Author: Encrypted Coconut

The current market diversified game framework

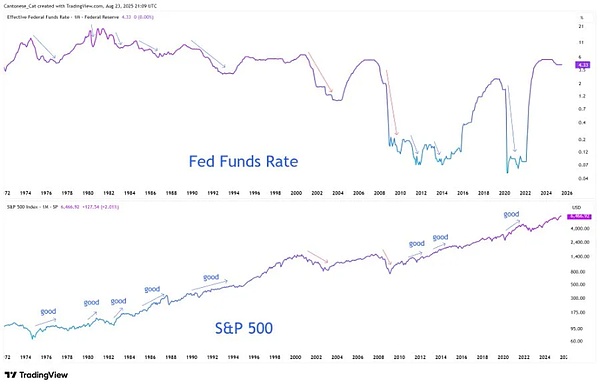

Each round of economic and financial cycle has its dominant narrative logic, and the current market is in an intertwined game of multiple contradictions: Bitcoin’s seasonal fluctuations form a hedge against the cyclical characteristics after halving, the Federal Reserve’s policy statements are vague and inflation stickiness constitute tension, and behind the steepening of the bond market yield curve, the dual signals of economic relief and recession warning are also implied.This “break” at the narrative level is not a short-term market noise, but a concentrated reflection of the current macro environment complexity and structural contradiction, which also determines that the market will find a new balance fulcrum in the violent fluctuations.

Disassembled from the time dimension, the current market fluctuation logic presents clear layered characteristics:

-

Short term (1-3 months):Bitcoin’s “September Effect” forms a core contradiction with the particularity of the post-halving cycle.Historical data shows that September is the traditional weak month of Bitcoin, and the decline caused by long clearing has occurred repeatedly, but 2025 is the year after Bitcoin halving, and the third quarter of the year after halving in history often shows a bullish trend. This conflict between seasonal laws and cyclical characteristics will most likely lead to significant fluctuations for the first time this year.

-

Medium term (3-12 months):The credibility crisis in the Federal Reserve policy has become a key variable.Forced interest rate cuts under inflationary pressure will break the traditional monetary policy transmission path and reshape the valuation logic of assets such as stocks, bonds, commodities, etc. The ambiguity of policy signals and the sensitivity of market expectations will further amplify asset price fluctuations.

-

Long-term (more than 1 year):The structural demand pillars of the cryptocurrency market are facing tests.Unlike previous cycles that rely on retail investors or institutional capital flows, the core support of current cryptocurrency demand comes from corporate cryptocurrency treasury (such as BTC and ETH positions of institutions such as MSTR and Metaplanet). If this structural pillar is reversed due to balance sheet pressure, it will trigger the transmission from the demand side to the supply side and reshape the cryptocurrency cycle logic.

For investors, the core cognitive framework of the current market needs to shift from “single narrative verification” to “multi-narration collision” – effective signals are no longer hidden in isolated data points (such as single-month inflation data and Bitcoin’s single-day increase), but exist in contradictions and resonances of different narrative dimensions, which also determines that “volatility” is no longer an accessory of risk, but has become a core value carrier that can be mined in the current environment.

Bitcoin: Double Pricing of Seasonal Game and Half Cycle

(I) The conflict between historical laws and current particularities

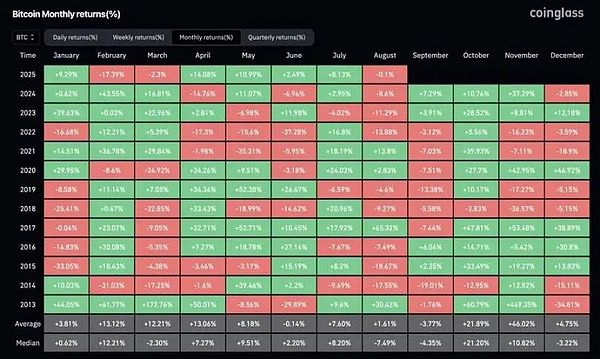

Looking back at the monthly yield data of Bitcoin from 2013 to 2024, the performance in September continued to be weak: it fell by 9.27% in September 2018, fell by 13.88% in September 2022, and fell by 12.18% in September 2023, and the transmission path of “long clearing → price pullback” repeatedly appeared.But the special feature of 2025 is that it is in a critical year after the Bitcoin halving. Historical data shows that the third quarter of the year after the halving (July-September) often presents strong characteristics: a 27.7% increase in Q3 in 2020 and a 16.81% increase in Q3 in 2024. This collision between “seasonal weakness” and “cyclical strength” constitutes the core contradiction in current Bitcoin pricing.

