Written by: Paolo & Andy @VDX

TL;DR

-

Big Picture: Why is financial chain-up a top-level national strategy and market trend in the United States —RWA is the tool for global assets to “degeographically and chemically export and compete for on-chain liquidity”. The United States uses high-quality assets + open boundaries + standard output to build a road network for free circulation of global capital and assets, pushing the US dollar’s pricing and liquidation radius to the open chain.

-

The essence and core value creation of RWA:RWA is essentially an on-chain reissue of real-world assets, rewriting “issuance-flow-pricing-transaction-clearing-settlement-combination”; its value comes from 1)Efficient and trustworthy settlement, 2) Open-ended funds and assets matching, 3) Asset composability.Improve corporate capital efficiency and asset plasticity.

-

Market structure:Early competition for on-chain asset issuance, next stage competition channel + ecological integration: the focus at this stage is to open upCompliant issuance + on-chain integration, run through the top model; as the issuance threshold sinks, competition will shiftChannel control and ecological coordination (market making, redemption, mortgage, hedging, distribution), DeFi protocol integration, liquidity routing and scenario access are the core tools.

-

Opportunities for entering different links of the industrial chain:The core link includes “Publisher – Tokenization Platform – Distributor”, plus third-party service providers such as blockchain financial contracts, oracles, law firms, custody, and auditing. In the future, the industry will converge to“RWA Prime Broker” super platform, integrate issuance, compliance, clearing and settlement with distribution/liquidity.

-

Publisher: Focus on short-termRate of return and liquidity cash, give priority to strong consensusand the underlying layer of differentiation

-

Tokenization platform: value capture is relatively low and may be integrated by upstream and downstream, pay attention toCompliance and neutrality

-

Distributor: Mastering control of fund routing and expected to achieve scale, the focus is onFund acquisition and channel coverage

Big Picture: Why is financial chaining a top-level national strategy and market trend in the United States

Looking at the multiple policies and remarks of Project Crypto, Trump administration and SEC Chairman Paul Atkins, we believe that financial chaining may have risen to the de facto top-level national strategy of the United States.The positioning is to make the US dollar an open chain, the tools are stablecoins and RWA, the path is legislative anchor + US dollar asset opening + fund channel access (traditional financial institutions, CEX, DeFi); the goal is to expand the US dollar interest rates and rules into the settlement gravity field of the open chain.From the GENIUS Act stablecoin bill passed in July to the accelerated entry of traditional asset management, exchanges, and banks, this chain has actually started to operate.

The US financial chain promotion measures mainly include three aspects

-

Institutional grasp: decentralization of issuance rights, pricing rights and anchoring rights are more market-oriented and concentratedEstablished at the federal levelStablecoin/RWA license framework, reserve quality, disclosure frequency, penetration standards;The control tool evolved from “authority control” to “market choice competition”.

-

Assets: Uplinking the “US dollar, US bonds, US stocks”BundleUS dollar assetsMove on the chain,Let global DeFi/on-chain institutions use US dollar interest rates as the “gravity field”;Mortgage and hedgingAvailable,Redemption and liquidationSpeed up and absorb global idle stablecoins and risky funds into US dollar assets.

-

Channel tool: Standardize the “cleaning and settlement pipeline” to the open chain

The assets that will be packaged on the chainAccess to traditional financial institutions (broker firms, stock exchanges), encrypted CEX and on-chain DEX/DeFi protocols, expand users and capital tentacles, and at the same time, with the introduction of on-chain asset issuance regulatory rules, the regulatory logic is gradually embedded into the agreement.

Long-term impact trends

1. For global financial and capital flows:The US dollar’s “gravity field” has expanded, and the US dollar’s on-chain pricing power and asset anchoring power have been enhanced.

2. For other areas:Liquidity is siphoned, “regulation follows/defense”, forcing regulation and market infrastructure to upgrade.

3. For the crypto industry:The issuance of stablecoins has risen, and crypto assets have risen, but structured differentiation has occurred.

4. Opportunities for RWA issuers/participants:RWA connects to the global capital highway network to reduce growth and financing costs, and LEGO financial releases asset liquidity.

RWA Core Value Creation: More than Financing

– Essence = Asset reissue + Full process rewriting

– Value = Clearing and Settlement Efficiency × Distribution Radius × Composability.

