, and licensing systems, rather than creating a new encryption code.

2. Jersey Crypto Tax Regime

2.1 Jersey tax system

Jersey is a British Crown Dependency with a high degree of autonomy and independent tax and financial regulatory systems.Its tax system is known for its simplicity, stability, and low tax burden, and it is committed to providing an attractive tax environment for global investors and high-net-worth individuals.The main tax types and rates are as follows:

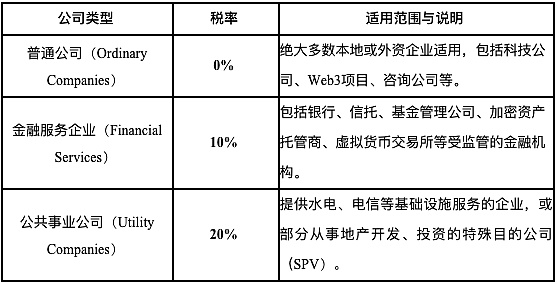

①Corporate tax: Jersey adopts a “0-10-20” classified tax rate structure, that is, the standard corporate income tax rate is 0%, 10% applies to financial services companies, and 20% applies to public utility companies.

②Personal income tax: The unified tax rate is 20%, with no progressive structure, and a basic tax exemption (around 17,000 pounds, slightly adjusted every year). There is no capital gains tax, inheritance tax, or gift tax.

③Goods and Services Tax (GST): Goods and services tax was introduced in 2008, with a unified tax rate of 5%. It is similar to value-added tax but has a narrower scope. It is mainly applicable to local goods and service transactions. Financial services, export services, etc. are usually tax-free.

This tax system design not only serves traditional finance, but also provides policy space for crypto-asset-related businesses, and has become one of the key factors in attracting Web3 companies to register and operate on the island.

2.2 Jersey crypto tax policy

2.2.1 Qualification of crypto assets

From the overall regulatory perspective, Jersey regards crypto assets as an “asset” rather than legal tender, and does not recognize them as securities or financial products.This means that at the legal and tax levels, crypto assets neither enjoy legal status nor are they automatically included in the regulatory scope of financial instruments. Instead, they are functionally identified based on specific usage scenarios:

Based on the JFSC (Jersey Financial Services Commission) definition, Jersey regulators identify crypto-assets as “digital representations of value that can be traded or transmitted, and used for payment or investment,” but do not regard them as legal tender.If cryptoassets are used for investment and are held to increase in value, they are considered an investment asset similar to “personal property” and are subject to similar tax rules as ordinary property.

According to the JFSC 2018 ICO Guidance Note, if a token has characteristics such as participation in the issuer’s profits, asset claims, redemption commitments, management rights or income expectations, it will be recognized as a security. If it has the characteristics of a collective investment arrangement, it will be treated as a “collective investment scheme” and needs to be evaluated on a case-by-case basis based on its equity structure.If you engage in mining or on-chain services to obtain crypto-assets, the relevant income may be regarded as “commercial income” or consideration for “reimbursed services” and need to be included in the scope of income tax or corporate tax.

The Jersey regulator emphasizes the principles of risk orientation and use classification in the supervision and taxation of crypto assets. It does not bring all virtual assets into the scope of supervision across the board. Instead, it classifies the transactions, holdings, circulation, services and other activities of crypto assets separately to determine whether current financial regulations or anti-money laundering obligations apply.

2.2.2 Tax policies related to crypto assets

Although Jersey has not yet promulgated a special tax law on crypto assets, its tax authority, Revenue Jersey, has adopted explanatory documents and practical cases to include crypto assets under the existing tax framework for classification.Overall, Jersey’s tax system for crypto-assets adopts the basic principles of purpose orientation, attribute determination, and risk adaptation.Different taxation entities and activity scenarios will apply differentiated tax rules. The following are the main situations:

(1) Personal holding and trading

For natural persons who hold crypto-assets only for long-term investment or occasional trading, gains in value are generally considered capital gains and are not subject to tax in Jersey.However, if the transactions are frequent and of a commercial nature, such as using leverage or continuously providing liquidity, the relevant income will be regarded as business income and will need to be reported at a 20% personal income tax rate.The identification of “trading behavior” in Jersey refers to the HMRC “Badges of Trade” principles (BIM20205) of the British Revenue and Customs Administration.In addition, non-capital income such as staking income, airdrops, and node rewards are usually considered taxable income and must be paid accordingly.

(2) Enterprise ownership and operation

If a company engages in crypto-asset-related businesses, such as exchange operations, digital wallet custody, mining, token issuance, DeFi protocol development, etc., its operating income should be regarded as taxable business income.According to Jersey’s “0-10-20” corporate tax classification: general technology or platform companies may be subject to a 0% corporate tax rate; if they involve financial services (such as encrypted asset custody, transaction matching, financial product issuance, etc.), a 10% tax rate may be applicable; if they are identified as public utilities or real estate investment companies, a 20% tax rate may be applied.

(3) Mining behavior

There is no specific legislation prohibiting or exempting crypto asset mining from taxation in Jersey.Officials pointed out in the Cryptocurrency Tax Treatment document that if mining activities are “occasional or non-commercial”, they do not constitute taxable activities; however, if mining is continuous, profitable and organized, the crypto assets produced constitute taxable income and should be included in current income and taxed at market prices.

(4) Crypto payment and GST issues

Although Jersey implements a 5% Goods and Services Tax (GST), the tax authorities have made it clear that the “act of exchange” of cryptoassets themselves as a means of payment does not constitute a taxable transaction.In other words, when users use Bitcoin or Ethereum to purchase goods or exchange fiat currencies or other virtual currencies, the act itself does not generate GST obligations.However, if a merchant accepts crypto payments and provides taxable goods or services, the goods themselves still need to pay GST as required.At this time, encrypted assets are only regarded as payment media, and there is no real difference from using cash or credit cards.