(II) Regression logic after volatility compression

As of August 2025, Bitcoin has not yet seen a single-month increase of more than 15%, which is significantly lower than the normal “month increase of 30%+” in the historical bull market cycle, reflecting that the current market volatility is in a state of temporary compression.From the perspective of cyclical rules, the surge in the bull market has the characteristics of “concentrated release” rather than uniform distribution – the increase in November 2020 was 42.95%, the increase in November 2021 was 39.93%, and the increase in May 2024 was 37.29%, all verifying this rule.

From this, the current investment logic can be derived: In the remaining 4 months in 2025, the regression of volatility is a deterministic event, and the differences are only at the time node.If there is a pullback in September due to seasonal factors, it will form a dual support of “cyclical support after halving + volatility repair expectations”, which is likely to become the last entry window before the fourth quarter rise market starts.This logic of “callback is opportunity” is essentially a rebalancing of the weight of “seasonal short-term disturbance” and “cyclical long-term trend”, rather than a linear deduction that simply relies on historical laws.

Fed: Split in Policy Narratives and Pricing Restructuring of Credibility Risks

(I) Misreading of signal and true intention of Jackson Hall’s speech

Federal Reserve Chairman Powell’s statement at the 2025 Jackson Hall Global Central Bank Annual Meeting was initially interpreted by the market as a “radical easing signal”, but in-depth analysis shows the subtlety of its policy logic:

-

Limitations of interest rate cut path:Powell made it clear that “reserving space for the interest rate cut in September”, but at the same time emphasized that “this move does not mark the start of the easing cycle”, that is, a single interest rate cut is more inclined to “phase adjustments under inflationary pressure” rather than “the beginning of a new round of easing”, to avoid the market from forming the expected inertia of “continuous interest rate cuts”.

-

The fragile balance of the labor market:The “double slowdown in labor supply and demand” mentioned by it implies deep risks – the current stability of the employment market does not stem from economic resilience, but the synchronous weakness of both supply and demand. This balance has “asymmetric risk”: once broken, it may trigger a rapid transmission of a wave of layoffs, which also explains the Federal Reserve’s swing between “rate cuts” and “anti-recession”.

-

Major turn to the inflation framework:The Federal Reserve officially abandoned the “average inflation target system” launched in 2020 and returned to the “balanced path” model in 2012 – the core change lies in “no longer tolerate inflation being phased higher than 2%” and “no longer single focus on the unemployment rate target”. Even if the market has digested the expectation of interest rate cuts, the Federal Reserve is still strengthening the signal of “2% inflation target anchor” in an attempt to repair the credibility previously damaged by policy swings.

(II) Policy dilemma in the environment of stagflation and the impact of asset pricing

The core contradiction facing the Federal Reserve is “forced interest rate cuts under the pressure of stagflation”: core inflation continues to stick to the impact of tariffs (Powell made it clear that “the impact of tariffs pushing up prices will continue to accumulate”), and the weak signal of labor market is revealed, while the high debt burden of the United States (government debt/GDP ratio continues to rise) makes “high interest rates last longer” unfeasible at both the fiscal and political levels, forming a vicious cycle of “spension → lending → printing of money”.

This policy dilemma is directly transformed into the reconstruction of asset pricing logic:

-

Trustworthiness risk becomes the core pricing factor:If the 2% inflation target degenerates from the “policy anchor” to the “visional expression”, it will trigger the bond market to reprice the “inflation premium” – long-term US Treasury yields may rise due to the upward trend of inflation expectations, and the “profit valuation gap” in the stock market will further expand.

-

The hedging value of scarce assets is highlighted:Against the backdrop of rising risk of fiat currency credit dilution, the “anti-inflation dilution” function of assets such as Bitcoin, Ethereum, and gold will be strengthened, becoming the core allocation targets for hedging the decline in credibility of the Federal Reserve’s policy.