RWA’s value creation closely revolves around the core advantages of blockchain technology:

1. Efficient and reliable clearing settlement:Reshape the underlying architecture of enterprise operations

To B (Financial Institution) – Achieve the upgrade of underlying infrastructure and more standardized/convenient asset issuance, solve the problems of trust, traceability and transparency through blockchain technology, and achieve more efficient clearing and settlement, and gradually realize the transformation of the traditional financial system.

To Enterprise – Reduce wear and tear of intermediary institutions, simplify cross-border and off-site processes, enhance reconciliation and penetration, and accelerate capital turnover

2. Open finance:Break the growth ceiling

By allowing high-quality assets to enter the global clearing and settlement network, it helps to improve the problem of financing difficulties in the original channel, improves the matching efficiency of the capital and asset sides, and significantly expands the issuance and distribution radius, and the constraints of “difficulty/expensive financing” are diluted by networked liquidity, which greatly improves the efficiency of capital allocation and opens up a new imagination space for corporate growth.

3. Composability:Detonate business model innovation

Connect off-chain assets and on-chain funds to realize the license-free combination of assets and leverage in a more efficient network.The chain allows combinations such as “revenue enhancement + hedging + re-pled” to form a new paradigm of asset operation.

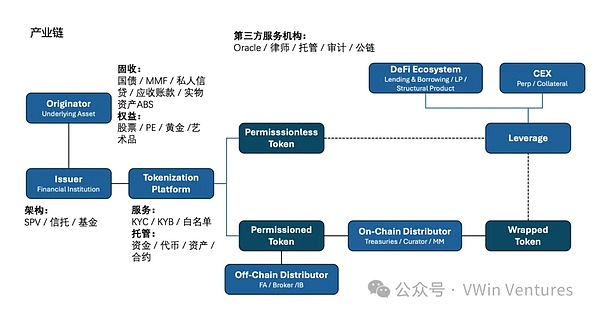

Industrial Chain: How enterprises position and participate

– Issuer-tokenization platform-distributor three-stage type, neutral third party (orbiter/custody/law firm/audience) forms the base.

– The focus of competition has shifted from “can be issued” to “channel and ecological integration”, and the final convergence is to RWA Prime Broker.

The core link of the RWA industry is asset issuers + tokenization technology platforms + distributors, plus third-party service agencies (oracists/lawyers/custodians/auditors/auditors/on-chain contracts, etc.), which are expanded to blockchain native scenarios through on-chain packaging and redistribution after off-chain compliance issuance.

– Three-end positioning of the industrial chain: issuers connect compliance and high-quality asset supply, tokenization platforms provide neutral on-chain issuance infrastructure, distributors integrate the ecosystem and master funding entrances.

– Corporate core concerns: Issuance depends on yield and liquidity, platform depends on compliance and neutrality, and distribution depends on user acquisition and channel coverage.

– Competitive pattern: the issuance side is scattered; the platform side is squeezed by upstream and downstream, but a third-party head neutral platform will appear; the distribution side is relatively concentrated (including on-chain ecology and CEX).

– Current pain points: lack of cross-border extension motivation at both issuance and distribution; platform technology is homogeneous and value capture is thin.

– Evolution direction: The industry will converge into the “RWA Prime Broker” super platform, integrating issuance, compliance, clearing and settlement with distribution/liquidity.

Market structure and opportunities for breakthrough

– The first-mover enjoys the “traffic × valuation” dividend, and the barriers quickly shift from license/issuance to cross-domain integration and operation capabilities.

– The capital side prefers high returns and high liquidity, and oversupply on the asset side – high-quality targets take the lead under mismatch, and long tails are overflowed.

The current market is in the stage of opening up compliant issuance + trying to integrate ecologically, and extending leading asset cases.Companies that have potential flow and liquidity dividends in the early stage of the market. Enterprises that are the first to RWA to RWA of high-quality assets can enjoy significant “flow and liquidity dividends”. Early successful cases can often obtain excess valuation premiums in the capital market. With the development of the industry, the barriers to asset issuance gradually decrease, market dividends gradually narrow, and competition will shift to deeper industrial integration capabilities.

RWA underlying assets are mainly divided into two categories:

– Fixed income products (treasury bonds/MMF/private credit/accounts receivable/physical assets ABS, etc.) provide stable cash flow returns

– Equity assets (stocks/PE/gold/artwork, etc.) provide volatility.