3. Establishment and improvement of Jersey’s crypto regulatory framework

Jersey’s crypto-asset regulatory framework is led by the Jersey Financial Services Commission (JFSC).JFSC is responsible for the supervision, regulation and development of the financial services industry in Jersey, including the supervision of virtual assets. Its responsibilities mainly include:

① Develop regulatory policies and guidelines: JFSC will issue guidance notes and other documents to clarify the regulatory approach to virtual assets in Jersey, including issuing guidelines and licenses for virtual currency exchanges.

② Registration and licensing: Enterprises operating in the virtual asset field in Jersey must register with the JFSC and obtain all necessary licenses or permits.

③Supervision and enforcement: JFSC is responsible for supervising regulated entities to ensure their compliance with Jersey’s anti-money laundering/anti-terrorist financing laws and other regulatory requirements.At the same time, the JFSC also has the authority to take enforcement actions against entities that violate these requirements.

④ Set compliance and supervision standards: JFSC sets compliance and review standards for the virtual asset industry.For example, companies must have personnel with appropriate skills and experience, including designated anti-money laundering reporting officers (MLROs) and deputy reporting officers (Deputy MLROs), as well as key personnel responsible for compliance and internal oversight.The JFSC also oversees whether virtual asset service providers comply with the Travel Rule and international crypto asset tax reporting standards.

⑤International cooperation: JFSC cooperates and exchanges information with other regulatory agencies and international organizations to promote the coordination and consistency of global virtual asset supervision.

Jersey has not formulated a special code for crypto assets. Instead, based on the original financial supervision system and anti-money laundering system, Jersey has gradually brought virtual assets and their service providers into the regulatory track by adding definitions, expanding the scope of application, and implementing a registration system.The following are the core legal and regulatory documents currently relevant to crypto-assets:

①Financial Services (Jersey) Law 1998

This Act is the most basic financial regulatory law in Jersey and stipulates that any business providing specified financial services in Jersey must register with the JFSC or apply for a license.The JFSC clearly stated in 2016 that virtual currency exchanges fall within the regulatory scope of the law and therefore must be registered as a “Money Service Business”.

②Proceeds of Crime (Jersey) Law 1999

This is Jersey’s core anti-money laundering and counter-terrorism financing law and applies to all high-risk industries, including crypto businesses.The law requires companies engaged in the virtual asset business to perform the following obligations: customer due diligence (CDD), transaction record retention, and reporting of suspicious transactions to the Jersey Financial Crime Unit (JFCU).

③Virtual Currency Exchange Regulations

JFSC issued regulatory regulations specifically for virtual currency exchanges in 2016, requiring them to strictly implement AML/CFT measures and establish a sound internal control and governance structure.These regulations bring crypto trading platforms into the substantive regulatory system.

⑤”Initial Coin Offerings Guidance Note”

The JFSC issued this guideline in 2017 to clarify the scope of regulatory application of ICOs in Jersey.The document emphasizes that ICOs will be evaluated on a case-by-case basis and will determine whether existing financial services regulatory laws are applicable based on the nature of the tokens issued. If the tokens have securities properties or constitute collective investment tools, they will need to obtain a license and be subject to supervision.

⑥Information Accompanying Transfers of Funds (Jersey) Regulations 2017, revised in 2023

This regulation is used to implement FATF’s “Travel Rule”, which requires all VASPs to collect and exchange sender/receiver identification information in virtual asset transfers. It is an important measure for Jersey to enhance the transparency of cross-border crypto transactions.

⑦ “OECD Crypto-Asset Reporting Framework Regulations, 2024–2025”

Jersey will join the CARF agreement in 2024 and implement local regulations in 2025, requiring all crypto asset service providers to fulfill their obligations to collect and report customer tax information and implement automatic information exchange with other jurisdictions.

In Jersey, the tax and regulatory arrangements related to virtual assets are based on the Financial Services Act and the Proceeds of Crime Act, and are gradually improved through scenario-based detailed regulations and international cooperation provisions.The “Financial Services Law” establishes the licensing requirements for emerging businesses such as crypto exchanges to be included in the management of “money service businesses”, while the “Proceeds of Crime Law” serves as the anti-money laundering and counter-terrorism financing bottom line for all virtual asset activities, covering obligations such as customer due diligence, transaction records and suspicious activity reporting.On this basis, the “Initial Coin Offering Guidelines” make a functional classification of token issuance activities and clarify whether different issuance models should be included in the existing regulatory framework for securities or collective investments.The Information Accompanying Fund Transfers Regulations and the CARF regulations further strengthen the transparency of cross-border capital flows and tax information, ensuring that Jersey maintains the advantages of a flexible tax system while being consistent with international compliance requirements.

4. Summary and outlook

With its simple and flexible tax system and progressive regulatory strategy, Jersey is gradually building an attractive and compliant crypto-asset institutional environment.In terms of tax system, Jersey still maintains its traditional advantages – no capital gains tax and low corporate tax burden, which provides favorable conditions for the implementation of the crypto industry.However, it can be seen that Jersey does not encourage speculative arbitrage-style structural design. Instead, it uses the tax definition of “commercial activities” to clarify the boundaries and leave room for regulatory judgment. This fuzzy boundary is the source of its flexibility.

In the future, Jersey will inevitably be affected by the tightening of international rules, especially the implementation of the OECD’s CARF framework and FATF’s transparency requirements for VASPs, which will gradually compress its policy buffer zone.The real challenge facing Jersey may not be how to “attract more crypto companies,” but how to maintain institutional autonomy while establishing a regulatory image that is trustworthy but does not overly sacrifice flexibility.