Bond Market: Recession Warning Signs Behind Steeper Curves

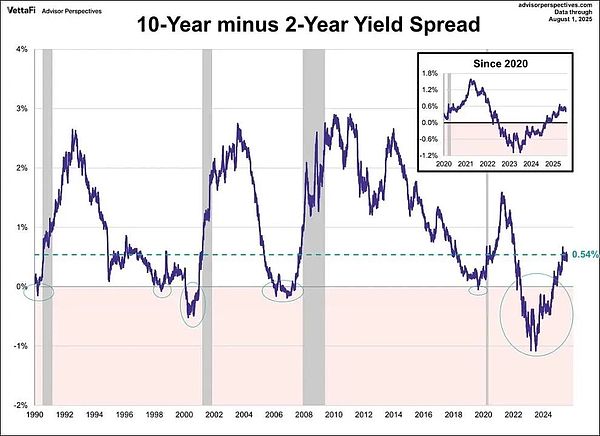

(I) The surface and essence of steeper curve

In August 2025, the 10-year and 2-year U.S. bond interest rate spread rebounded from the historical deep inverted range to +54 basis points, showing the characteristics of “curve normalization” on the surface, which was interpreted by some market views as a signal of “economic risk mitigation”.However, historical experience (especially in 2007) warns that the steepening after the curve is inverted has two paths: “benevolent” and “malignant”:

-

Benign steepening:Due to the improvement of economic growth expectations, the positive profit prospects of corporate enterprises drive long-term interest rates to rise faster than short-term interest rates, which is often accompanied by rising stock markets and narrowing of credit spreads.

-

Vicious steepening:The reason for short-term interest rates to fall rapidly due to policy easing expectations, while long-term interest rates to remain high due to inflation expectations is essentially a warning of “policy easing cannot hedge the risk of recession”. The subprime mortgage crisis broke out after the curve steepened in 2007, which is a typical case of this path.

(II) Determination of current steeper risk attributes

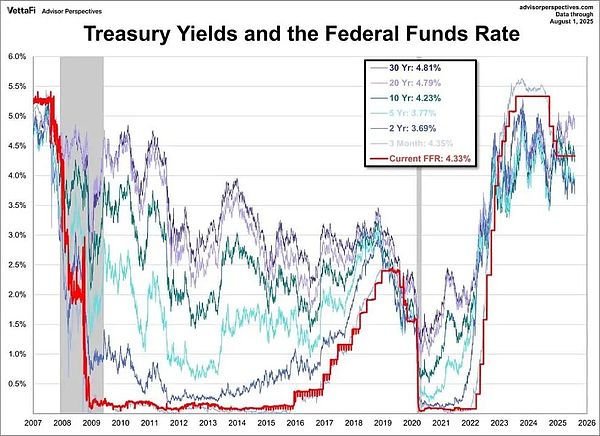

Combined with the current U.S. Treasury yield structure, the 3-month U.S. Treasury yield (4.35%) is higher than the 2-year yield (3.69%), and the 10-year yield (4.23%) is higher than the 2-year, but it is mainly supported by long-term inflation expectations. The market interprets the Fed’s September interest rate cut expectations as “passive response to stagflation” rather than “active adjustment under economic resilience”. This combination of “short-term interest rate decline + long-term inflation stickiness” is in line with the core characteristics of “vicious steepening”.

The core basis of this judgment is that the steepening curve does not stem from the restoration of growth confidence, but the market’s pricing of “policy failure” – even if the Federal Reserve initiates interest rate cuts, it will be difficult to reverse the dual pressures of core inflation stickiness and economic weakness. Instead, it may further intensify the risk of stagflation through the transmission of “loose expectations → upward inflation expectations”, which also means that there is a significant recession warning signal hidden under the “surface health” of the current bond market.