The market development stage follows three core changes brought by RWA to the industry: compliance issuance – open finance – compatibility.From the release of permitted tokens, to permissionless wrappers, and then to RWA ecosystem, the mainstream global markets have gradually opened up compliance boundaries to explore derivative scenarios.

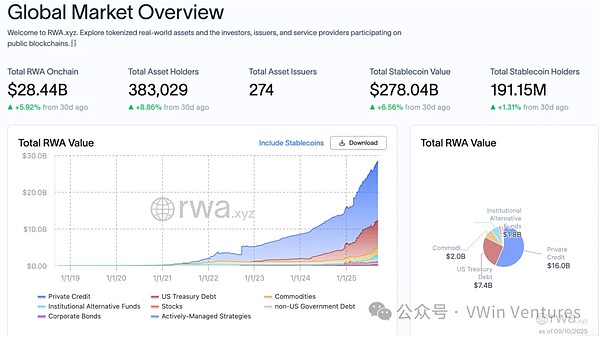

Looking at the current development of the capital and asset side of the market, although the size of stablecoins on the capital side has accelerated growth, most native funds on the chain still favor high returns and high odds on the chain, and the corresponding audience and capital side of RWA assets are relatively short of; in contrast, the real world asset side has relatively oversupply on-chain financing.

Therefore, the asset side should give priority to top assets and differentiated assets, and empower asset appreciation; similarly, as a distribution channel, we should give priority to finding high-quality assets for funds.Market development also gives priority to mainstream assets with strong consensus and high liquidity. As the scale of the capital side gradually increases, it gradually spills over to long-tail and alternative assets.In the end, the scale distribution of all things is on the chain stage, and the scale distribution of the investment products converges to the traditional financial market structure.

Opportunities for breaking the road in the industrial chain link

Issuers rely on top assets to start volume, form economies of scale or expand differentiated assets

– The market issuance threshold is gradually lowering, and long-term issuers are gradually extending to the downstream. The vertical track has the opportunity to form a leading issuer + bundled third-party service provider, combined with distribution channels + brands, to achieve stronger bargaining power;

– Long-term decentralized chain investment banks (similar to traditional financial fields, there are local leading asset issuers), but they will form regional leading RWA Prime Broker.

Tokenized platforms open up issuance channels, open up compliance and technical architecture, and are relatively neutral to third-party

– Core capabilities lie in compliance capabilities, licenses, architecture reuse, and marginal cost reduction

– Long-term upstream integration or third-party leading technical service providers such as Paxos

Distributors seize the capital side and open up the chain ecosystem

– Can be CEX or on-chain

– Long-term barriers are strengthened, relative to head concentration

On-chain ecological integration

RWA brings asset choices with real gold flow and different risk preferences and yields to the entire chain ecosystem. At the same time, various infrastructures on the chain also provide additional empowerment of underlying RWA assets.

Analyzing the transmission and combination mechanisms of different types of RWA assets on the chain, the most directly related infrastructure includes oracle-DEX-borrow pools, etc.Among them, the oracle is the core infrastructure for the RWA asset chain mapping on and off-chain mapping, and DEX is a liquidity gathering place, becoming a key link in the upstream of the RWA ecosystem.

Since equity and fixed income RWA assets have different profiles on the chain, there are also differences in their impact mechanisms on the chain infrastructure: the audience of equity RWA assets pursues volatility, and core infrastructure is oriented around transactions, such as Perp Trading, revolving loans and leverage, etc.; the audience of fixed income RWA assets pursues yield rates, and the secondary price fluctuates little and the transaction demand is low, and core infrastructure is oriented around yield rates, such as pledge, income swap (similar to Pendle), etc.

Key case analysis: Different attempts on compliance and chain

– Trade-off function of path = compliance boundary × right confirmation depth × distribution radius

– First “ownership and pricing penetration”, then “channel and market making arrangements” – clearly define the rights/income rights and extreme rights confirmation paths, select the neutral oracle/custody and issuance paths; design the CEX+DeFi distribution, market making/redemption/repurchase and income components simultaneously

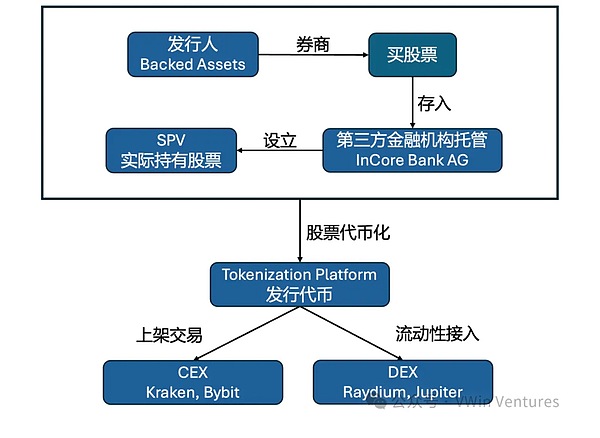

Equity: Stock Tokenization

There are currently three mainstream solutions on the market:

1. xStocks/Dinary offshore SPV shares are tokenized, and the to B business model is used to connect to the chain and off-chain exchanges, and avoid the risk of being recognized as securities by weakening the corresponding underlying rights and interests of tokens (such as voting rights, etc.); relatively compliant release in the form of securities

2. Robinhood uses CFD CFD to map stock price fluctuations. Token only anchors the income and does not correspond to the ownership of the underlying assets. There is no native token on the issuance chain yet. It quickly implements land grabbing and waits for policy supervision to be implemented.

3. StableStocks adopts a large account system, and users use stablecoin subscription and redemption tokens to correspond to securities trading within securities companies, to C business model.

Core user portraits are divided into three categories:

1. Access to new markets: Cover investors in third world countries or emerging markets that cannot invest in your company due to restrictions on opening accounts by traditional brokerage firms.

2. Provide new ways to play: On-chain investors can use the company’s stock tokens to play higher-level leverage and hedging strategies through DeFi lending or derivatives agreements to increase the depth and breadth of stocks

3. Empower traditional stock holders: Traditional Long-term holders achieve profit enhancement through on-chain financial management (locking the value of underlying stocks through options, and providing liquidity tokens to provide liquidity to earn excess returns)