Cryptocurrencies: The test of vulnerability in the structural demand pillar

(I) Logical differences in demand in the current cycle

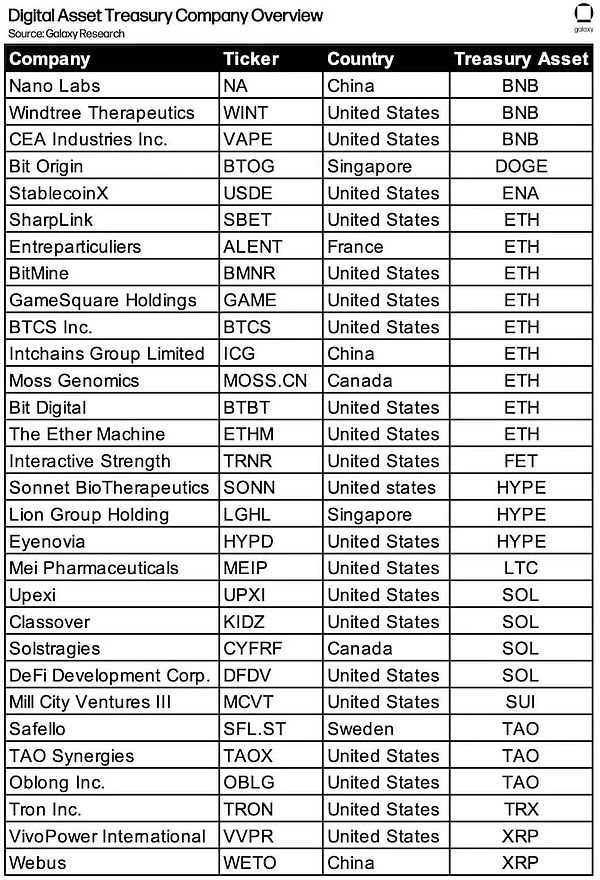

Comparing the core drivers of the three-wheeled bull cycle of cryptocurrency: the ICO financing boom in 2017 (incremental funds led by retail investors), DeFi leverage and NFT speculation in 2021 (resonance between institutions and retail investors), and in 2025, it showed the characteristics of “structural demand-led” – corporate crypto treasury has become the core buyer’s force.

It can be seen from Galaxy Research data that as of August 2025, more than 30 listed companies around the world have included crypto assets such as BTC, ETH, SOL, etc. into the treasure allocation, among which MSTR’s BTC holdings exceeded 100,000, and the proportion of ETH holdings in Bit Digital, BTCS and other institutions in circulation continues to increase.This “enterprise-level allocation demand” is different from the previous “speculative demand” and is regarded as a “stabilizer” of the current cryptocurrency market.

(II) Potential risks of demand reversal

The current stability of corporate crypto treasury depends on the support of “net value premium” – If the stock prices of relevant companies fall due to market fluctuations or performance pressure, resulting in an imbalance in the ratio of “crypto asset holdings / total company market value”, which may trigger a chain reaction of “forced to reduce holdings of crypto assets to stabilize the balance sheet”.Historical experience shows that the end of the cryptocurrency cycle often stems from the “reversal of the core demand mechanism”: ICO regulation tightened in 2017 ended the bull market, DeFi leverage liquidation triggered a collapse in 2021, and if corporate cryptocurrency treasury changes from “net buyer” to “net seller” in 2025, it will become a key trigger point for the cycle turn.

The particularity of this risk lies in its “structural transmission” – the short-term trading behavior of corporate holdings is different from retail investors or institutions. It often has the characteristics of “large scale and long cycle”, which may break the current “fragile state of supply and demand balance” of the cryptocurrency market, triggering the dual pressure of price overshoot and liquidity contraction.

Conclusion: Reconstruction of investment logic of volatility as core assets

The essence of the current market is the “era volatility pricing era under narrative collisions”. The four core contradictions constitute the underlying framework of investment decisions: Bitcoin’s “seasonal pullback” collides with “up after halving”, the Federal Reserve’s “cautious statement” collides with “stagflation and interest rate cuts”, the “curve normalization” collides with “recession warning”, and the “corporate treasury support” collides with “demand reversal risk”.

In this environment, investors’ core abilities need to shift from “predicting the direction of a single narrative” to “capturing volatility opportunities in multiple narrative collisions”:

-

Actively embrace volatility:No longer regard volatility as a risk, but as the core carrier for obtaining excess returns – such as using Bitcoin’s seasonal pullback layout in September to arbitrage through interest rate fluctuations during the steepening stage of the US bond curve.

-

Strengthen hedging thinking:Against the backdrop of declining policy credibility and rising stagflation risks, scarce assets such as Bitcoin, Ethereum, and gold are allocated to hedge against the risks of fiat currency credit dilution and asset valuation reset.

-

Tracking structural signals:Pay close attention to “structural indicators” such as changes in corporate crypto treasury positions, the implementation of the Fed’s inflation target, and the slope of the US Treasury yield curve. These indicators are key anchor points for judging the direction of narrative collision.

Ultimately, the current investment opportunity in the market is not “choosing a certain winning narrative”, but understanding that “volatility itself is an asset” – In an era of narrative collision, being able to control volatility, hedge risks, and capture the value fulcrum in contradictions is the core logic for building long-term investment advantages.