xStocks U.S. stock chain structure

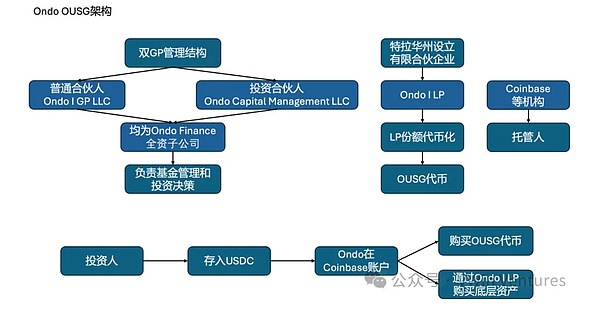

Fixed income category: US bond tokenization

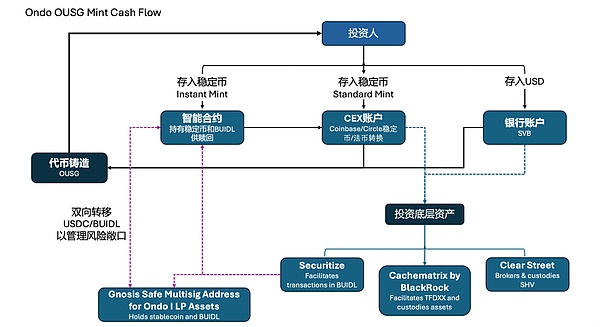

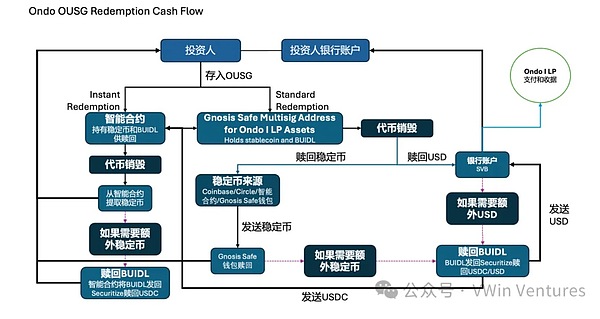

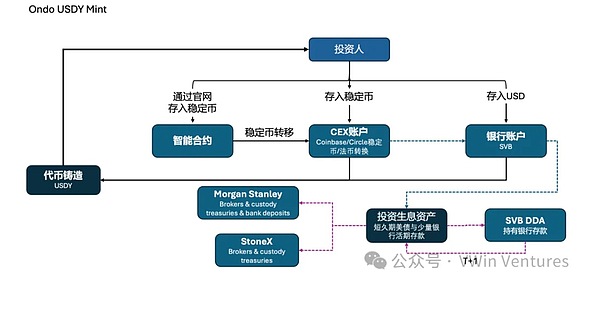

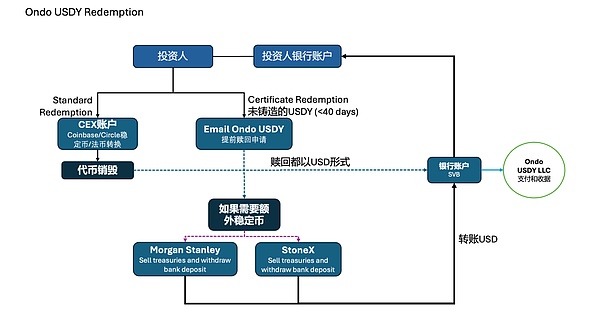

Ondo Finance uses two packaged tokens to achieve risk-free returns of underlying US debt to global investors: OUSG (lowering the threshold for domestic US investors through Reg-D) & USDY (exporting to global investors through Reg-S)

Core user portrait:

1. Lower the investment threshold: Open investments that were originally only allowed to participate in by institutions or high-net-worth individuals to a wider range of qualified investors around the world

2. Empower idle funds: Provide stablecoin income enhancement to institutions and individuals holding a large number of stablecoins around the world (on-chain hedge funds, on-chain idle stablecoins)

3. Build a bottom-income position: become the foundation of the on-chain treasury investment portfolio

OUSG architecture

OUSG Mint Cash Flow

OUSG Redemption Cash Flow

USDY Mint Cash Flow

USDY Redemption Cash Flow

Action recommendations to RWA participants

-

Priority for inventory of core assets:Sorting internal corporateHigh consensus, easy to be standardized, easy to penetrate, strong cash flow or high growth potentialassets.E.g. Mainstream financial assets – high-credit corporate bonds, accounts receivable, gold ETFs, etc.; mainstream equity assets – high liquidity, high market-oriented demand, and high growth potential.Differentiated assets– A second-stage breakthrough is provided by amplified assets (such as specific ABSs) in brands and channels.

-

Select the release path:Combining the sale target and channel, integratingLeading compliance agencies in mainstream regionsOr adoptMature offshore paths such as overseas SPVs.Choose a trusted third-party neutral platform (issuance, custody, oracle, lawyer, etc.) to ensure strong binding of price/net value to the underlying layer and clear KYC/AML and information disclosure boundaries.

-

Distribution and liquidity integration: Synchronously layout on-chain protocols and CEX channels, design market-making/redemption/repurchase and income enhancement components (such as pledge and swap); strive to access the mainstream liquidity pool to avoid liquidity fragmentation.

-

Clarify risks:Legal penetration and investor suitability – Ensure that the rights/earnings rights are clearly defined, and the right confirmation/liquidation path in extreme situations is clear; pricing and oracle risks: net value/price are strongly consistent with the bottom layer, avoiding liquidity mismatch triggering runs; Operation and reputation – Redemption/repurchase and market making mechanisms are transparent and verifiable, and information disclosure and audit frequency can be accepted by institutional investors.

The essence of RWA is to perform a “reissuance” of your company’s high-quality assets on a global blockchain, which rewrites the entire process from issuance, circulation, pricing to portfolio.Its core business value comes from a more efficient and reliable clearing and settlement system, an open financial network that breaks boundaries, and disruptive permissionless combination capabilities.

Corporate action suggestions:

-

Highly attach importance to strategy: regard financial chaining as a core strategy related to the future competitiveness of enterprises, rather than a simple financing tool;

-

Actively embrace in action: take stock of the high-quality assets that are most suitable for RWA, give priority to top assets and differentiated assets, and pass the first sample case;

-

Strong cooperation: Select the top partners in compliance, technology and global distribution to seize the dividends of the blue ocean market.